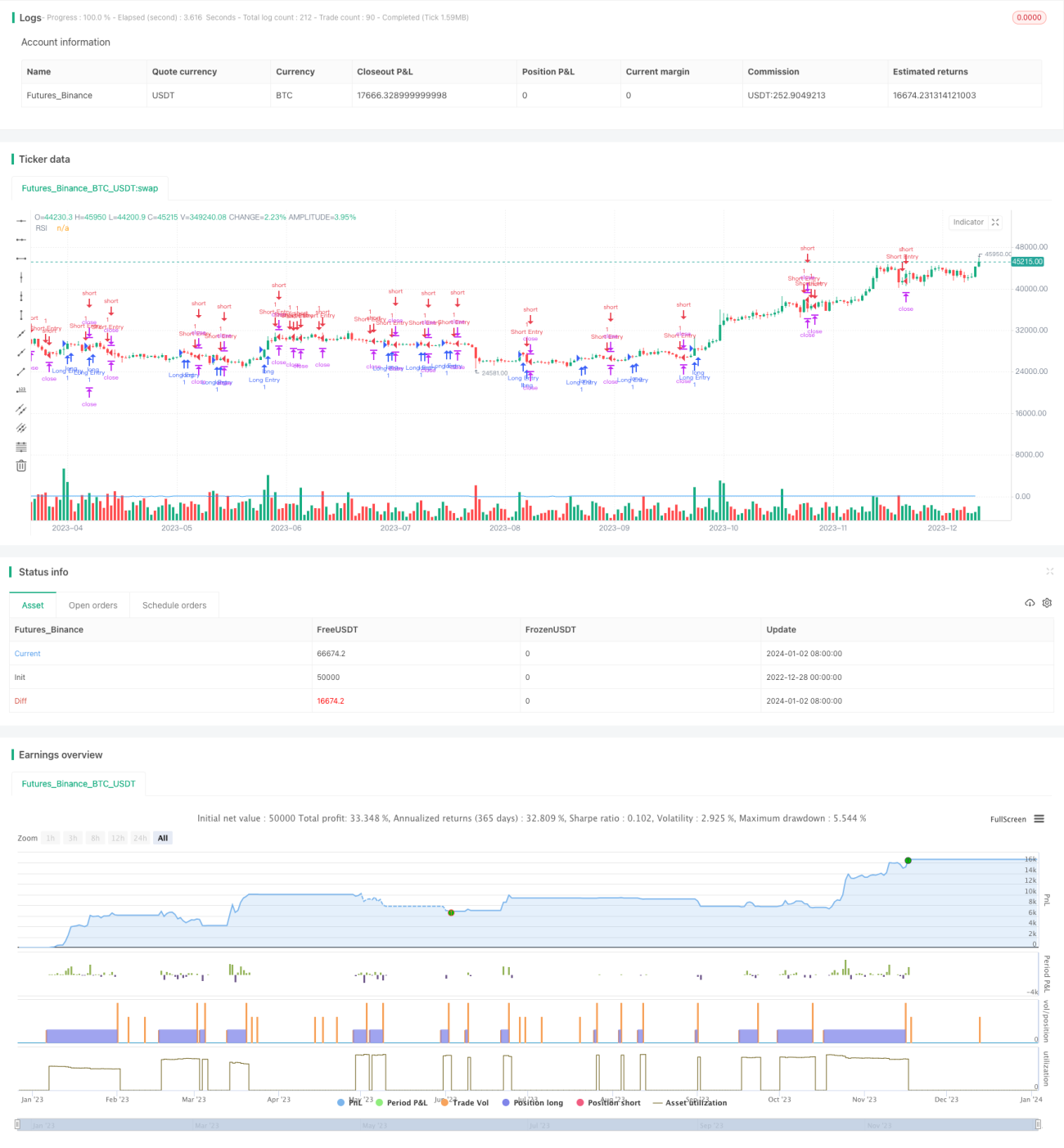

Chiến lược giao dịch nâng cao dựa trên RSI và điều kiện tùy chỉnh AI

Tổng quan

Ý tưởng cốt lõi của chiến lược này là kết hợp chỉ báo RSI và các điều kiện AI tùy chỉnh để phát hiện cơ hội giao dịch. Nó sẽ thiết lập vị thế mua hoặc bán khi thỏa mãn nhiều điều kiện, và sử dụng mức chốt lời và cắt lỗ cố định.

