Korrektur-Rücksetzer-Kaufstrategie

Übersicht

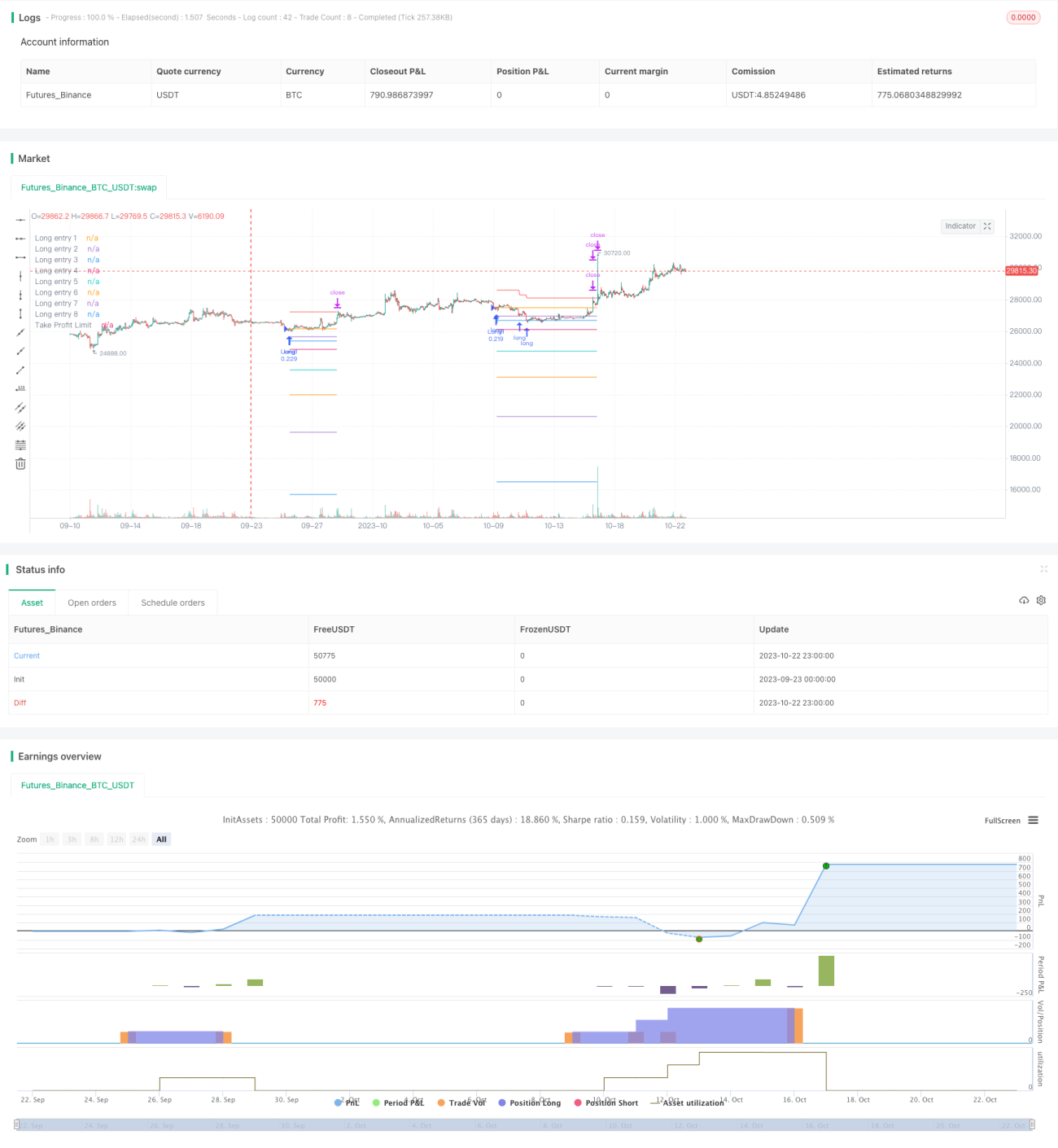

Diese Strategie kombiniert den RSI-Indikator mit einem gleitenden Durchschnitt des Kurses. Wenn der Aktienkurs unter den gleitenden Durchschnitt fällt, wird nach einer überverkauften Gelegenheit gesucht, um eine Long-Position zu eröffnen. Sollte der Kurs weiter fallen, wird die Position schrittweise gemäß vordefinierter Prozentsätze nachgekauft, um die durchschnittlichen Anschaffungskosten zu senken. Sobald die Position einen festgelegten Gewinnprozentsatz erreicht, wird sie geschlossen. Gleichzeitig wird ein progressiver Take-Profit-Mechanismus eingeführt, der basierend auf den bereits realisierten Gewinnen einzelner Teilpositionen den Take-Profit-Preis der Gesamtposition dynamisch anpasst. Dies reduziert das Verlustrisiko effektiv und ermöglicht einen schrittweisen Ausstieg.

