Eine Strategie, die mehrere technische Indikatoren für den quantitativen Handel nutzt.

Überblick

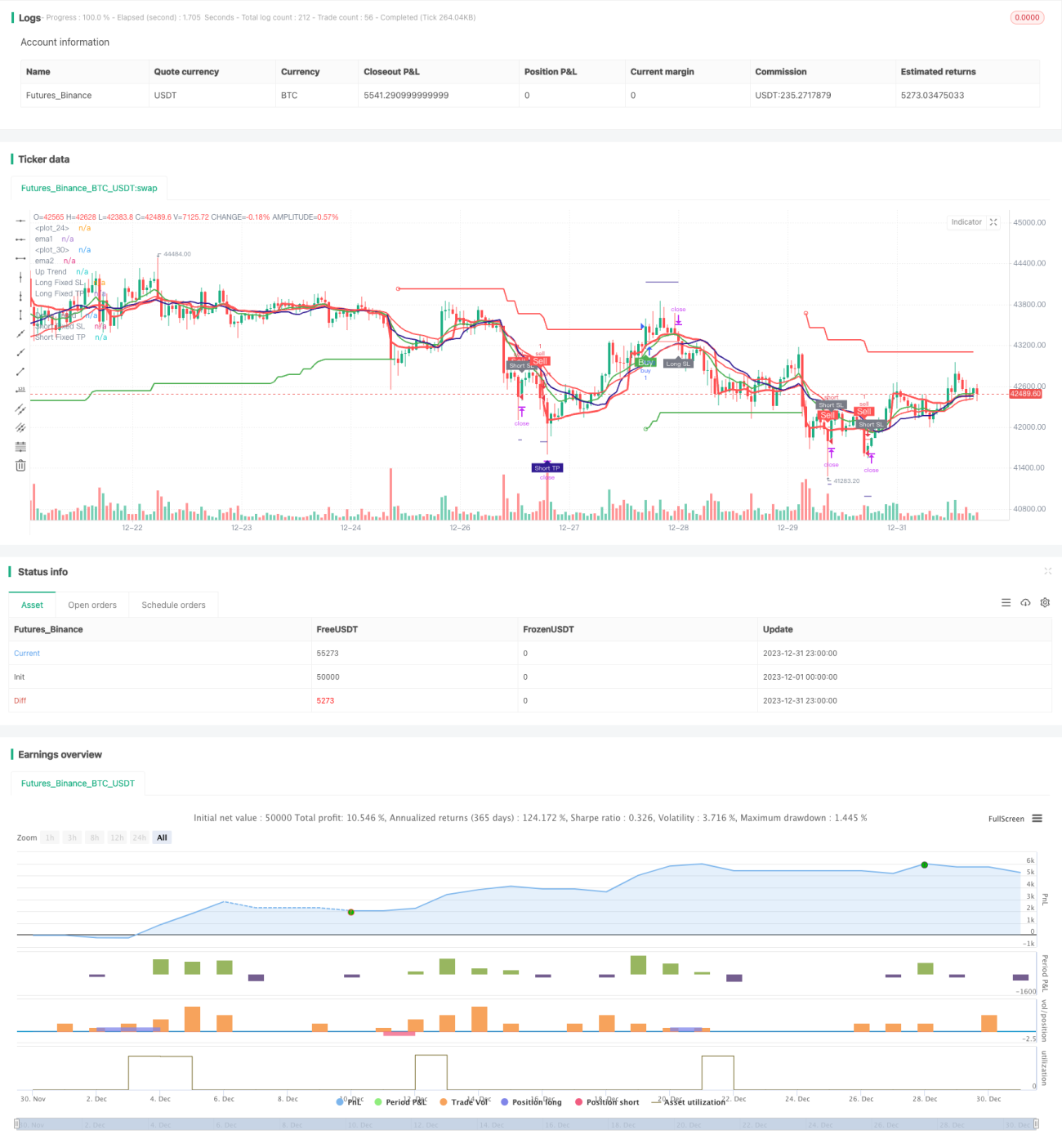

Diese Strategie ist eine quantitative Handelsstrategie, die mehrere technische Indikatoren nutzt. Hauptsächlich werden EMA-Gleitendurchschnittskreuze, der SuperTrend-Indikator, der RSI-Indikator und der MACD-Indikator kombiniert, um Handelssignale zu generieren.

