MACD-Handelsstrategie mit bidirektionaler Optimierung

II. Strategieübersicht

Diese Strategie nutzt den MACD-Indikator sowie die Kreuzungsprinzipien gleitender Durchschnitte zur Generierung von Handelssignalen. Ihr Vorteil liegt darin, dass die MACD-Parameter für Long- und Short-Positionen separat optimiert werden können, sodass die Parameter für verschiedene Marktrichtungen optimal konfiguriert werden.

III. Strategieprinzip

- Berechnung der MACD-Indikatoren für Long- und Short-Richtungen. Long verwendet einen Parametersatz, Short einen anderen, die frei konfiguriert werden können.

- Die Kreuzung der MACD-Linie und der Signallinie erzeugt Handelssignale. Bei Long wird ein bullischer Cross verwendet, bei Short ein bärischer Cross.

- Es kann konfiguriert werden, ob auch die Signallinie kreuzen muss, um ein Signal auszulösen, um so Fehlsignale zu vermeiden.

- Nach Eingehen einer Long- oder Short-Position wird auf den entgegengesetzten Cross gewartet, um die Position zu schließen.

IV. Strategievorteile

- Bidirektionale Parameteroptimierung: Die Long- und Short-Parameter können frei optimiert werden, um sie jeweils optimal an die Marktrichtung anzupassen.

- Konfigurierbare Signalglättung: Der Signalparameter kann die Glättung der Signallinie steuern und Fehlsignale filtern.

- Konfigurierbare Signalfilterung: Es kann eingestellt werden, ob ein Cross der Signallinie erforderlich ist, um Fehlsignale zu vermeiden.

- Feinabstimmung der Positionskontrolle: Long oder Short können einzeln oder gleichzeitig aktiviert werden.

V. Strategierisiken

- MACD-Verzögerungsproblem: Der MACD selbst hat eine gewisse Verzögerung und kann schnelle Umkehrungen verpassen.

- Long/Short-Umschaltrisiko: Bei schnellen Marktveränderungen kann der Positionswechsel zu häufig erfolgen.

- Parameterrisiko: Eine ungeeignete Parametereinstellung kann die Marktcharakteristiken nicht erfassen.

- Stop-Loss-Schutz: Es sollten angemessene Stop-Loss-Limits gesetzt werden, um Einzelverluste zu begrenzen.

Methoden zur Risikosteuerung:

- Kombination mit anderen Indikatoren zur Beurteilung des Gesamttrends, um nicht dem Markt hinterherzulaufen.

- Einstellung von Signalverzögerung und Glättungsparametern zur Reduzierung von Fehlsignalen.

- Wiederholtes Testen und Optimieren der Parameter, um sie an die Taktung verschiedener Zeiträume anzupassen.

- Festlegung von Stop-Loss- und Take-Profit-Mechanismen zur Begrenzung von Einzelverlusten.

VI. Optimierungsrichtungen

Die Strategie kann in folgenden Bereichen optimiert werden:

- Testen verschiedener Parameterkombinationen für schnelle und langsame Linien, um die optimalen Parameter für verschiedene Zeiträume zu finden.

- Testen verschiedener Signalparameter; ein glatteres Signal kann mehr Rauschen herausfiltern.

- Testen der Unterschiede bei aktiviertem/deaktiviertem Signallinien-Cross-Filter, um das beste Gleichgewicht zu finden.

- Festlegen optimaler Stop-Loss- und Take-Profit-Verhältnisse basierend auf Backtest-Ergebnissen.

- Versuchen, nur Long oder nur Short zu handeln, um zu sehen, ob die Strategieeffektivität maximiert werden kann.

VII. Zusammenfassung

Diese MACD-bidirektionale Optimierungsstrategie erreicht durch separate Konfiguration der Long- und Short-Parameter eine Optimierung für verschiedene Marktrichtungen und ermöglicht eine freie Anpassung der teilnehmenden Richtungen. Gleichzeitig wird ein Signalfiltermechanismus hinzugefügt, um Fehlsignale zu vermeiden. Durch Parameteroptimierung und Risikomanagementmaßnahmen kann die Strategieeffektivität weiter verbessert werden.

