Chiến lược xu hướng đường trung bình động với trailing stop hai chiều

Tổng quan

Chiến lược này kết hợp sử dụng SuperTrend, SSL Hybrid Baseline Channel và chỉ báo hình thái QQE, để thực hiện theo dõi cắt lỗ cho cả vị thế mua và bán nhằm bắt xu hướng trung và dài hạn.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa trên các điểm sau:

- Sử dụng chỉ báo SuperTrend để xác định hướng xu hướng tổng thể, hỗ trợ xác định thời điểm vào lệnh.

- Dựa trên SSL Hybrid Baseline Channel để xác định điểm vào lệnh cụ thể. Sự phá vỡ kênh là tín hiệu vào lệnh cơ bản.

- Sử dụng giao cắt mua/bán của chỉ báo QQE như tín hiệu xác nhận phụ cho việc vào lệnh.

- Chỉ báo ATR hỗ trợ tính toán mức cắt lỗ và chốt lời.

- Áp dụng quản lý rủi ro theo phần trăm và chiến lược điều chỉnh cắt lỗ động, kiểm soát rủi ro mỗi giao dịch.

Logic vào lệnh: khi SuperTrend đảo chiều và giá phá vỡ đường cơ sở của kênh, đồng thời chỉ báo QQE xảy ra giao cắt theo hướng tương ứng thì mới vào lệnh.

Hệ thống chỉ báo kết hợp này có thể kiểm soát hiệu quả thời điểm vào lệnh, tránh mở lệnh vô ích trong giai đoạn dao động.

Logic thoát lệnh tương đối đơn giản, sử dụng sự đảo chiều của SuperTrend làm tín hiệu đóng lệnh, hoặc khi chạm mức cắt lỗ/chốt lời.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng kết hợp nhiều chỉ báo, giúp lọc hiệu quả các phá vỡ giả, giảm xác suất giao dịch không hiệu quả.

Ngoài ra, việc sử dụng cắt lỗ theo phần trăm để kiểm soát rủi ro mất mát mỗi giao dịch là một điểm nhấn của chiến lược.

Thông qua ATR tính toán mức cắt lỗ, kết hợp với bội số cắt lỗ có thể cấu hình, chúng ta có thể biết rõ rủi ro mỗi giao dịch. Điều này rất quan trọng đối với quản lý rủi ro.

Chúng ta thậm chí có thể đặt phần trăm thua lỗ tối đa chấp nhận được để giới hạn tổn thất tổng thể.

Chiến lược này cũng sử dụng cắt lỗ di động để khóa lợi nhuận, đây cũng là yếu tố then chốt để tăng cường lợi nhuận.

Phân tích rủi ro

Rủi ro lớn nhất của chiến lược này là xác suất tín hiệu kết hợp phát ra tín hiệu sai. Mặc dù chúng ta đã sử dụng bộ lọc kết hợp nhiều chỉ báo, nhưng không có chỉ báo nào có thể hoàn toàn tránh khỏi sai lầm.

Khi SuperTrend xảy ra phá vỡ giả hoặc QQE hình thành tín hiệu sai, chiến lược này dễ dàng vào lệnh xây dựng vị thế, làm tăng rủi ro cắt lỗ bị kích hoạt.

Ngoài ra, chiến lược này cũng đối mặt với rủi ro tối ưu hóa quá mức. Việc thiết lập tham số cần thận trọng, tránh phụ thuộc quá nhiều vào dữ liệu lịch sử.

Chúng ta cần chú ý đến các tham số quan trọng như độ dài ATR, bội số cắt lỗ, phần trăm rủi ro, v.v. Các tham số này cần điều chỉnh riêng cho từng loại sản phẩm.

Hướng tối ưu hóa

Chiến lược này vẫn còn không gian để tối ưu hóa thêm:

- Có thể thử nghiệm kết hợp thêm nhiều chỉ báo, ví dụ như thêm chỉ báo KD vào hỗ trợ đánh giá.

- Có thể thử nghiệm độ ổn định dưới các thiết lập tham số khác nhau.

- Có thể thử nghiệm phương pháp dựa trên học máy để tự động tối ưu hóa tham số.

- Có thể giới thiệu cơ chế cắt lỗ thích ứng, điều chỉnh biên độ cắt lỗ dựa trên mức độ biến động của thị trường.

