Chiến lược lượng tử theo dõi xu hướng dựa trên chỉ báo Hull và chỉ báo LSMA

Tổng quan

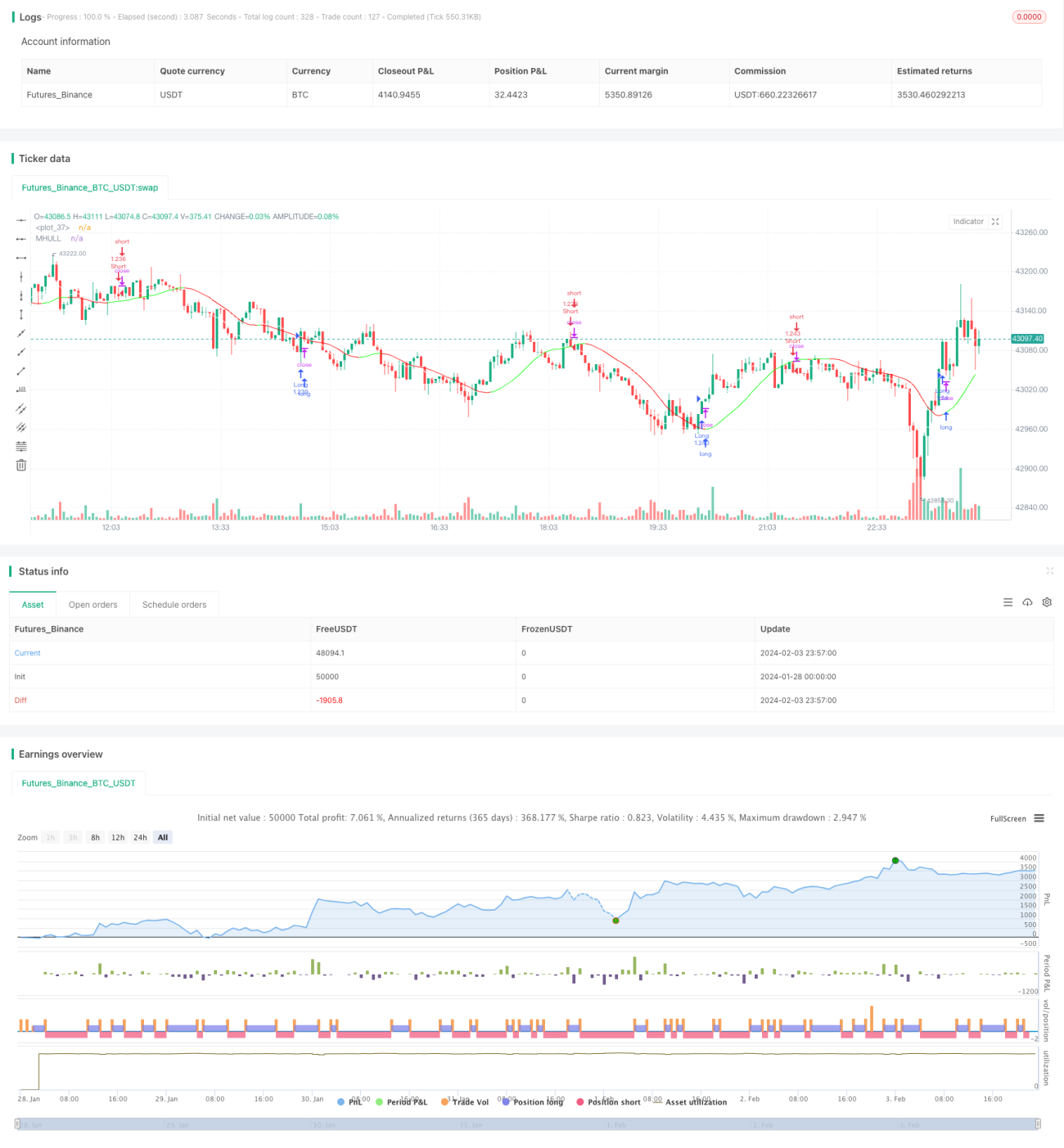

Chiến lược này kết hợp chỉ báo Hull và chỉ báo LSMA (Đường trung bình động bình phương tối thiểu) để xác định hướng xu hướng và điểm đảo chiều xu hướng, nhằm theo dõi xu hướng. Khi chỉ báo Hull cho thấy xu hướng tăng và LSMA cắt lên trên Hull thì mua lên; khi chỉ báo Hull cho thấy xu hướng giảm và LSMA cắt xuống dưới Hull thì bán xuống. Chiến lược này phù hợp với giao dịch tần suất trung bình thấp, có thể sử dụng trên khung thời gian 1 phút.

