Super Goose Inverse Triangle Moving Average Handelsstrategie

Überblick

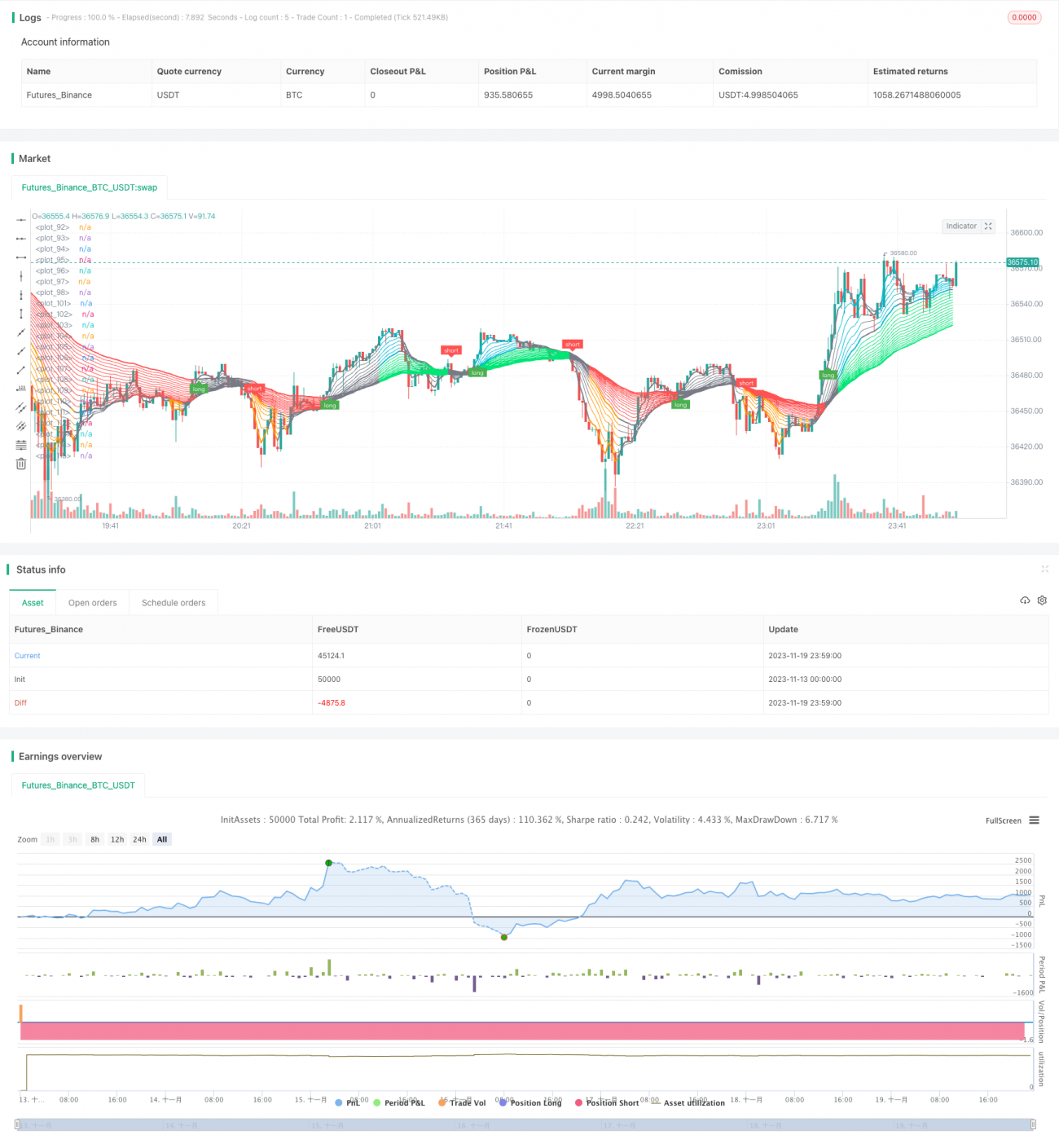

Der Hauptgedanke dieser Strategie ist es, durch die Verwendung mehrerer gleitender Durchschnitte mit unterschiedlichen Perioden ein „Super Goose“-Handelssignal zu erzeugen, um relative langfristige Trendrichtungen zu erkennen. Super Goose besteht aus zwei Gruppen von gleitenden Durchschnitten: schnellen gleitenden Durchschnitten und langsamen gleitenden Durchschnitten. Die schnelle Linie bestimmt den genauen Einstiegspunkt, die langsame Linie bestimmt die allgemeine Handelsrichtung. Wenn die schnelle Linie von unten nach oben durch die langsame Linie kreuzt, wird ein Long-Signal erzeugt; wenn sie von oben nach unten kreuzt, ein Short-Signal.