- Có thể thêm logic vào lệnh lại, tức là vào lệnh lại sau khi cắt lỗ, để giảm thiểu cơ hội bị bỏ lỡ.

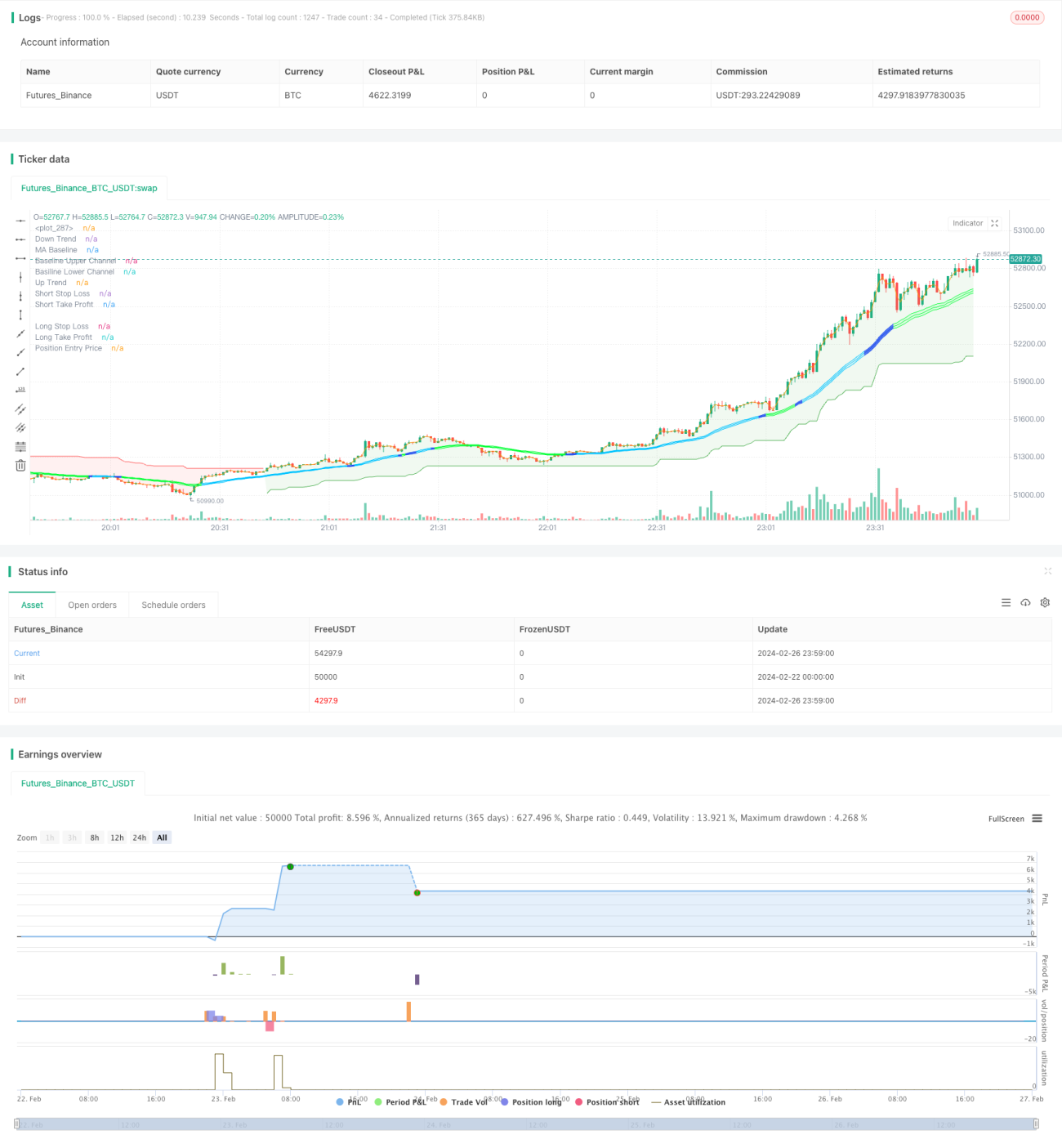

/*backtest

start: 2024-02-22 00:00:00

end: 2024-02-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to W3MCT - @simonFUTURE2 w3mct.com -

// @version=5- 1