Geduldige Verfolgung von Trendfolgestrategien

Überblick

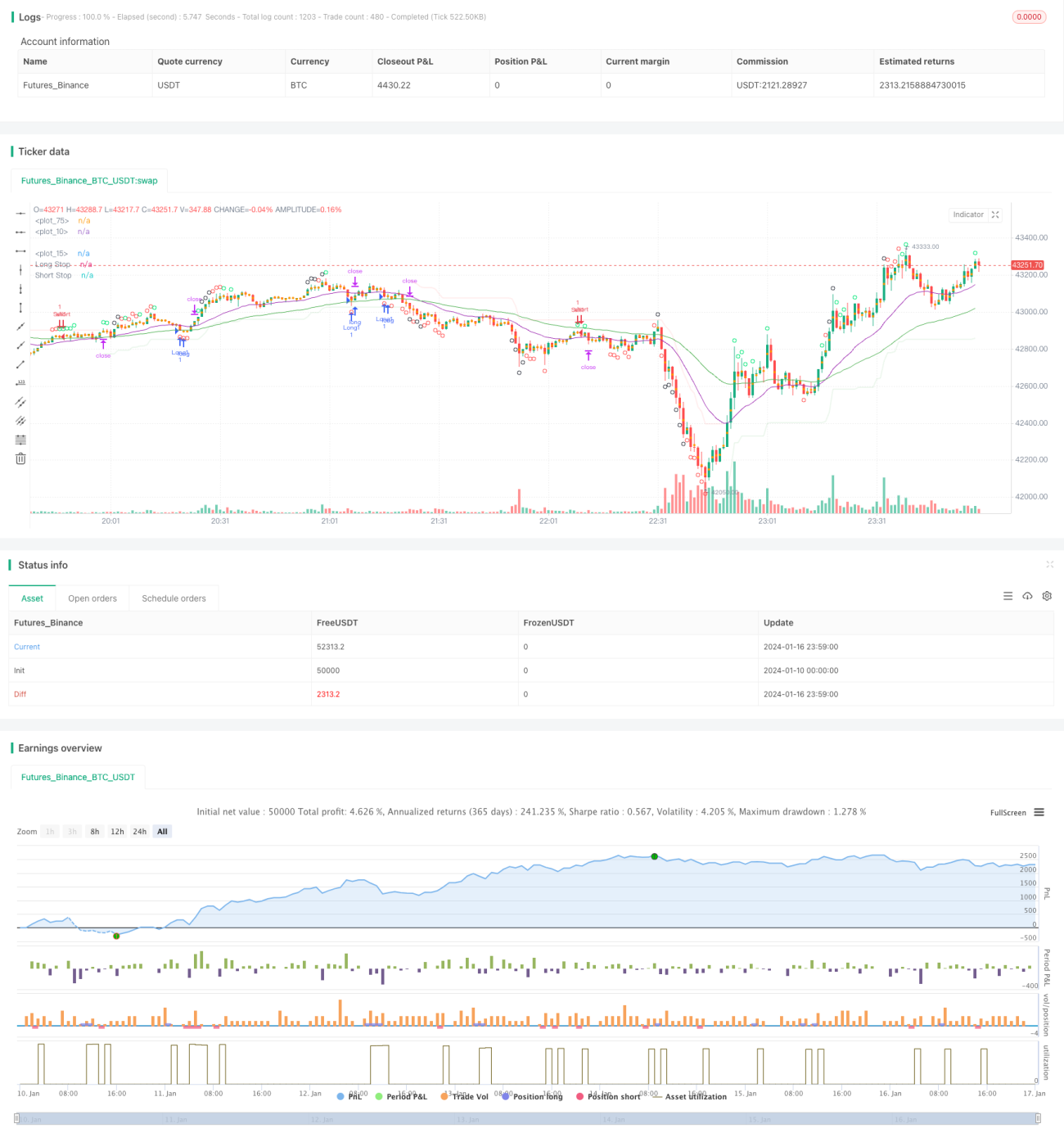

Die Patient-Trend-Tracking-Strategie ist eine trendfolgende Strategie. Sie nutzt eine Kombination aus gleitenden Durchschnitten zur Bestimmung der Trendrichtung und verwendet den CCI-Indikator (überkauft/überverkauft) zur Generierung von Handelssignalen. Die Strategie verfolgt den großen Trend und kann in Seitwärtsmärkten effektiv vor falschen Ausbrüchen schützen.