Prinzip

Die Strategie verwendet mehrere Gruppen von EMA-Linien mit unterschiedlichen Perioden, im Einzelnen:

- Schnelle Linien: 7 Linien mit Perioden von 3, 6, ... 21

- Langsame Linien: Linien mit Perioden von 24, 27, ... 200

Wenn sich die schnellen Linien kreuzen, werden sie blau (aufsteigend) und orange (absteigend) dargestellt; bei Kreuzungen der langsamen Linien werden sie grün (aufsteigend) und rot (absteigend). Wenn die blaue schnelle Linie von grau zu grün (langsame Linie) wechselt, wird ein Long-Signal erzeugt; umgekehrt wird beim Wechsel von grün zu grau die Long-Position geschlossen. Beim Wechsel von grau zu rot entsteht ein Short-Signal.

Die Strategie bietet zwei Modi: Der stabile Modus handelt nur, wenn sowohl schnelle als auch langsame EMA eine Richtung bestätigt haben; der aggressive Modus erzeugt bereits bei jeder Richtungsänderung der schnellen EMA ein Signal.

Vorteile

Diese Strategie vereint die Vorteile eines dualen gleitenden Durchschnittssystems. Sie kann sowohl zeitnah Handelsmöglichkeiten in kürzeren Zyklen erfassen als auch durch die langsameren Linien übermäßige Fehlsignale herausfiltern. Die spezifischen Vorteile sind:

- Die Kombination von schnellen und langsamen EMA-Linien ermöglicht eine effektive Risikokontrolle.

- Der aggressive Modus kann kurzfristige Chancen zeitnah erfassen.

- Der stabile Modus bietet Gelegenheiten mit hoher Wahrscheinlichkeit und einem guten Risiko-Ertrags-Verhältnis.

- Großer Spielraum für manuelle Parameteroptimierung.

Risiken

Die Strategie birgt auch einige Risiken:

- In stark schwankenden Märkten kann es zu längeren Zeiträumen der Marktexposition kommen.

- Das System mit mehreren gleitenden Durchschnitten erschwert die Parameteroptimierung und das Testen.

- Im stabilen Modus können Gewinne aufgrund der Verzögerungseigenschaften der schnellen EMA-Linien verloren gehen.

Durch geeignete Anpassung der Parameterkombinationen der schnellen und langsamen EMA oder durch das Setzen von Stop-Loss können diese Risiken kontrolliert werden.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen optimiert werden:

- Hinzufügen eines volatilitätsbasierten Stop-Loss. Dadurch können Verluste nach einzelnen starken Ausschlägen effektiv begrenzt werden.

- Einsatz von maschinellen Lernalgorithmen zur Optimierung der EMA-Parameter. Dies kann die Parametereffizienz erheblich steigern.

- Hinzufügen eines Filters aus Volumen und Preis. Dadurch können die tatsächlichen Handelsmöglichkeiten erhöht werden.

- Erkundung von Kombinationen anderer Indikatoren mit EMA-Kreuzen. Auf diese Weise könnte die Handelsgenauigkeit weiter gesteigert werden.

Zusammenfassung

Die Super-Goose-Strategie berücksichtigt mehrere Zeitrahmenfaktoren und verbessert die Gewinnchancen bei gleichzeitiger Risikokontrolle. Sie kann auf verschiedene Weise optimiert und verbessert werden und ist für quantitative Trader eine eingehende Untersuchung wert.

/*backtest

start: 2023-11-13 00:00:00

end: 2023-11-20 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// A strategized version Daryl Guppy Super EMA's with additional options

// by default "early signals" is enabled, which will trade any green/gray or red/gray transitions of the guppy. Disable to only take longs while green, and shorts while red.

//@version=4- 1