Nguyên lý chiến lược

Chiến lược này được thực hiện qua các bước sau:

- Tính toán giá trị RSI 14 kỳ

- Xác định hai điều kiện AI tùy chỉnh (mua và bán)

- Kết hợp điều kiện AI với vùng quá mua/quá bán của RSI để tạo tín hiệu vào lệnh

- Tính toán kích thước vị thế dựa trên tỷ lệ phần trăm rủi ro và số điểm dừng lỗ

- Tính toán giá chốt lời và cắt lỗ

- Mở vị thế khi tín hiệu vào lệnh được thỏa mãn

- Đóng vị thế khi điều kiện chốt lời hoặc cắt lỗ được đáp ứng

Đồng thời, chiến lược này cũng sẽ phát cảnh báo khi có tín hiệu giao dịch và vẽ đường RSI trên biểu đồ.

Phân tích ưu điểm chiến lược

Chiến lược này có những ưu điểm sau:

- Kết hợp RSI và điều kiện AI giúp phát hiện cơ hội giao dịch chính xác hơn

- Sử dụng tổ hợp nhiều điều kiện có thể lọc hiệu quả các tín hiệu giả

- Tính toán kích thước vị thế theo nguyên tắc quản lý rủi ro, kiểm soát rủi ro cho mỗi giao dịch

- Sử dụng phương pháp chốt lời và cắt lỗ cố định, rủi ro và lợi nhuận của mỗi giao dịch rõ ràng

- Có thể tùy chỉnh chiến lược tự do thông qua điều chỉnh tham số

Phân tích rủi ro chiến lược

Chiến lược này cũng tồn tại một số rủi ro:

- Cài đặt tham số RSI không phù hợp có thể dẫn đến tín hiệu giao dịch không chính xác

- Thiết kế điều kiện AI tùy chỉnh không đúng cũng có thể tạo ra tín hiệu sai

- Đặt số điểm dừng lỗ quá nhỏ có thể khiến dừng lỗ bị kích hoạt thường xuyên

- Khi thị trường biến động mạnh, phương pháp chốt lời và cắt lỗ cố định có thể làm mất thêm lợi nhuận hoặc tăng thua lỗ

Có thể giảm thiểu các rủi ro này bằng cách điều chỉnh tham số RSI, tối ưu hóa điều kiện AI, nới rộng khoảng cách dừng lỗ một cách hợp lý, v.v.

Hướng tối ưu hóa chiến lược

Chiến lược này còn có thể được tối ưu hóa qua các hướng sau:

- Thêm nhiều điều kiện AI tùy chỉnh, kết hợp nhiều yếu tố hơn để đánh giá xu hướng

- Tối ưu hóa tham số RSI để tìm ra tổ hợp tham số tốt nhất

- Kiểm tra các cơ chế chốt lời/cắt lỗ khác nhau như trailing stop, di chuyển chốt lời

- Thêm các điều kiện lọc bổ sung như khối lượng giao dịch tăng đột biến, để phát hiện các cơ hội giao dịch chất lượng cao

- Kết hợp thuật toán học máy để tự động tạo ra các tham số tối ưu

Tổng kết

Nhìn chung, đây là một chiến lược giao dịch nâng cao dựa trên chỉ báo RSI và các điều kiện AI tùy chỉnh, có khả năng tùy chỉnh và không gian tối ưu hóa lớn. Nó đánh giá hướng xu hướng bằng cách kết hợp nhiều nguồn tín hiệu, sử dụng cơ chế quản lý rủi ro và chốt lời/cắt lỗ để giao dịch. Chiến lược này có thể mang lại hiệu quả giao dịch tốt cho người dùng, đồng thời có khả năng mở rộng và không gian tối ưu hóa mạnh mẽ.

- 1