Funktionsweise der Strategie

Die Strategie verwendet eine Kombination aus 21-Perioden- und 55-Perioden EMA zur Bestimmung der Trendrichtung. Wenn der kurzfristige EMA über dem langfristigen EMA liegt, wird ein Aufwärtstrend definiert; liegt der kurzfristige EMA unter dem langfristigen EMA, wird ein Abwärtstrend definiert.

Der CCI-Indikator wird verwendet, um überkaufte oder überverkaufte Bedingungen zu identifizieren. Ein Aufwärtskreuzen der -100-Linie durch den CCI ist ein überverkauftes Signal am Boden; ein Abwärtskreuzen der +100-Linie ist ein überkauftes Signal am Gipfel. Basierend auf den verschiedenen CCI-Überkauft/-Überverkauft-Linien hat die Strategie drei Stufen der Signalstärke.

Wenn ein Aufwärtstrend identifiziert wurde und der CCI ein starkes überverkauftes Signal am Boden liefert, wird eine Long-Position eröffnet. Wenn ein Abwärtstrend identifiziert wurde und der CCI ein starkes überkauftes Signal am Gipfel liefert, wird eine Short-Position eröffnet.

Der Stop-Loss wird auf den SuperTrend-Indikator gesetzt, das Take-Profit-Ziel wird als feste Punktzahl definiert.

Vorteilsanalyse

Die Strategie bietet hauptsächlich folgende Vorteile:

- Verfolgung großer Trends, Vermeidung falscher Ausbrüche

- Der CCI-Indikator kann Umkehrpunkte effektiv identifizieren

- Der SuperTrend-Stop-Loss ist sinnvoll eingestellt

- Fester Stop-Loss und fester Take-Profit, das Risiko ist kontrollierbar

Risikoanalyse

Die Strategie birgt hauptsächlich folgende Risiken:

- Wahrscheinlichkeit einer Fehleinschätzung des großen Trends

- Wahrscheinlichkeit von Fehlsignalen des CCI-Indikators

- Wahrscheinlichkeit unnötiger Stopps durch zu enge oder zu weite Stop-Loss-Punkte

- Wahrscheinlichkeit, dass der feste Take-Profit eine fortlaufende Trendverfolgung zur Gewinnmitnahme verhindert

Diesen Risiken kann durch die Anpassung der EMA-Periodenparameter, CCI-Parameter sowie der Stop-Loss- und Take-Profit-Punkte begegnet werden. Auch die Einbeziehung weiterer Indikatoren zur Bestätigung der Strategie ist sinnvoll.

Optimierungsrichtungen

Die Hauptoptimierungsrichtungen für diese Strategie sind:

- Testen weiterer Indikatorenkombinationen zur Verbesserung der Trendbestimmung und Signalbestätigung.

- Einsatz eines dynamischen ATR-basierten Stop-Loss und Take-Profit, um den Trend besser zu verfolgen und Risiken zu kontrollieren.

- Einführung eines maschinellen Lernmodells, das auf historischen Daten trainiert wurde, um die Trendwahrscheinlichkeit einzuschätzen.

- Anpassung und Optimierung der Parameter für verschiedene Instrumente.

Zusammenfassung

Die Patient-Trend-Tracking-Strategie ist insgesamt ein sehr praktischer Trendfolgeansatz. Sie nutzt gleitende Durchschnitte zur Bestimmung der großen Trendrichtung, den CCI-Indikator zur Identifizierung von Umkehrpunkten und setzt einen angemessenen SuperTrend-Stop-Loss. Durch Parameteranpassung und die Kombination mehrerer Indikatoren zur Bestätigung kann diese Strategie weiter optimiert werden und ist eine langfristige Live-Betrachtung und -Verifizierung wert.

- 1