Bidirektionale Gitter-Kerzen-Tracking-Handelsstrategie

Überblick

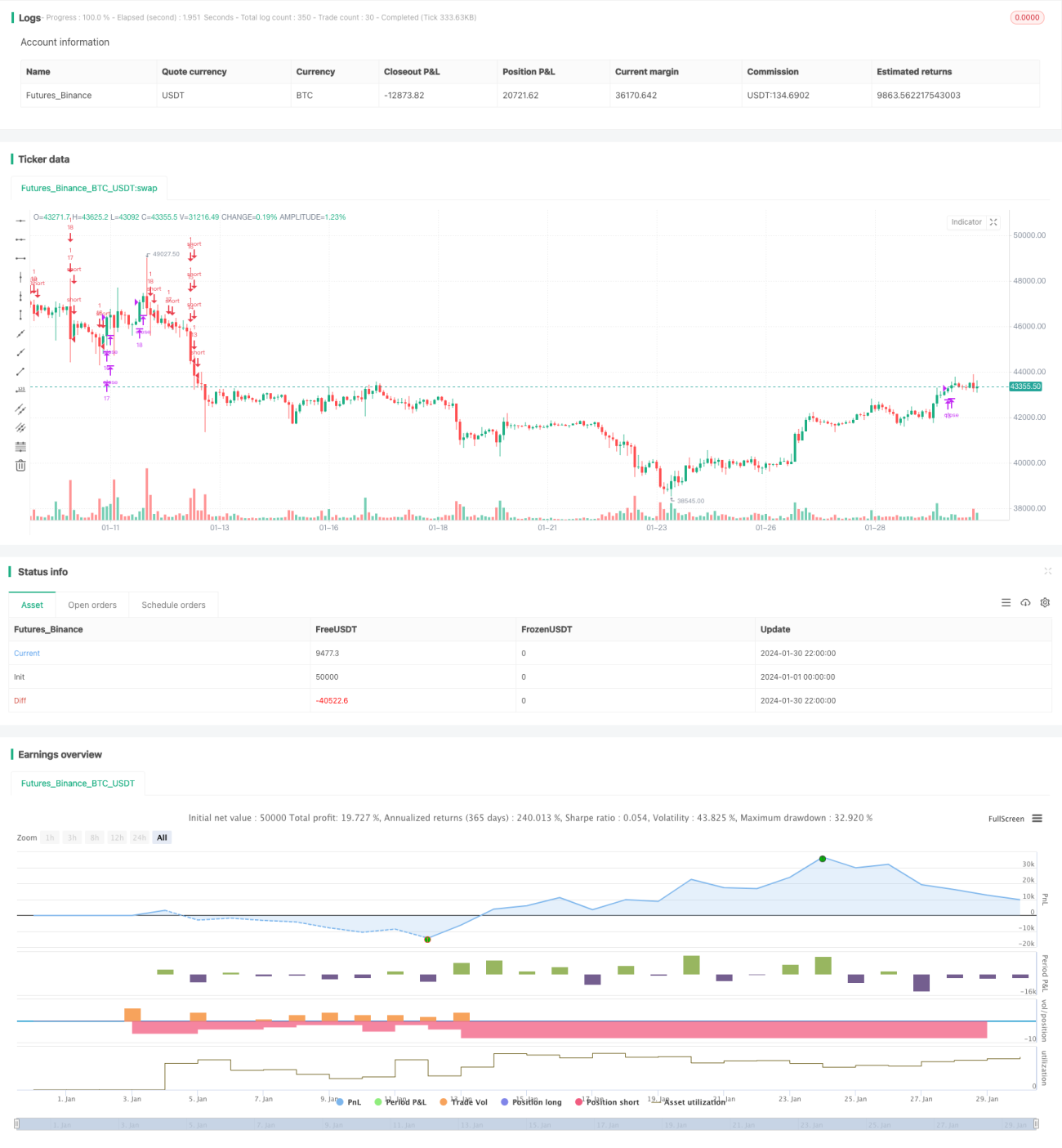

Diese Strategie ist eine bidirektionale Grid-Trading-Strategie, die auf Echtzeit-Kerzenänderungen basiert. Sie kann sowohl in Bullen- als auch in Bärenmärkten stabile Gewinne erzielen.

Strategieprinzip

-

Basierend auf der vom Benutzer festgelegten Anzahl von Gittern werden automatisch der Preisbereich des Gitters und jeder Gitterpreis berechnet.

-

Wenn der Preis einen Gitterpreis durchbricht, wird eine Long-Position mit einer festen Anzahl eröffnet; wenn der Preis unter einen Gitterpreis fällt, wird die Long-Position geschlossen und eine Short-Position eröffnet.

-

Auf diese Weise können, wenn der Preis im Gitterbereich schwankt, Gewinne durch die Verfolgung von Preisänderungen erzielt werden.

Vorteile

-

Automatische Berechnung eines sinnvollen Gitterbereichs, sodass keine manuelle Bestimmung von Support und Widerstand erforderlich ist.

-

Bidirektionaler Handel, der sich an wechselhafte Marktbedingungen anpassen kann.

-

Feste Anzahl offener Positionen fördert die Risikokontrolle.

-

Der Code ist intuitiv und klar, leicht zu verstehen und zu modifizieren.

Risikoanalyse

-

Starke Kursausschläge können zu größeren Verlusten führen.

-

Die Akkumulation von Transaktionsgebühren wirkt sich ebenfalls auf den endgültigen Gewinn aus.

-

Die Anzahl der Gitter muss angemessen bestimmt werden; zu viele Gitter erhöhen die Anzahl der Trades, aber jeder Trade bringt nur begrenzten Gewinn.

Optimierungsmöglichkeiten

-

Hinzufügen einer Stop-Loss-Strategie, um Verluste zu begrenzen.

-

Dynamische Anpassung der Gitteranzahl.

-

Einbeziehung von Hebelwirkung zur Vergrößerung des Handelsvolumens.

Zusammenfassung

Die Gesamtidee dieser Strategie ist klar und einfach. Durch bidirektionales Grid-Trading werden stabile Erträge erzielt, wobei jedoch auch gewisse Handelsrisiken bestehen. Durch kontinuierliche Optimierung können voraussichtlich bessere Ergebnisse erzielt werden.

- 1