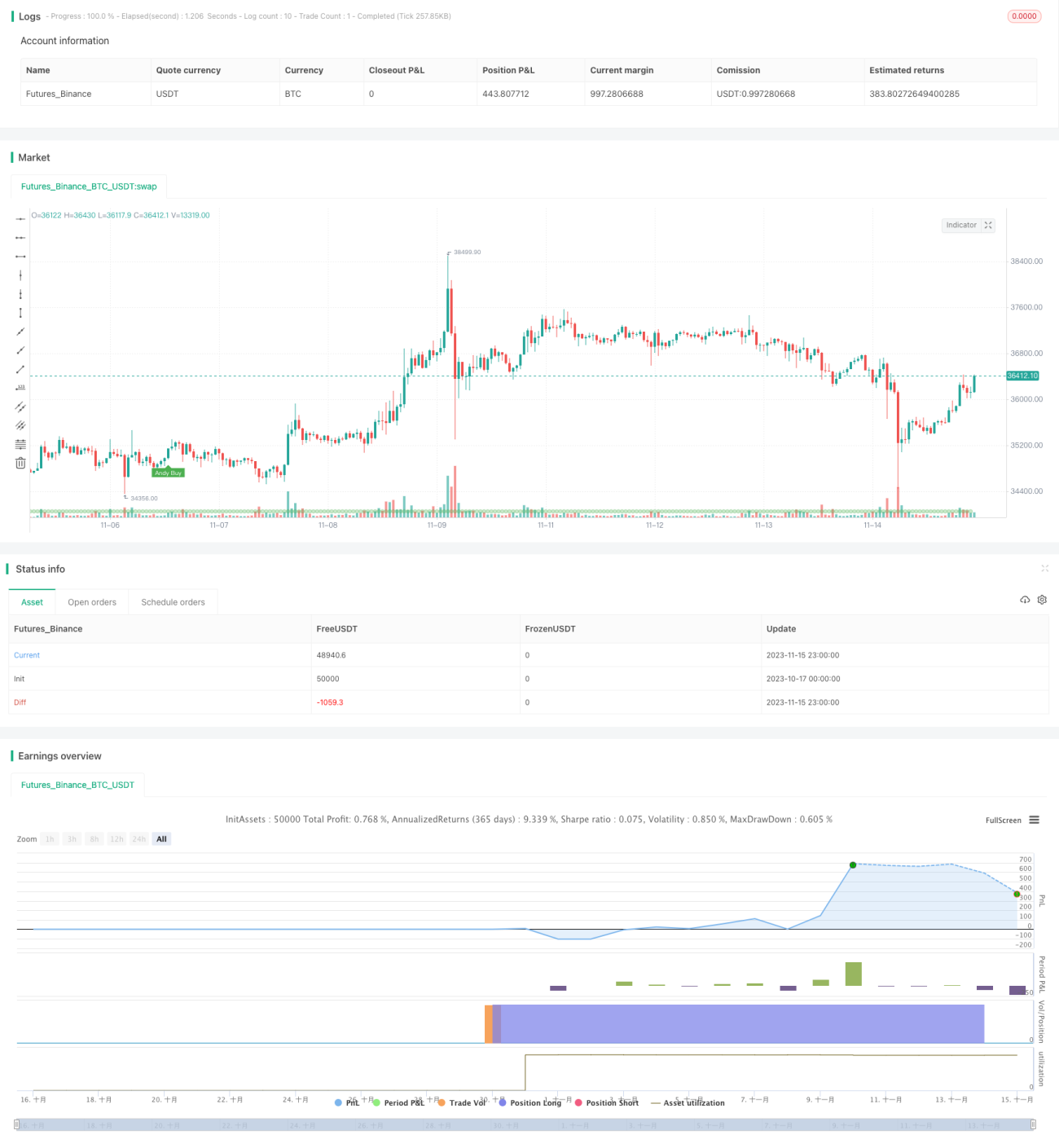

Eine Trendfolgestrategie basierend auf Multi-Timeframe-Momentum-Rotation

Überblick

Diese Strategie verwendet eine Kombination von gleitenden Durchschnitten über verschiedene Zeitrahmen, um Trendrotationen auf den Stunden-, Tages- und Wochencharts zu identifizieren. Sie ermöglicht einen risikoarmen Trendfolgehandel. Die Strategie ist flexibel, einfach umsetzbar, kapital effizient und eignet sich für mittel- bis langfristige Trendtrader.