Strategieprinzip

-

Wenn der RSI-Indikator unter die überverkaufte Schwelle von 29 fällt und der Schlusskurs unter dem gleitenden Durchschnitt liegt, wird die erste Long-Position eröffnet.

-

Sinkt der Kurs um 2 % gegenüber der ersten Position, wird eine zweite Long-Position nachgekauft; bei einem Rückgang von 3 % erfolgt der dritte Nachkauf, und so weiter bis zu maximal 8 Nachkäufen. Dies bewirkt einen gestaffelten Aufbau der Position.

-

Nach jeder Eröffnung einer Position wird der damalige Eröffnungskurs aufgezeichnet. Diese Kurspunkte dienen als Referenz für den Einstieg. Auf dem Chart werden diese Kurslinien eingezeichnet.

-

Nach der Positionseröffnung wird der durchschnittliche Preis der Gesamtposition berechnet. 3 % dieses Durchschnittspreises dienen als Take-Profit für jede einzelne Teilposition, 4 % als Take-Profit für die gesamte Position.

-

Steigt der Kurs über den Take-Profit-Preis einer Teilposition, wird diese Teilposition geschlossen.

-

Berechnung des progressiven Take-Profits: Bei jedem Schließen einer Teilposition wird der realisierte Gewinn dieser Teilposition vom Take-Profit-Preis der Gesamtposition abgezogen. Dadurch sinkt die Take-Profit-Linie langsam, und erst wenn die Gewinne aller Teilpositionen ausreichen, um den maximalen Verlust zu decken, wird die gesamte Position geschlossen.

-

Sobald der Kurs die progressive Take-Profit-Linie erreicht, wird die gesamte Position geschlossen.

Vorteilsanalyse

-

Der RSI-Indikator kann die überverkaufte Zone relativ genau bestimmen und hilft, Wendepunkte zu erkennen.

-

Mehrfaches gestaffeltes Nachkaufen ermöglicht es, die durchschnittlichen Anschaffungskosten bei niedrigen Kursen zu senken.

-

Der progressive Take-Profit reduziert das Verlustrisiko und ermöglicht einen schrittweisen Ausstieg. Selbst bei Verlusten bleiben diese in einem kontrollierbaren Rahmen.

-

Konfigurierbare Take-Profit- und Nachkauf-Prozentsätze erlauben eine Anpassung des Strategierisikos an den Markt.

-

Die Darstellung der Einstiegs- und Take-Profit-Linien im Chart ermöglicht eine visuelle Beurteilung der Positionsverteilung.

Risikoanalyse

-

In Seitwärtsmärkten können häufig Eröffnungen und Take-Profits ausgelöst werden, was zu erhöhter Handelsaktivität und Slippage-Verlusten führt. Durch eine Anpassung der RSI-Parameter (z. B. großzügigere Schwellen) kann die Handelsfrequenz reduziert werden.

-

Eine ungeeignete Anzahl von Nachkäufen oder unpassende Prozentsätze können zu übermäßigem Handel führen. Die Parameter sollten sorgfältig an die Kapitalausstattung angepasst werden.

-

Falls der Markt weiter fällt und nachgekauft wird, kann dies zu einem unbegrenzten Risiko führen. Daher sollte eine Obergrenze für die Anzahl der Nachkäufe festgelegt werden, und der letzte Nachkauf sollte mit einem konservativen Prozentsatz erfolgen.

-

Ein zu geringer Take-Profit-Prozentsatz kann zu vorzeitigem Gewinnmitnahmen führen. Der geeignete Prozentsatz sollte auf Basis von historischen Backtests ermittelt werden.

Optimierungsmöglichkeiten

-

Es können zusätzliche Indikatoren wie MACD zur Filterung der RSI-Signale eingeführt werden, um ineffektive Trades zu reduzieren.

-

Ein Stop-Loss basierend auf dem ATR (Average True Range) kann implementiert werden, um extreme Verluste bei Ausreißern zu vermeiden.

-

Parameter wie Anzahl der Nachkäufe, Nachkaufprozentsätze und Take-Profit-Prozentsätze können optimiert werden, um die Strategie an verschiedene Anlageklassen anzupassen.

-

Der Take-Profit-Prozentsatz kann dynamisch an die Volatilität angepasst werden – bei hoher Volatilität etwas großzügiger.

Zusammenfassung

Diese Strategie nutzt den RSI-Indikator zur Erkennung von überverkauften Zonen und kombiniert ihn mit einem gleitenden Durchschnitt für Reversal-Trades. Durch intelligente Nachkauf- und progressive Take-Profit-Mechanismen wird unter Risikokontrolle eine effiziente Long-Strategie umgesetzt. Durch Optimierung der Indikatorparameter, des Take-Profit-Mechanismus usw. kann die Strategie stabiler und effizienter gestaltet werden. Die Strategie lässt sich auf eine Vielzahl von Finanzinstrumenten mit Trendwende-Eigenschaften anwenden, wie z. B. Aktienindex-Futures oder Kryptowährungen, und besitzt einen praktischen Anlagewert.

- 1