Chiến lược theo dõi xu hướng giao cắt DEMA

Tổng quan

Chiến lược này dựa trên sự giao cắt của đường trung bình động hàm mũ kép (DEMA) làm tín hiệu giao dịch, áp dụng phương pháp theo xu hướng, tự động đặt lệnh cắt lỗ và chốt lời. Ưu điểm của chiến lược là tín hiệu giao dịch rõ ràng, cài đặt cắt lỗ và chốt lời linh hoạt, có thể kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

-

Tính toán DEMA nhanh (8 ngày), DEMA chậm (24 ngày) và DEMA phụ trợ (có thể cấu hình).

-

Khi đường nhanh cắt lên đường chậm tạo tín hiệu vàng (golden cross), mua lên; khi đường nhanh cắt xuống đường chậm tạo tín hiệu tử (death cross), bán khống.

-

Thêm bộ lọc tín hiệu giao dịch, chỉ khi giá trị ngày hiện tại của đường phụ trợ cao hơn ngày trước đó mới tạo tín hiệu, tránh phá vỡ giả.

-

Sử dụng cơ chế cắt lỗ theo xu hướng, đường cắt lỗ sẽ điều chỉnh theo diễn biến giá, đảm bảo điểm cắt lỗ khóa một phần lợi nhuận.

-

Đồng thời đặt cắt lỗ và chốt lời theo tỷ lệ cố định, kiểm soát mức thua lỗ và lợi nhuận tối đa cho mỗi giao dịch.

Ưu điểm chiến lược

-

Tín hiệu giao dịch rõ ràng, dễ dàng xác định thời điểm vào và ra.

-

Thuật toán DEMA kép mượt hơn, tránh tối ưu quá mức, tín hiệu đáng tin cậy hơn.

-

Bộ lọc đường phụ trợ tăng hiệu quả đánh giá tín hiệu, giảm tín hiệu giả.

-

Sử dụng cắt lỗ theo xu hướng, có thể khóa một phần lợi nhuận, kiểm soát rủi ro hiệu quả.

-

Đặt cắt lỗ và chốt lời theo tỷ lệ cố định, kiểm soát mức thua lỗ tối đa cho mỗi giao dịch, tránh vượt quá phạm vi rủi ro.

Rủi ro chiến lược

-

Trong thị trường dao động (sideways), có thể tạo ra giao dịch thường xuyên, dễ làm tăng rủi ro, gây thua lỗ cho chiến lược.

-

Cài đặt tỷ lệ cắt lỗ cố định quá lớn, trong tình huống thị trường bất thường có thể kích hoạt cắt lỗ lớn.

-

Tín hiệu giao cắt DEMA bị trễ, trong thị trường biến động nhanh, mua gần đỉnh sẽ tăng rủi ro thua lỗ.

-

Khi triển khai giao dịch thực tế, chi phí trượt giá (slippage) sẽ ảnh hưởng đến lợi nhuận, cần điều chỉnh tham số chốt lời/cắt lỗ.

Tối ưu chiến lược

-

Có thể điều chỉnh tham số DEMA theo điều kiện thị trường để tìm điểm cân bằng tốt nhất.

-

Trong giao dịch thực tế cần xem xét chi phí trượt giá, mở rộng phạm vi cắt lỗ cố định phù hợp.

-

Có thể thêm các chỉ báo phụ trợ khác như MACD để tăng cường hiệu quả tín hiệu.

-

Có thể đặt giá trị bước của cắt lỗ theo xu hướng để tối ưu logic cắt lỗ.

Tổng kết

Chiến lược này tận dụng khả năng nhận biết xu hướng của DEMA, kết hợp cơ chế theo xu hướng để kiểm soát rủi ro, là một đại diện rất điển hình trong hệ thống chiến lược giao dịch xác định hướng xu hướng. Nhìn chung, chiến lược có tín hiệu rõ ràng, cài đặt cắt lỗ và chốt lời hợp lý, là một chiến lược giao dịch dễ nắm bắt, rủi ro có thể kiểm soát. Kết hợp tối ưu chi phí trượt giá và đánh giá chỉ báo phụ trợ trong giao dịch thực tế, có thể đạt được lợi nhuận đầu tư tốt.