Nguyên lý chiến lược

-

Chỉ báo Hull được sử dụng để xác định hướng xu hướng của giá trị. Khi đường giữa (MHULL) nằm trên đường dưới (LHULL), điều đó cho thấy xu hướng tăng; ngược lại cho thấy xu hướng giảm.

-

Chỉ báo LSMA được sử dụng để xác định điểm đảo chiều xu hướng. Khi LSMA cắt lên trên MHULL, điều đó cho thấy xu hướng tăng hình thành hoặc tăng tốc; khi LSMA cắt xuống dưới MHULL, điều đó cho thấy xu hướng giảm hình thành hoặc tăng tốc.

-

Kết hợp cả hai: Khi chỉ báo Hull cho thấy xu hướng tăng (MHULL > LHULL) và LSMA cắt lên trên MHULL, thì mua lên; khi chỉ báo Hull cho thấy xu hướng giảm (MHULL < LHULL) và LSMA cắt xuống dưới MHULL, thì bán xuống.

-

Điểm dừng lỗ được đặt tại điểm dao động gần nhất. Dừng lỗ cho lệnh mua là mức thấp nhất gần đây, dừng lỗ cho lệnh bán là mức cao nhất gần đây.

Phân tích ưu điểm

Chiến lược này có các ưu điểm sau:

-

Chỉ báo Hull phản ứng nhanh, kịp thời nắm bắt sự chuyển đổi xu hướng; LSMA có độ mượt cao, nhận diện tín hiệu đảo chiều chính xác và đáng tin cậy. Sự kết hợp cả hai mang lại hiệu quả tốt.

-

Thông qua sự cắt nhau của LSMA để lọc các tín hiệu giả do chỉ báo Hull đưa ra, giảm xác suất giao dịch sai.

-

Sử dụng điểm dao động làm mức dừng lỗ, bảo vệ an toàn vốn ở mức tối đa.

-

Phù hợp với giao dịch tần suất trung bình thấp, có thể sử dụng trên khung thời gian 1 phút hoặc thấp hơn, tính ứng dụng rộng rãi.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

-

Trong thị trường dao động (sideway), chỉ báo Hull và LSMA có thể xảy ra nhiều lần cắt nhau, gây ra giao dịch quá thường xuyên. Cần điều chỉnh tham số phù hợp để giảm tần suất giao dịch.

-

Việc đặt dừng lỗ tại điểm dao động có thể bị kích hoạt do điều chỉnh giá ngắn hạn, cần mở rộng khoảng cách dừng lỗ hợp lý.

-

Do độ trễ của chỉ báo LSMA, có thể có rủi ro nhận định sai. Cần kết hợp các chỉ báo khác như mô hình nến để xác nhận.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Tối ưu hóa tham số của chỉ báo Hull và LSMA để kết hợp phù hợp hơn với các loại tài sản và khung thời gian khác nhau.

-

Thêm các điều kiện lọc dựa trên biến động, khối lượng giao dịch, v.v., để tránh giao dịch sai trong thị trường dao động.

-

Thêm hỗ trợ phán đoán từ thuật toán học máy để xác định xu hướng.

-

Kết hợp kỹ thuật học sâu để nhận diện các vùng hỗ trợ/kháng cự quan trọng, giúp dừng lỗ hợp lý hơn.

Tổng kết

Chiến lược này thông qua sự kết hợp giữa chỉ báo Hull và LSMA để phán đoán sự thay đổi hướng xu hướng, thực hiện giao dịch theo xu hướng. Ưu điểm là thao tác đơn giản, phản ứng nhanh, có thể áp dụng rộng rãi cho giao dịch định lượng tần suất trung bình thấp. Thông qua việc tối ưu hóa thêm các điều kiện lọc, hỗ trợ phán đoán và thuật toán dừng lỗ, có thể đạt được hiệu quả chiến lược tốt hơn.

- 1