Quantitative Strategie: MA-Trendfolge für Stärke und Schwäche

Überblick

Diese Strategie bewertet die Stärke des Markttrends, indem sie die Stärke gleitender Durchschnitte (MA) über mehrere Zeiträume berechnet, um den Trend zu erkennen und zu verfolgen. Wenn der kurzfristige MA-Indikator kontinuierlich ansteigt, wird eine hohe Punktzahl vergeben, die den "MA-Stärke"-Indikator bildet. Wenn dieser Indikator seinen eigenen langfristigen MA überschreitet, wird ein Kaufsignal generiert. Die Strategie kann mit verschiedenen Kombinationen von kurzen und langen MAs konfiguriert werden, um Trends unterschiedlicher Zyklen zu verfolgen.

Strategieprinzip

- Es werden mehrere MAs wie 5-Tage, 10-Tage, 20-Tage usw. berechnet. Es wird beurteilt, ob der Preis jeden MA nach oben durchbricht. Bei einem Durchbruch wird ein Punkt vergeben, die Punkte summieren sich zur "MA-Stärke".

- Auf die "MA-Stärke" wird ein gleitender Durchschnitt angewendet, um einen Durchschnittslinien-Indikator zu bilden. Die bullische/bärische Ausrichtung der Durchschnittslinie wird bewertet, um Handelssignale zu generieren.

- Parameter für die verfolgten Zyklen sind konfigurierbar: Anzahl der kurzfristigen MAs, Periode des langfristigen gleitenden Durchschnitts, Eröffnungsbedingungen usw.

Die Strategie bewertet hauptsächlich die bullische/bärische Ausrichtung des Durchschnittslinien-Indikators, der die durchschnittliche Stärke der MA-Gruppe widerspiegelt. Die MA-Gruppe bewertet konzentriert die Trendrichtung und -stärke, während der Durchschnittslinien-Indikator die Nachhaltigkeit beurteilt.

Vorteilsanalyse

- Mehrdimensionales Modell zur Bewertung der Trendstärke. Ein einzelner MA kann die ausreichende Stärke nicht bestimmen; diese Strategie misst mehrere MA-Durchbrüche, um sicherzustellen, dass die Stärke ausreicht, bevor ein Signal ausgegeben wird – hohe Zuverlässigkeit.

- Konfigurierbare Verfolgungszyklen. Die Anpassung der kurzfristigen MA-Parameter ermöglicht das Erfassen von Trends unterschiedlicher Niveaus; die Anpassung der langfristigen MA-Parameter steuert den Ausstiegsrhythmus. Benutzer können die Zyklen je nach Markt anpassen.

- Nur Long-Positionen vermeiden Fehlentscheidungen in Abwärtsbewegungen und folgen langfristigen Aufwärtstrends. Die Strategie geht nur long, verfolgt Aufwärtstrends ohne Abwärtstrends und kann Verluste durch Trendumkehr reduzieren.

Risikoanalyse

- Risiko von Drawdowns. Wenn die kurzfristige Durchschnittslinie die langfristige Durchschnittslinie unterschreitet, besteht ein erhebliches Drawdown-Risiko. Dies kann durch Stop-Loss-Maßnahmen zur Begrenzung einzelner Verluste reduziert werden.

- Umkehrrisiko. Da der Markt langfristig zwangsläufig Korrekturen durchläuft, muss die Strategie rechtzeitig stoppen und aussteigen. Es wird empfohlen, Wellen- und Kanaltechniken zu kombinieren, um das Ende großer Zyklen zu erkennen und das Umkehrrisiko zu kontrollieren.

- Parameterrisiko. Ungeeignete Parametereinstellungen können zu falschen Signalen führen. Parameter sollten an verschiedene Instrumente angepasst werden, um Stabilität zu gewährleisten.

Optimierungsmöglichkeiten

- Kombination mit weiteren Indikatoren zur Filterung von Einstiegssignalen. Die Einbeziehung des Volumens kann Signale unter Bestätigung der Volumenkraft ausgeben und falsche Ausbrüche vermeiden.

- Hinzufügen von Stop-Loss-Methoden. Nachziehende Stop-Loss- oder kurvenbasierte Stop-Loss können Verluste in Korrekturen reduzieren. Auch Take-Profit-Methoden können in Betracht gezogen werden, um Gewinne zu sichern und Umkehrungen zu vermeiden.

- Berücksichtigung von Futures- und Devisenprodukten. MA-Durchbrüche eignen sich besser für Trendinstrumente. Die Parameterstabilität für verschiedene Futures-Produkte kann bewertet werden, um das beste Instrument auszuwählen.

