Chiến lược giao dịch phá vỡ hai chiều dựa trên nến K

Tổng quan

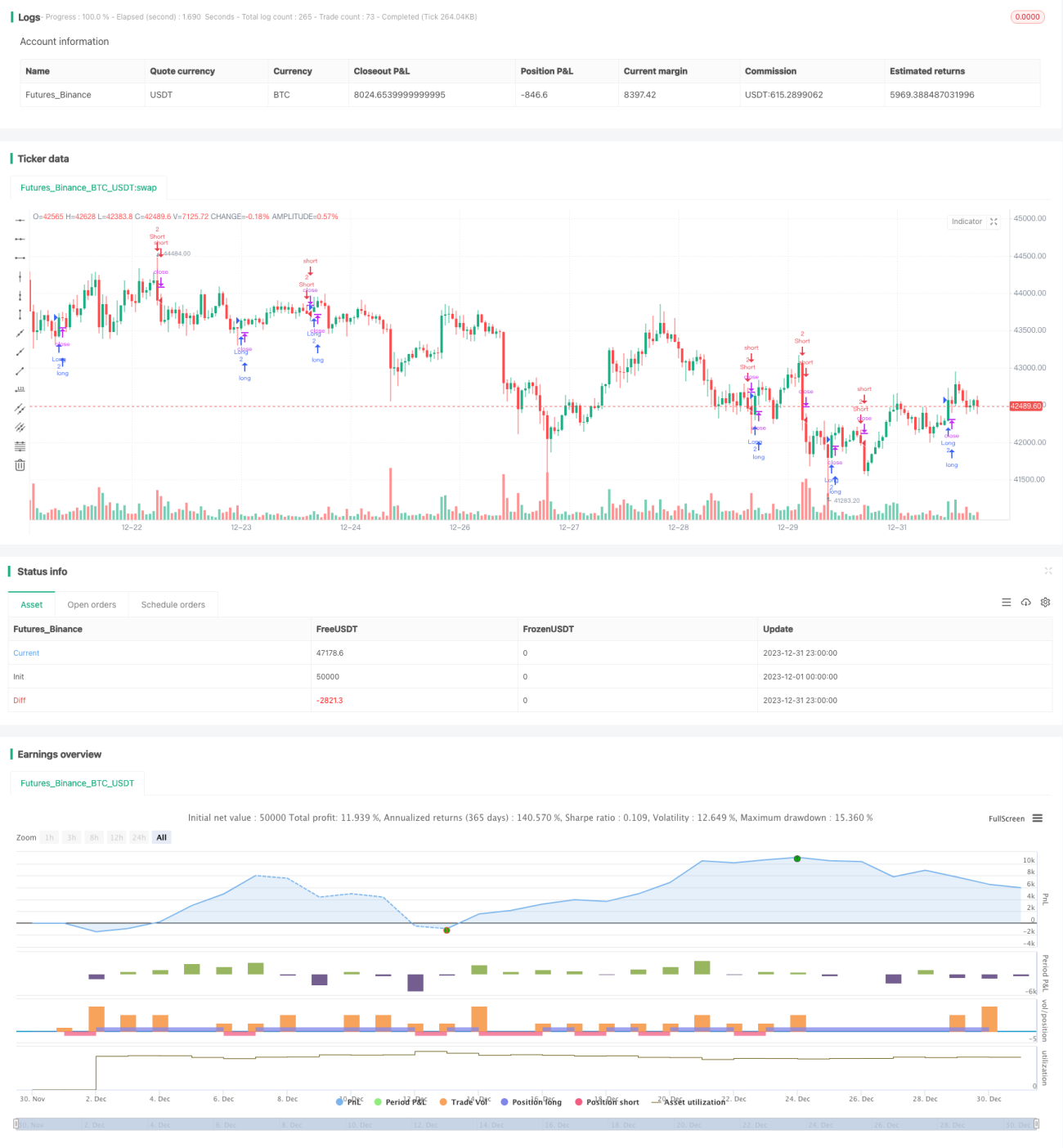

Đây là chiến lược giao dịch phá vỡ hai chiều dựa trên nến. Nó sẽ tạo ra tín hiệu giao dịch khi giá đóng cửa của nến hiện tại phá vỡ cả mức cao nhất và thấp nhất của hai nến trước đó.

Nguyên lý chiến lược

Logic cơ bản của chiến lược này là:

-

Xác định tín hiệu tăng (bull):

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]. Nghĩa là, giá đóng cửa của nến hiện tại lớn hơn giá mở cửa, đồng thời lớn hơn mức cao nhất của hai nến trước, trong khi giá thấp nhất của nến hiện tại lại thấp hơn giá thấp nhất của nến liền trước. -

Xác định tín hiệu giảm (bear):

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]. Nghĩa là, giá đóng cửa của nến hiện tại nhỏ hơn giá mở cửa, đồng thời nhỏ hơn mức thấp nhất của hai nến trước, trong khi giá cao nhất của nến hiện tại lại cao hơn giá cao nhất của nến liền trước. -

Khi tín hiệu tăng được kích hoạt, vào lệnh mua (long); khi tín hiệu giảm được kích hoạt, vào lệnh bán (short).

-

Có thể thiết lập mức cắt lỗ và chốt lời.

Chiến lược này tận dụng đặc điểm phá vỡ hai chiều, dựa trên việc phá vỡ các vùng giá quan trọng để xác định sự thay đổi xu hướng, từ đó tạo ra tín hiệu giao dịch.

Phân tích ưu điểm

Đây là một chiến lược phá vỡ tương đối đơn giản và trực quan, có những ưu điểm sau:

-

Logic rõ ràng, dễ hiểu và triển khai, không yêu cầu kỹ thuật cao.

-

Phá vỡ là tín hiệu giao dịch phổ biến, dễ hình thành xu hướng.

-

Có thể giao dịch cả hai chiều mua và bán, tăng cơ hội sinh lời.

-

Có thể linh hoạt thiết lập cắt lỗ và chốt lời để kiểm soát rủi ro.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

-

Rủi ro giao dịch hai chiều khá lớn, cần giám sát chặt chẽ.

-

Phá vỡ dễ bị mắc kẹt, có thể tạo ra tín hiệu giả.

-

Thiết lập tham số không phù hợp có thể dẫn đến giao dịch quá mức.

-

Thiết lập cắt lỗ và chốt lời không đúng cũng ảnh hưởng đến không gian lợi nhuận.

Có thể tối ưu hóa tham số và lọc sản phẩm phù hợp để giảm rủi ro.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Tối ưu tham số, như chu kỳ phá vỡ, biên độ cắt lỗ/chốt lời, v.v.

-

Thêm bộ lọc để tránh tín hiệu sai trong các tình huống như sideway, nhiễu.

-

Kết hợp các chỉ báo xu hướng để tránh vùng tích lũy.

-

Tối ưu quản lý vốn, cải thiện thuật toán khối lượng vị thế.

-

Tham số khác nhau cho từng sản phẩm, có thể kiểm tra và tối ưu riêng.

Tổng kết

Đây là một chiến lược đơn giản dựa trên ý tưởng phá vỡ hai chiều. Nó có ưu điểm logic rõ ràng, dễ triển khai, nhưng cũng tồn tại một số rủi ro giám sát nhất định. Thông qua tối ưu hóa tham số và điều kiện, có thể đạt được hiệu quả chiến lược tốt hơn.

- 1