Chiến lược tăng vị thế linh hoạt

Tổng quan

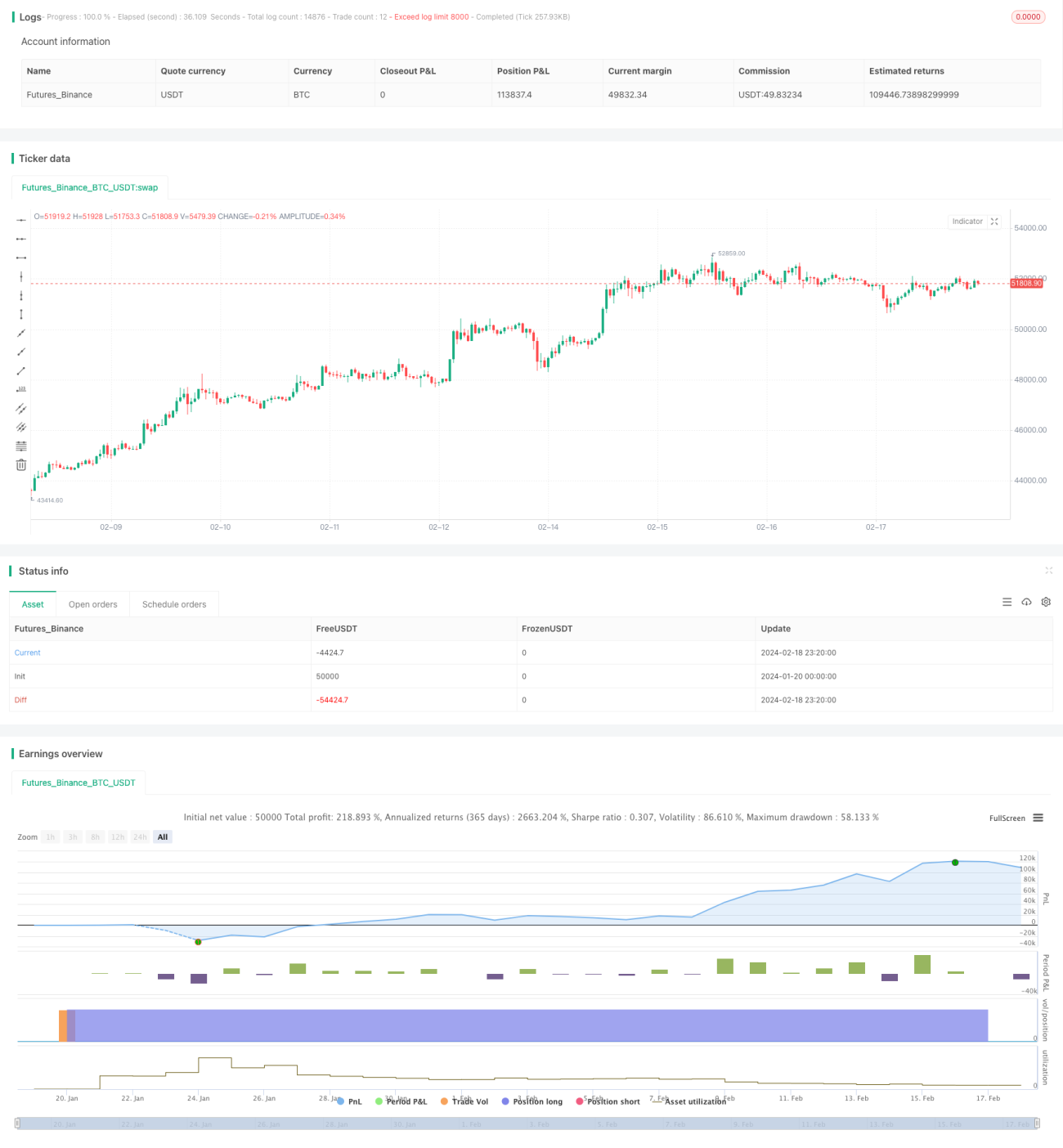

Ý tưởng chính của chiến lược này là tăng vị thế một cách linh hoạt dựa trên tín hiệu của hệ thống, xây dựng vị thế dần dần trong thị trường tăng giá nhằm kiểm soát rủi ro và đạt được mức giá vào lệnh trung bình thấp hơn.