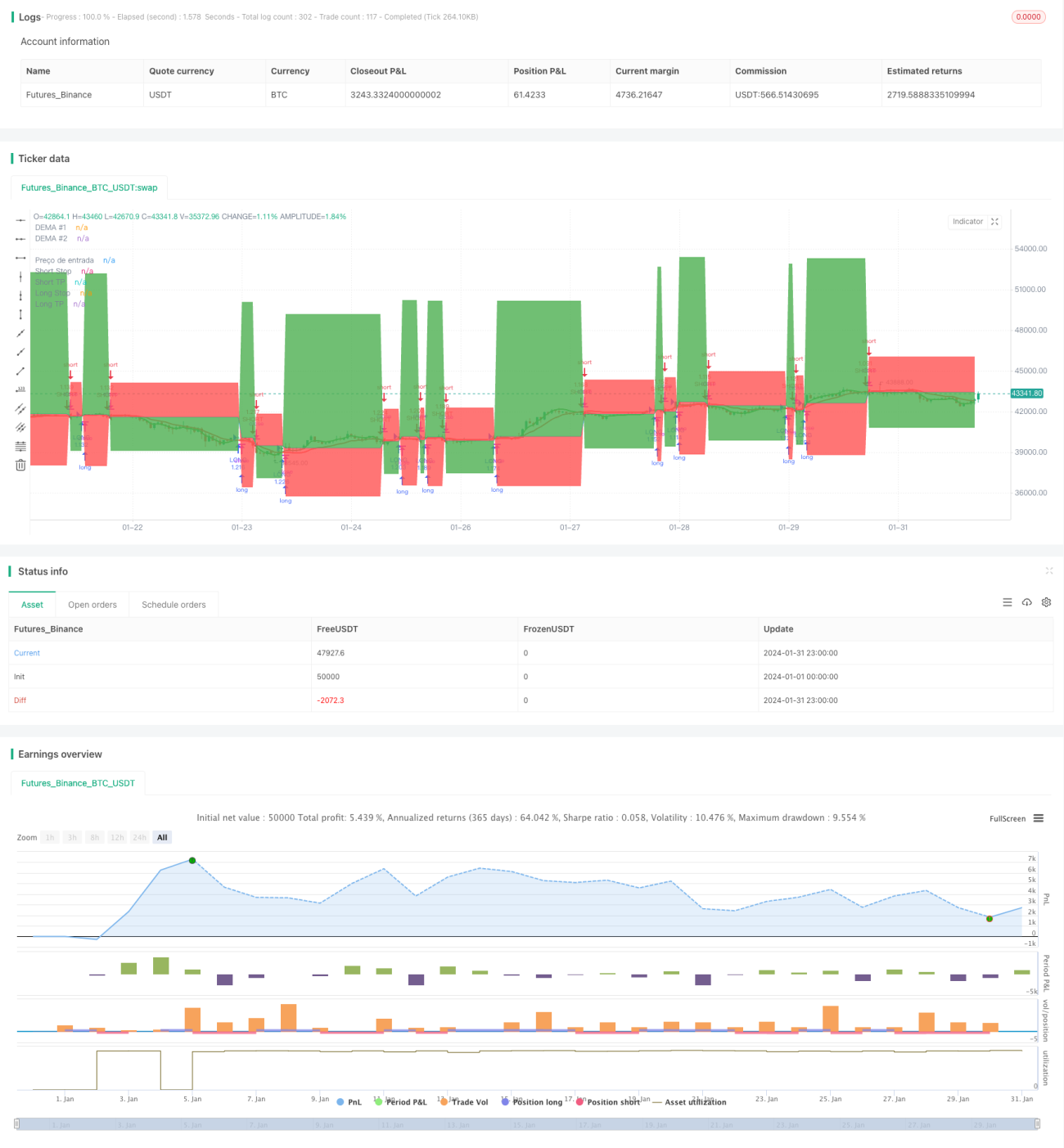

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zeguela

//@version=4

strategy(title="ZEGUELA DEMABOT", commission_value=0.063, commission_type=strategy.commission.percent, initial_capital=100, default_qty_value=90, default_qty_type=strategy.percent_of_equity, overlay=true, process_orders_on_close=true)- 1