Chiến lược tối ưu hóa giao cắt đường trung bình động đa khung thời gian

1

Follow

1802

Followers

Tổng quan

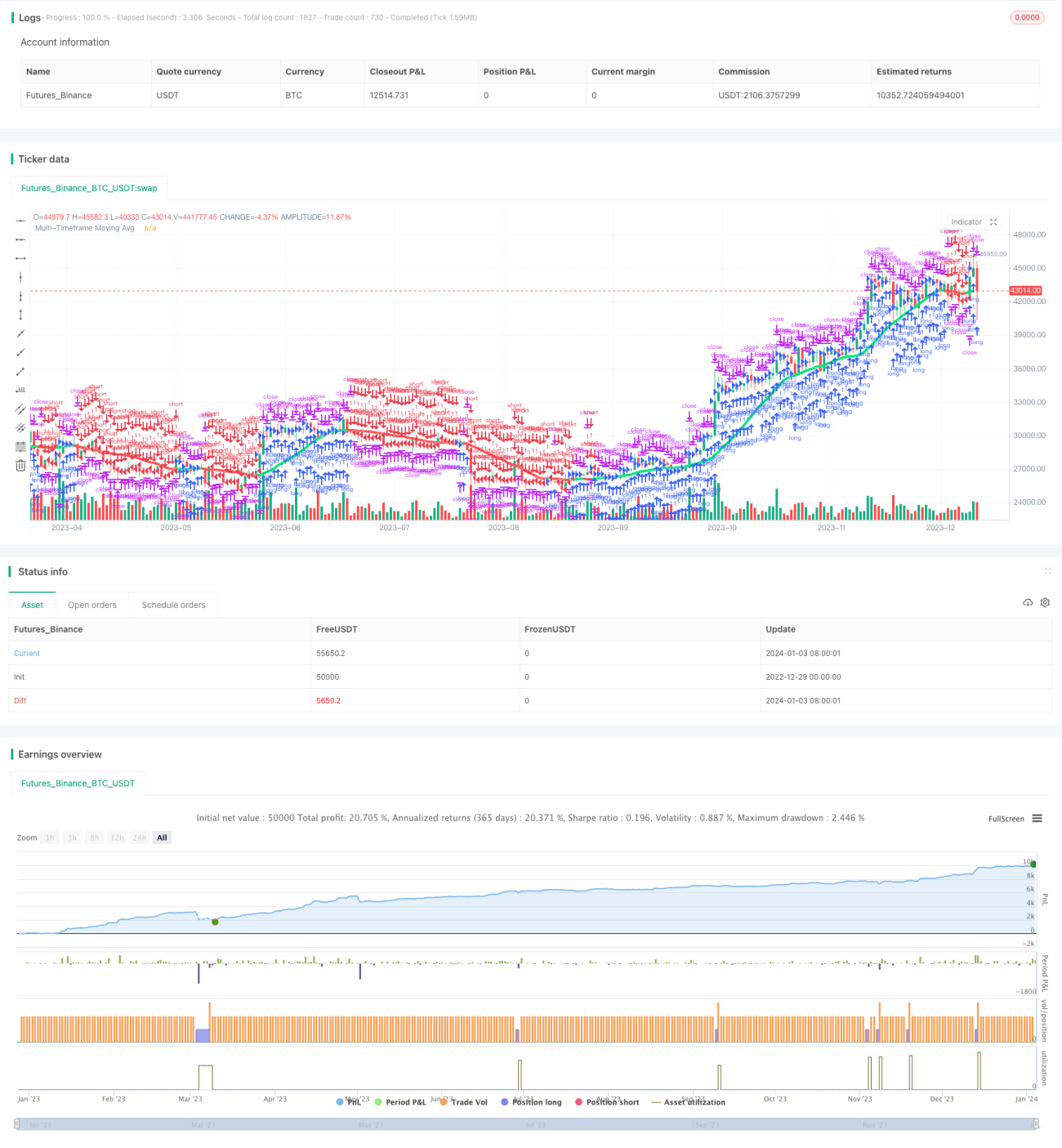

Chiến lược này được viết lại dựa trên chỉ báo nổi tiếng CM_Ultimate_MA_MTF, có thể vẽ đường trung bình động trên nhiều khung thời gian, thực hiện các giao dịch chéo MA giữa các chu kỳ thời gian khác nhau. Chiến lược cũng có chức năng trailing stop loss.

Nguyên lý chiến lược

- Dựa theo lựa chọn của người dùng, sử dụng các loại MA khác nhau để vẽ đường MA trên khung thời gian chính và các khung thời gian cao hơn.

- Khi đường MA nhanh cắt lên trên đường MA chậm, vào lệnh Long; khi đường MA nhanh cắt xuống dưới đường MA chậm, vào lệnh Short.

- Thêm cơ chế trailing stop loss để kiểm soát rủi ro hơn nữa.

Phân tích ưu điểm

- Giao cắt MA trên nhiều khung thời gian có thể cải thiện chất lượng tín hiệu, giảm tín hiệu nhiễu.

- Sự kết hợp các loại MA khác nhau có thể phát huy ưu điểm của từng chỉ báo, tăng tính ổn định.

- Trailing stop giúp cắt lỗ kịp thời, giảm xác suất thua lỗ lớn.

Phân tích rủi ro

- Chỉ báo MA có độ trễ, có thể bỏ lỡ cơ hội giao dịch ngắn hạn.

- Cần tối ưu hóa tham số chu kỳ MA phù hợp, nếu không có thể tạo ra quá nhiều tín hiệu nhiễu.

- Cài đặt điểm dừng lỗ không hợp lý có thể dẫn đến cắt lỗ không cần thiết.

Hướng tối ưu

- Có thể thử nghiệm các tổ hợp MA với tham số khác nhau để tìm tham số tốt nhất.

- Có thể thêm các chỉ báo khác để lọc, nâng cao chất lượng tín hiệu.

- Có thể tối ưu hóa chiến lược dừng lỗ để phù hợp hơn với đặc điểm thị trường.

Tổng kết

Chiến lược này tích hợp phân tích đa khung thời gian của đường trung bình động và phương pháp trailing stop loss, nhằm nâng cao chất lượng tín hiệu và kiểm soát mức độ rủi ro. Thông qua việc tối ưu hóa tham số và thêm các chỉ báo khác, có thể tăng cường hiệu quả của chiến lược.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1