Strategieprinzip

Die Kernlogik der Strategie basiert auf den folgenden Aspekten:

-

EMA-Gleitendurchschnittskreuz: Berechnung der schnellen Linie EMA1 und der langsamen Linie EMA2. Wenn die schnelle Linie die langsame Linie von unten nach oben kreuzt, wird ein Kaufsignal generiert; bei einem Kreuz von oben nach unten entsteht ein Verkaufssignal.

-

VWMA-Gleitendurchschnitt: Berechnung des VWMA-Gleitendurchschnitts. Ein Kaufsignal entsteht, wenn der Schlusskurs diesen Gleitendurchschnitt von unten nach oben durchbricht, ein Verkaufssignal beim Durchbruch von oben nach unten.

-

SuperTrend-Indikator: Basierend auf dem ATR und dem Multiplikatorparameter werden die obere und untere Bande des SuperTrend berechnet, um die Trendrichtung zu bestimmen. In einem Aufwärtstrend wird ein Kaufsignal generiert, in einem Abwärtstrend ein Verkaufssignal.

-

RSI-Indikator: Berechnung des RSI. Wenn der RSI über die Überkauft-Linie steigt, wird ein Verkaufssignal generiert; wenn der RSI unter die Überverkaufszone fällt, ein Kaufsignal.

-

MACD-Indikator: Berechnung der schnellen Linie, langsamen Linie und Signallinie des MACD. Ein Kaufsignal entsteht, wenn die schnelle Linie die Signallinie von unten nach oben kreuzt, ein Verkaufssignal beim Kreuz von oben nach unten.

Nachdem die Signale der oben genannten Indikatoren vorliegen, verwendet die Strategie die UND-Logik, um endgültige Kauf- und Verkaufssignale zu generieren – nur wenn mehrere Indikatoren gleichzeitig ein Signal senden, wird gehandelt.

Vorteile der Strategie

Diese Strategie kombiniert mehrere Indikatoren zur Marktbeurteilung und reduziert effektiv Fehlsignale. Hauptvorteile:

-

Durch die Kombination mehrerer Indikatoren als Filter werden Einzelfehlsignale reduziert.

-

Die Kombination von Trendindikatoren und Oszillatoren ermöglicht zusätzliche Gewinne in Trendmärkten.

-

Eine ausgefeilte Stop-Loss-Logik begrenzt den maximalen Verlust pro Trade.

-

Die Martingale-artige Positionserhöhung ermöglicht nach Verlusten eine Chance auf Erholung.

Risiken der Strategie

Die Strategie birgt folgende Hauptrisiken:

-

Die Kombination mehrerer Indikatoren kann zu konservativ sein und Handelsmöglichkeiten verpassen. Eine Vereinfachung der Indikatorkombination wäre denkbar.

-

Die Martingale-artige Nachkauflogik kann Verluste vergrößern. Die Anzahl der Nachkäufe sollte sinnvoll begrenzt werden.

-

Eine falsche Platzierung des Stop-Loss kann zu unnötigen Auslösungen führen. Ein adaptiver Stop-Loss sollte implementiert werden.

-

Falsche Indikatorparameter können zu vielen Fehlsignalen führen. Eine Optimierung der Parameter ist erforderlich.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen weiter verbessert werden:

-

Bewertung verschiedener Parameterkombinationen der Indikatoren und Auswahl der Gewichtung.

-

Testen unterschiedlicher Indikatorparametereinstellungen.

-

Hinzufügen einer adaptiven Stop-Loss-Logik.

-

Integration eines dynamischen Positionsgrößenmanagements.

-

Einsatz von maschinellem Lernen zur Optimierung von Parametern und Modellen.

Zusammenfassung

Insgesamt handelt es sich um eine sehr praktische quantitative Handelsstrategie. Sie vereint die Vorteile mehrerer klassischer technischer Indikatoren und ermöglicht eine effektive Marktbeurteilung. Durch Parameteroptimierung und Modelliteration kann die Strategie bessere Handelsergebnisse erzielen.

- 1