Nguyên lý chiến lược

Chiến lược trước tiên thiết lập vốn khởi động và tỷ lệ phân bổ DCA. Khi đóng nến mỗi cây, nó tính toán tỷ lệ phân bổ đã điều chỉnh dựa trên biến động giá. Nếu giá tăng, nó giảm tỷ lệ; nếu giá giảm, nó tăng tỷ lệ. Nhờ đó, vị thế được tăng lên khi giá thấp. Sau đó, quy mô lệnh được tính dựa trên tỷ lệ đã điều chỉnh và số vốn còn lại. Khi đóng mỗi cây nến, nó đặt lệnh tăng vị thế cho đến khi vốn khởi động được sử dụng hết.

Bằng cách này, chiến lược có thể kiểm soát rủi ro và đạt được mức giá vào lệnh trung bình thấp hơn khi thị trường biến động. Đồng thời, nó thống kê giá vào lệnh trung bình và giá trung vị để đánh giá tình hình vào lệnh hiện tại.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

-

Có thể tăng vị thế linh hoạt: mở rộng vị thế khi thị trường giảm và thu hẹp vị thế khi thị trường tăng, từ đó kiểm soát rủi ro.

-

Đạt được mức giá vào lệnh trung bình thấp hơn giá trung vị, có lợi cho việc thu được biên lợi nhuận cao hơn.

-

Phù hợp với biến động của thị trường tăng giá, mang lại tỷ lệ lợi nhuận / rủi ro tốt.

-

Có thể cài đặt sẵn vốn khởi động và tỷ lệ DCA, kiểm soát lượng vốn mỗi lần tăng vị thế, tránh rủi ro quá lớn.

-

Cung cấp thống kê giá vào lệnh trung bình và giá trung vị, giúp trực quan đánh giá chất lượng vào lệnh.

Phân tích rủi ro

Chiến lược cũng tồn tại một số rủi ro nhất định:

-

Khi thị trường giảm mạnh đột ngột, chiến lược sẽ liên tục tăng vị thế, có thể gây tổn thất vốn lớn. Có thể đặt lệnh dừng lỗ để kiểm soát rủi ro.

-

Nếu thị trường tăng nhanh, mức tăng vị thế của chiến lược sẽ giảm, có thể bỏ lỡ phần lớn cơ hội tăng giá. Lúc này cần sử dụng các tín hiệu khác để thực hiện lối thoát linh hoạt (LSI).

-

Cài đặt tham số không phù hợp cũng mang lại rủi ro. Vốn khởi động quá lớn hoặc tỷ lệ DCA quá cao đều làm tăng tổn thất.

Hướng tối ưu hóa

Chiến lược có thể được tối ưu hóa theo các hướng sau:

-

Thêm logic dừng lỗ, ngừng tăng vị thế khi giảm mạnh.

-

Điều chỉnh động tỷ lệ DCA dựa trên biến động hoặc các chỉ báo khác.

-

Thêm mô hình học máy để dự đoán biến động giá, từ đó hướng dẫn quyết định tăng vị thế.

-

Kết hợp các chỉ báo kỹ thuật khác để xác định cấu trúc thị trường, ngừng tăng vị thế tại các điểm chuyển tiếp cấu trúc.

-

Thêm mô-đun quản lý vốn, điều chỉnh động lượng vốn mỗi lần tăng vị thế dựa trên tình hình tài khoản.

Tổng kết

Chiến lược này là một chiến lược tăng vị thế động rất thực tế. Nó có thể linh hoạt điều chỉnh vị thế theo biến động thị trường, đạt được mức giá vào lệnh trung bình thấp trong thị trường tăng giá. Đồng thời, nó tích hợp sẵn các cài đặt tham số để kiểm soát rủi ro. Nếu kết hợp với các chỉ báo kỹ thuật hoặc mô hình khác, có thể đạt được hiệu quả tốt hơn. Chiến lược này phù hợp với các nhà đầu tư theo đuổi lợi nhuận đầu tư dài hạn.

- 1