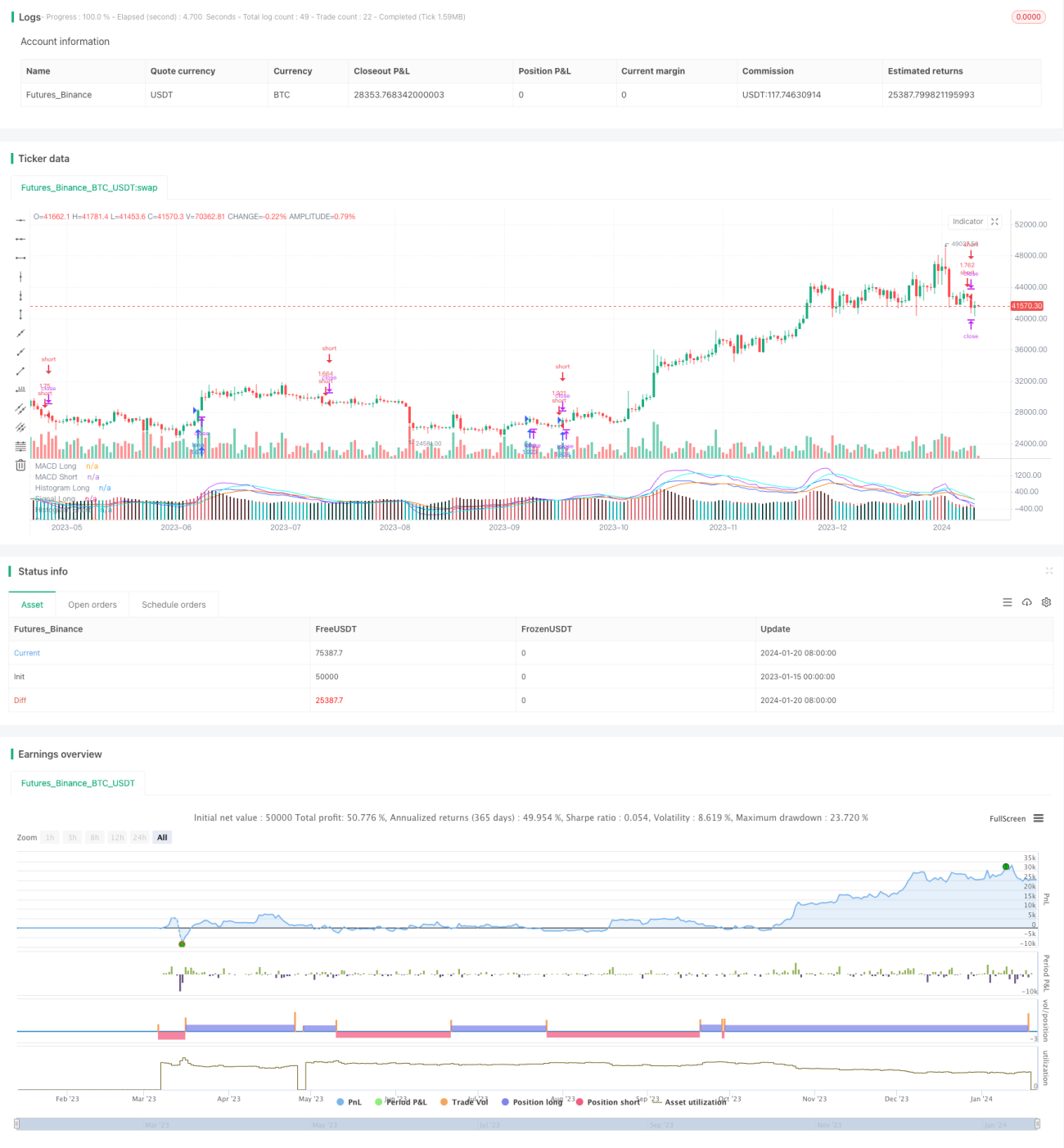

/*backtest

start: 2023-01-15 00:00:00

end: 2024-01-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Gentleman-Goat & TradingTools.Software/Optimizer

strategy(title="MACD Short/Long Strategy for TradingView Input Optimizer", shorttitle="MACD Short/Long TVIO", initial_capital=1000, default_qty_value=100, default_qty_type=strategy.percent_of_equity)- 1