Funktionsprinzip

Die Strategie verwendet drei gleitende Durchschnitte (5, 20 und 40 Tage), um die Anordnung der Trends auf verschiedenen Zeitrahmen zu bestimmen. Basierend auf dem Prinzip der Trendkonsistenz zwischen großen und kleinen Zeitrahmen werden bullische und bärische Zyklen identifiziert. Konkret wird ein Kreuzen des schnellen 5-Tage-Durchschnitts über den mittleren 20-Tage-Durchschnitt als kurzfristiges Kaufsignal gewertet, und ein Kreuzen des mittleren 20-Tage-Durchschnitts über den langsamen 40-Tage-Durchschnitt als mittelfristiges Kaufsignal. Wenn die drei Durchschnitte positiv ausgerichtet sind (5-Tage > 20-Tage > 40-Tage), wird ein bullischer Zyklus angenommen; bei negativer Ausrichtung (5-Tage < 20-Tage < 40-Tage) wird ein bärischer Zyklus angenommen. Auf diese Weise wird die Richtung aus dem größeren Trend bestimmt und der Einstieg anhand der Stärke des kleineren Zeitrahmens getätigt. Positionen werden nur eröffnet, wenn der Haupttrend gleichgerichtet ist und der kleinere Zeitrahmen stark ist, wodurch falsche Ausbrüche effektiv gefiltert werden und eine hohe Gewinnrate erzielt wird. Darüber hinaus verwendet die Strategie einen ATR-Trailing-Stop zur Kontrolle des Einzelrisikos, was die Rentabilität weiter verbessert.

Vorteile

Flexible Konfiguration: Benutzer können die Parameter der gleitenden Durchschnitte an verschiedene Instrumente und Handelspräferenzen anpassen. Einfache Implementierung: Auch Anfänger können es leicht nutzen. Hohe Kapitaleffizienz: Hebelwirkung kann voll ausgeschöpft werden. Kontrolliertes Risiko: Stopp-Mechanismen vermeiden erhebliche Verluste. Starke Trendfolgefähigkeit: Nach Bestätigung des großen Trends kontinuierliche Gewinne. Hohe Gewinnrate: Gute Signalqualität, weniger Fehlausführungen.

Risiken und Verbesserungen

Die Beurteilung des großen Trends basiert auf der Anordnung der gleitenden Durchschnitte, was zu Verzögerungen und Fehleinschätzungen führen kann. Die Stärkeerkennung im kleinen Zeitrahmen verwendet nur eine einzelne Kerze, was zu vorzeitigen Auslösern führen kann – die Bedingung könnte gelockert werden. Der feste ATR-Stop könnte zu dynamischen Stopps optimiert werden. Zusätzliche Filter wie Volumen könnten hinzugefügt werden. Verschiedene Parameterkombinationen der gleitenden Durchschnitte könnten getestet werden, um die Strategie zu optimieren.

Zusammenfassung

Diese Strategie integriert Multi-Timeframe-Analyse und Risikomanagement, um einen risikoarmen Trendfolgehandel zu ermöglichen. Durch Anpassung der Parameter kann sie an verschiedene Instrumente angepasst werden und die Bedürfnisse von Trendfolgern erfüllen. Im Vergleich zu herkömmlichen Systemen mit nur einem Zeitrahmen sind die Handelsentscheidungen robuster und die Signale effizienter. Insgesamt hat die Strategie eine gute Marktanpassungsfähigkeit und Entwicklungsperspektiven.

Überblick

This strategy uses a combination of moving averages across timeframes to identify trend rotations on the hourly, daily and weekly charts. It allows low-risk trend following trading. The strategy is flexible, simple to implement, capital efficient and suitable for medium-long term trend traders.

Handelslogik

The strategy employs 5, 20 and 40-day moving averages to determine the alignment of trends across different timeframes. Based on the consistency between larger and smaller timeframes, it identifies bullish and bearish cycles. Specifically, the crossing of 5-day fast MA above 20-day medium MA indicates an uptrend in the short term. The crossing of 20-day medium MA above 40-day slow MA signals an uptrend in the medium term. When the fast, medium and slow MAs are positively aligned (5-day > 20-day > 40-day), it is a bull cycle. When they are negatively aligned (5-day < 20-day < 40-day), it is a bear cycle. By determining direction from the larger cycles and confirming strength on the smaller cycles, this strategy opens positions only when major trend and minor momentum align. This effectively avoids false breakouts and achieves high win rate. The strategy also utilizes ATR trailing stops to control single trade risks and further improve profitability.

Vorteile

Flexible configurations to suit different instruments and trading styles; Simple to implement even for beginner traders; High capital efficiency to maximize leverage; Effective risk control to avoid significant losses; Strong trend following ability for sustained profits; High win rate due to robust signals and fewer whipsaws.

Risiken und Verbesserungen

MA crossovers may lag and cause late trend detection; Single candle strength detection could trigger premature entry, relax condition; Fixed ATR stop loss, optimize to dynamic stops; Consider adding supplementary filters like volume; Explore different MA parameters for optimization.

Fazit

This strategy integrates multiple timeframe analysis and risk management for low-risk trend following trading. By adjusting parameters, it can be adapted to different instruments to suit trend traders. Compared to single timeframe systems, it makes more robust trading decisions and generates higher efficiency signals. In conclusion, this strategy has good market adaptiveness and development potential.

- 1