Auf Wave Trend und VWMA basierende quantitative Trendfolgestrategie

Übersicht

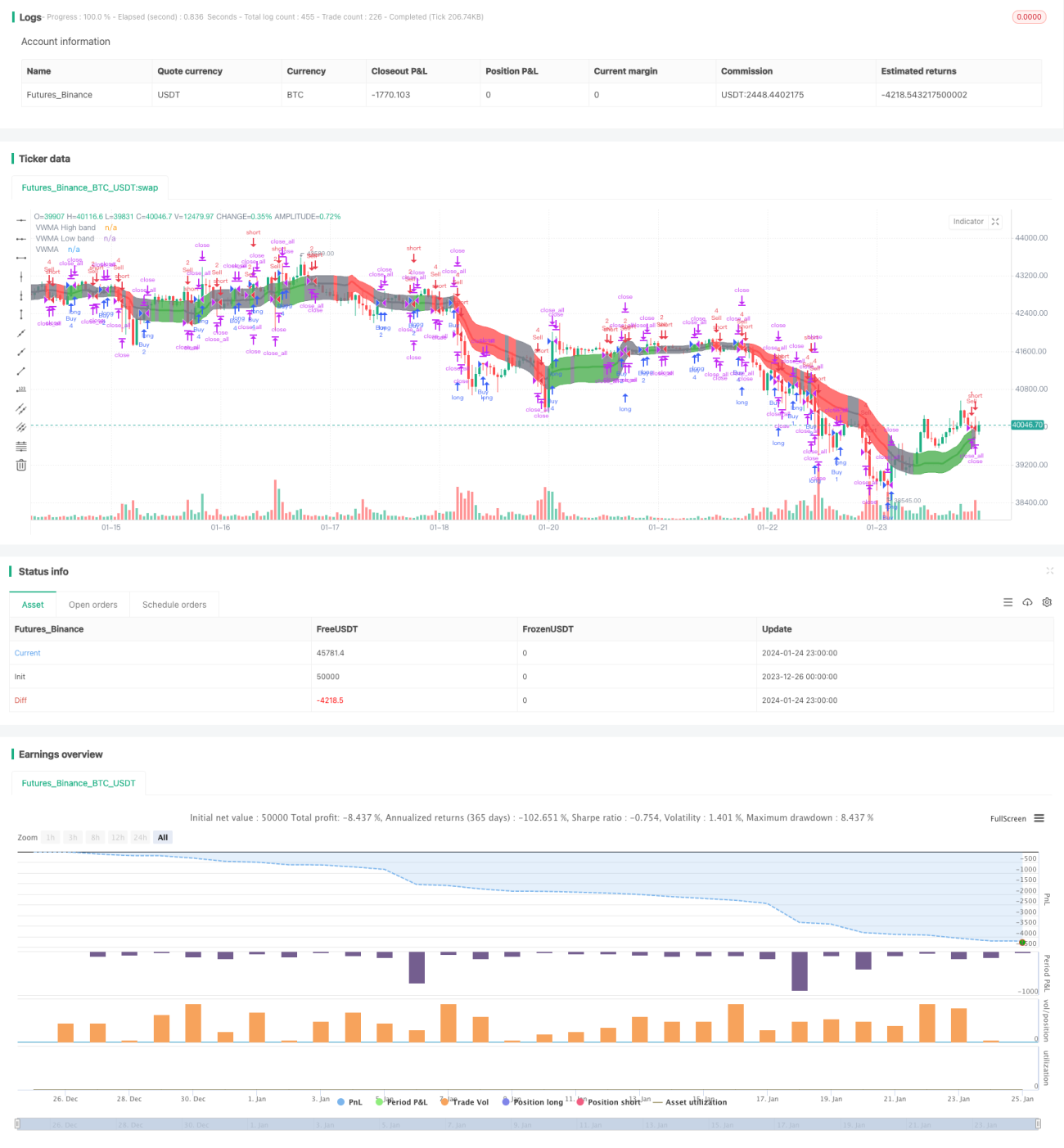

Diese Strategie kombiniert den Wave-Trend-Oszillator mit dem VWMA-Indikator und implementiert eine quantitative Trendfolgestrategie. Sie erkennt Markttrends und generiert Kauf- oder Verkaufssignale basierend auf den Signalen des Wave-Trend-Oszillators. Die Handelsgröße wird dabei anhand des VWMA-Signals bestimmt.

Strategieprinzip

Die Strategie basiert hauptsächlich auf den folgenden zwei Indikatoren:

-

Wave-Trend-Oszillator: Dieser von LazyBear auf TradingView portierte Indikator identifiziert „Wellen“ in Preisbewegungen und erzeugt Kauf-/Verkaufssignale. Die Berechnung erfolgt wie folgt: Zuerst wird der Durchschnittspreis (ap) berechnet, dann dessen EMA (esa), gefolgt vom EMA der absoluten Differenz zwischen ap und esa (d). Schließlich wird der Konkordanzindex ci = (ap - esa) / (0,015 * d) berechnet, dessen EMA den Wave-Trend (wt1) ergibt. Der 4-Perioden-SMA von wt1 ist wt2. Ein Kaufsignal entsteht, wenn wt1 wt2 von unten kreuzt, ein Verkaufssignal, wenn wt1 wt2 von oben kreuzt.

-

VWMA-Indikator: Ein volumengewichteter gleitender Mittelwert. Je nachdem, ob der Kurs innerhalb oder außerhalb der VWMA-Bänder (obere und untere Grenzen des VWMA) liegt, wird ein Signal von +1 (long), 0 (neutral) oder -1 (short) erzeugt.

Die Kauf- und Verkaufszeitpunkte werden durch die Wave-Trend-Signale bestimmt. Die genaue Handelsgröße für jede Transaktion wird anhand des Long/Short-Signals des VWMA-Indikators festgelegt.

Strategievorteile

- Die Kombination der Signale beider Indikatoren erhöht die Entscheidungsgenauigkeit.

- Der volumengewichtete VWMA-Indikator ermöglicht eine Beurteilung der Marktkräfte.

- Der Handelszeitraum kann individuell angepasst werden, um starke Schwankungen durch wichtige Nachrichtenereignisse zu vermeiden.

- Die Anpassung der Handelsgröße an das VWMA-Signal reduziert das Handelsrisiko.

Strategierisiken

- Der Wave-Trend-Indikator kann Fehlsignale erzeugen.

- Ungenaue Volumendaten können den VWMA-Indikator beeinträchtigen.

- Es wird eine längere Datenhistorie für die Indikatorberechnung benötigt.

- Es wird keine Stop-Loss-Strategie berücksichtigt.

Optimierungsmöglichkeiten

- Testen verschiedener Parameterkombinationen zur Ermittlung optimaler Parameter.

- Hinzufügen einer Stop-Loss-Strategie.

- Kombination mit anderen Indikatoren zur Signalfilterung.

- Testen unterschiedlicher Handelszeitraum-Einstellungen.

- Dynamische Anpassung der Berechnungsweise der Handelsgröße.

Zusammenfassung

Diese Strategie integriert Trendbewertung und Volumenindikatoren zu einer fortschrittlichen Trendfolgestrategie. Sie bietet gewisse Vorteile, birgt jedoch auch einige Risiken, die beachtet werden müssen. Durch Optimierung von Parametern und Regeln kann die Stabilität und Rendite der Strategie weiter verbessert werden.

- 1