Chiến lược siêu xu hướng ba lớp

Tổng quan

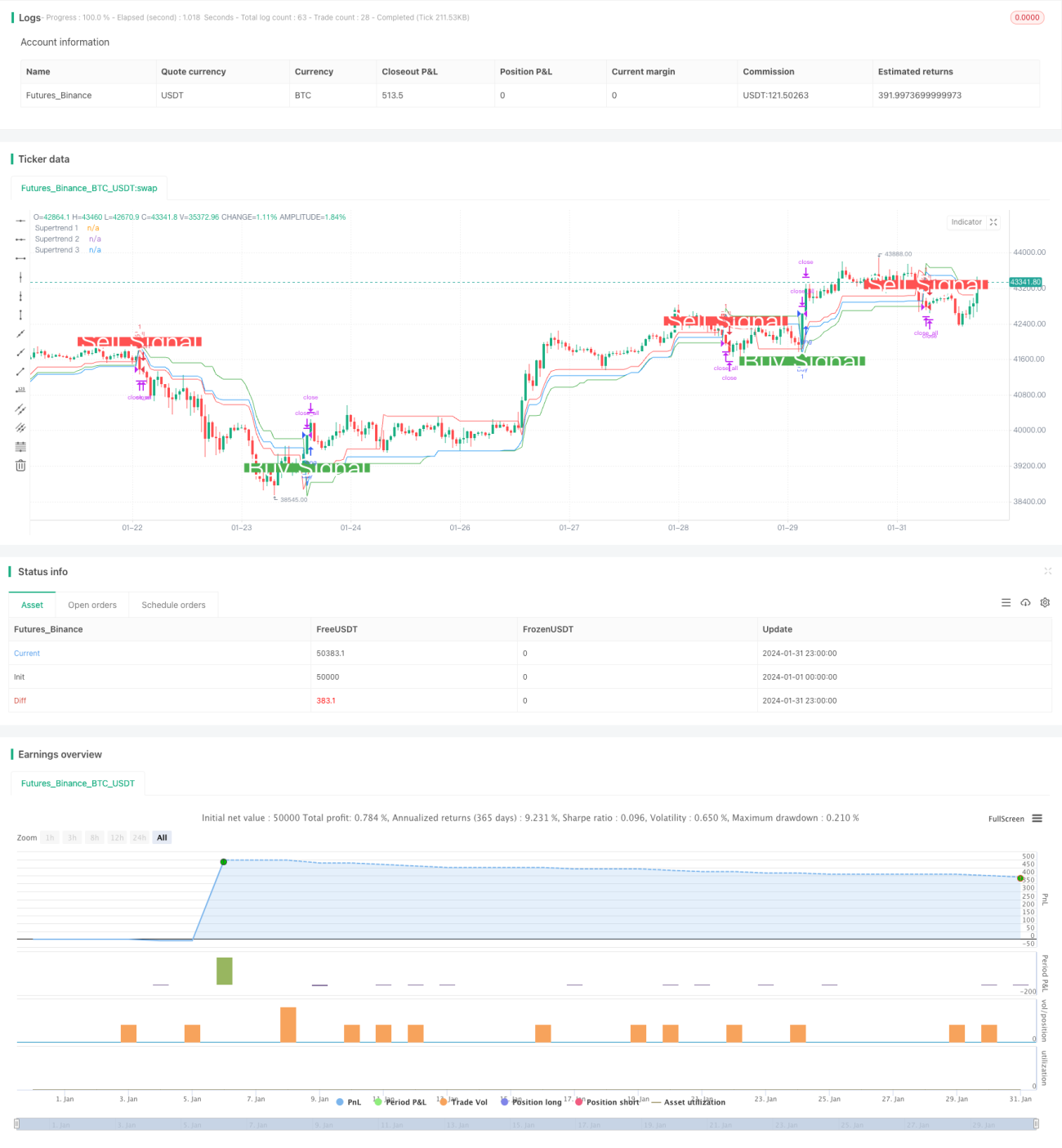

Đây là một chiến lược giao dịch sử dụng chỉ báo SuperTrend ba lớp chồng lên nhau để đưa ra quyết định. Nó có thể nắm bắt các cơ hội xu hướng lớn trong thị trường có xu hướng.

Nguyên lý chiến lược

Chiến lược này sử dụng hàm ta.supertrend() để tính toán ba chỉ báo SuperTrend với các tham số khác nhau. Lần lượt tính SuperTrend 1 với chu kỳ 10 ngày và ATR nhân 3, SuperTrend 2 với chu kỳ 14 ngày và ATR nhân 2, và SuperTrend 3 với chu kỳ 20 ngày và ATR nhân 2.5. Khi giá vượt lên trên cả ba đường SuperTrend, tín hiệu mua được tạo ra. Khi giá phá vỡ xuống dưới cả ba đường SuperTrend, tín hiệu bán được tạo ra.

Chỉ báo SuperTrend kết hợp với chỉ báo ATR có thể theo dõi hiệu quả xu hướng biến động giá. Chiến lược SuperTrend ba lớp chồng lên nhau giúp tín hiệu đáng tin cậy hơn, từ đó thu được lợi nhuận lớn hơn trong thị trường có xu hướng.

Ưu điểm của chiến lược

- Cơ chế lọc ba lớp, tránh tín hiệu giả, nâng cao chất lượng tín hiệu

- Bản thân chỉ báo SuperTrend đã có khả năng khử nhiễu tốt

- Có thể cấu hình nhiều tổ hợp siêu tham số, thích ứng với môi trường thị trường rộng hơn

- Kết quả kiểm tra lịch sử tốt, tỷ lệ lợi nhuận/rủi ro cao

Rủi ro của chiến lược

- Tín hiệu lọc nhiều lớp có thể bỏ lỡ một số cơ hội

- Hiệu suất không tốt trong thị trường đi ngang

- Cần tối ưu hóa tổ hợp ba siêu tham số

- Thời gian giao dịch tập trung dễ bị ảnh hưởng bởi các sự kiện bất ngờ

Có thể xem xét các điểm sau để giảm rủi ro:

- Điều chỉnh điều kiện lọc, giữ lại một hoặc hai SuperTrend

- Thêm chiến lược cắt lỗ

- Tối ưu hóa siêu tham số, nâng cao tỷ lệ thắng

Hướng tối ưu hóa chiến lược

- Kiểm tra thêm nhiều tổ hợp tham số, tìm siêu tham số tối ưu

- Thêm thuật toán học máy, tối ưu hóa tham số theo thời gian thực

- Thêm chiến lược cắt lỗ, kiểm soát lỗ từng lệnh

- Kết hợp với các chỉ báo khác, nhận diện xu hướng và đi ngang

- Mở rộng thời gian giao dịch, tránh rủi ro tại một thời điểm duy nhất

Tổng kết

Chiến lược này đưa ra quyết định thông qua SuperTrend ba lớp chồng lên nhau, có thể nhận diện hiệu quả hướng xu hướng. Nó có ưu điểm như chất lượng tín hiệu cao, có thể tối ưu tham số. Đồng thời cũng tồn tại một số rủi ro nhất định, cần điều chỉnh tham số và thời điểm thoát lệnh để thích ứng với các môi trường thị trường khác nhau. Nhìn chung, chiến lược này hoạt động nổi bật, đáng để nghiên cứu và ứng dụng thêm.

- 1