Zusammenfassung

Diese Strategie beurteilt den Preistrend durch die Berechnung des MA-Stärke-Indikators und verwendet den Crossover der Durchschnittslinien als Signalquelle zur Trendverfolgung. Der Vorteil der Strategie liegt in der genauen Bewertung der Trendstärke bei hoher Zuverlässigkeit. Hauptrisiken sind Trendumkehrungen und Parameteranpassungen. Durch Optimierung der Signaleingangsgenauigkeit, Hinzufügen von Stop-Loss-Methoden und Auswahl geeigneter Instrumente können gute Renditen erzielt werden.

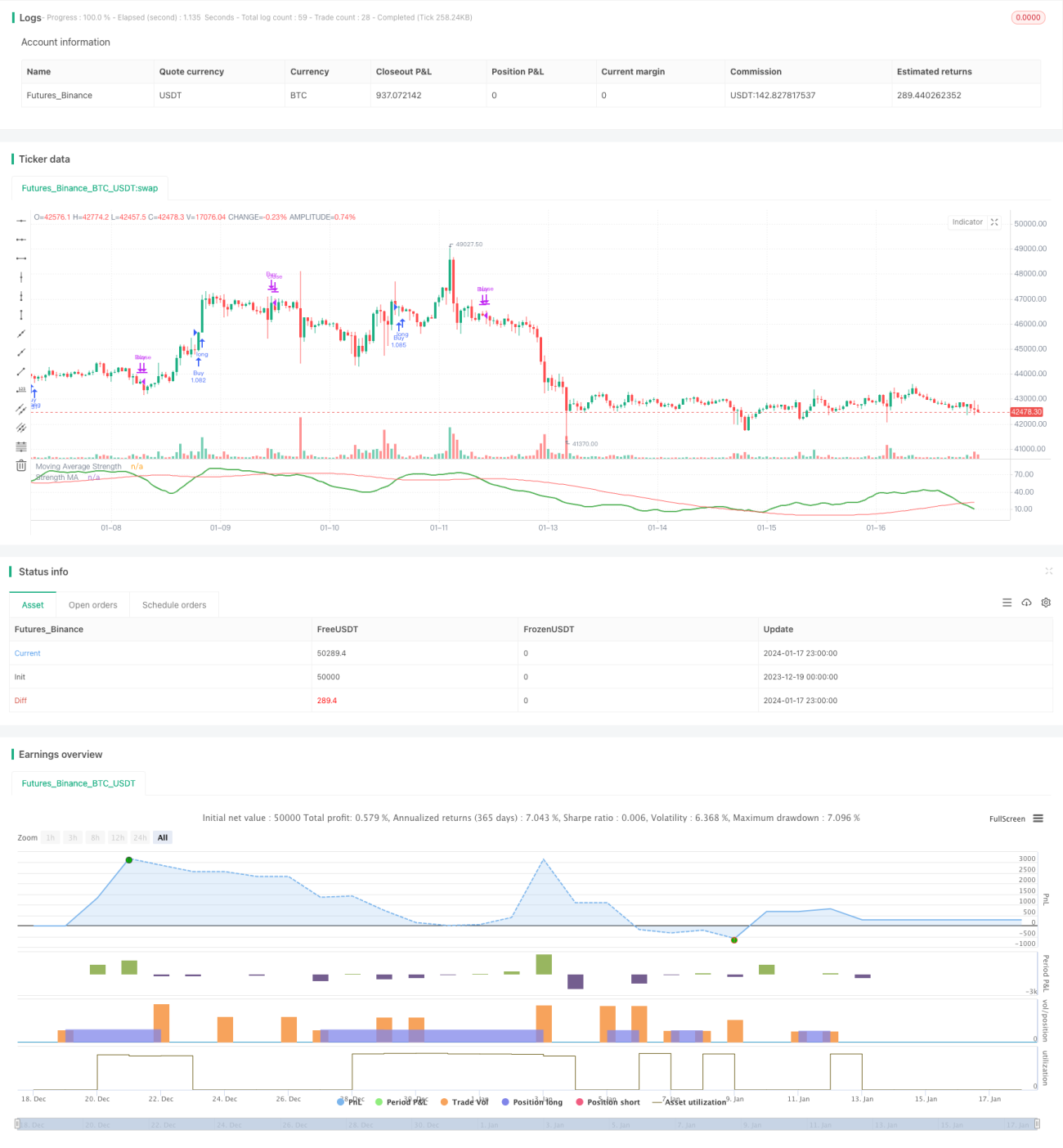

/*backtest

start: 2023-12-19 00:00:00

end: 2024-01-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1