Bidirektionale adaptive Bollinger-Bänder-Trendfolgestrategie

Übersicht

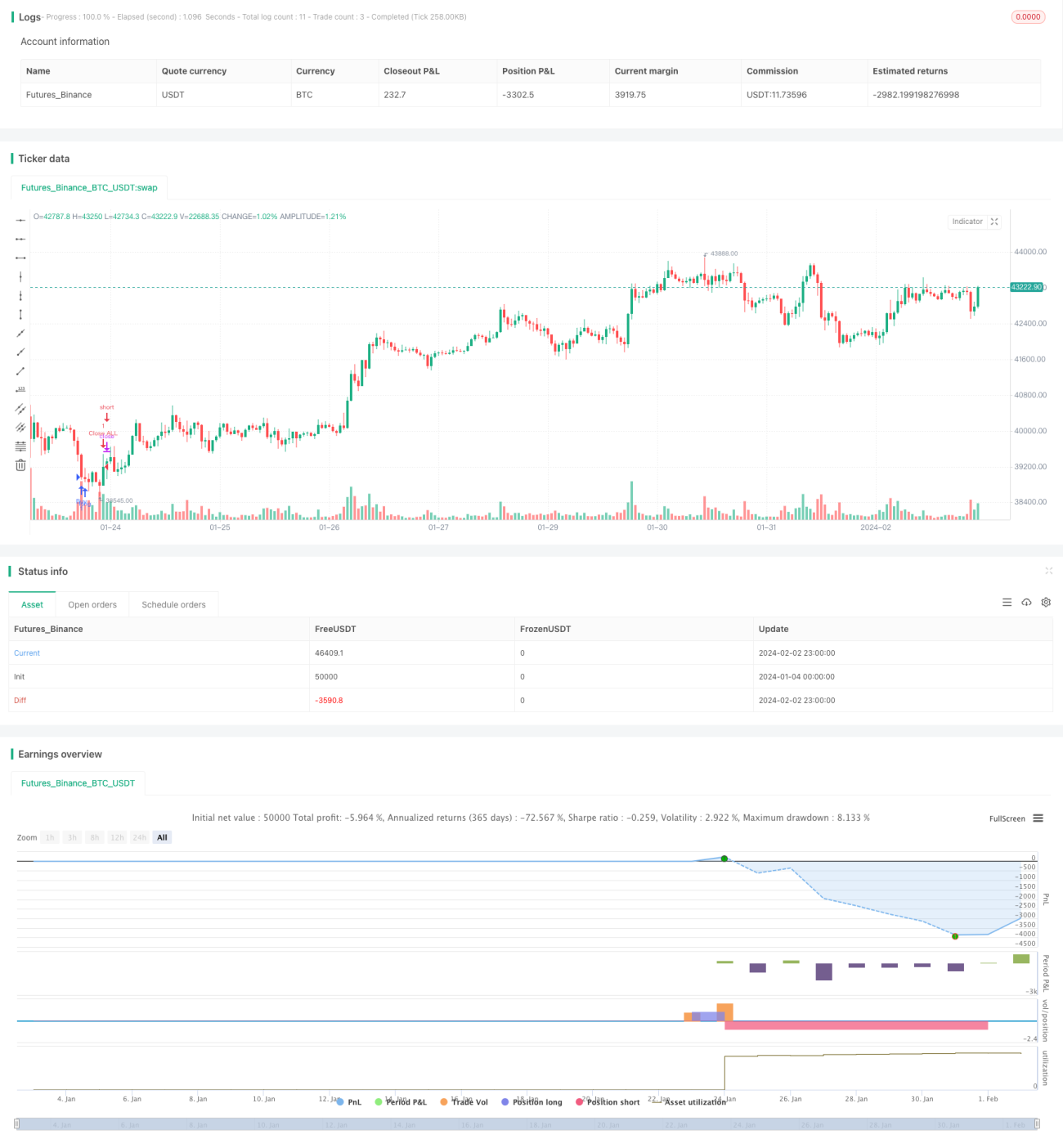

Diese Strategie verwendet den bidirektionalen adaptiven Bollinger-Band-Indikator zur Identifizierung von Trendrichtungen und kombiniert ihn mit Marktaufträgen für einen nachlaufenden Stop, um einen effizienten Trendfolgehandel zu realisieren.

Strategieprinzip

- Berechnung der mittleren, oberen und unteren Bollinger-Bänder über einen bestimmten Zeitraum.

- Wenn der Preis das obere Band durchbricht, wird eine Long-Position mit Nachlauf eröffnet; bei Durchbruch des unteren Bandes eine Short-Position.

- Schneller Einstieg mittels Marktaufträgen.

- Festlegung von Stop-Loss- und Take-Profit-Niveaus zur Positionsverwaltung.

Vorteilsanalyse

- Der adaptive Bollinger-Band-Indikator reagiert empfindlich auf Marktschwankungen und kann Trendumkehrungen schnell erkennen.

- Schneller Markteinstieg mittels Marktaufträgen reduziert das Slippage-Risiko.

- Automatischer Stop-Loss und Take-Profit zur strengen Risikokontrolle und Gewinnsicherung.

Risikoanalyse

- Bollinger-Bänder haben eine inhärente Verzögerung und können Fehlausbrüche nicht vollständig vermeiden.

- Bei Marktaufträgen kann der Ausführungspreis nicht kontrolliert werden.

- Eine angemessene Festlegung von Stop-Loss- und Take-Profit-Niveaus ist erforderlich.

Optimierungsrichtung

- Anpassung der Parameter der Bollinger-Bänder zur Optimierung der Trendempfindlichkeit.

- Einbeziehung von Indikatoren wie Volumen oder MACD zur Filterung von Fehlausbrüchen.

- Optimierung der Einstellungen für Stop-Loss und Take-Profit.

Zusammenfassung

Diese Strategie nutzt die Vorteile der Bollinger-Bänder zur Bestimmung von Trendrichtung und -änderung voll aus, kombiniert mit schnellen Marktaufträgen für einen bidirektionalen Nachlauf, um unter Risikokontrolle Überrenditen zu erzielen. Durch weitere Optimierung der Bollinger-Band-Parameter, Hinzufügen unterstützender Filterindikatoren und Anpassung der Stop-Loss-/Take-Profit-Logik kann eine bessere Strategieleistung erzielt werden. Diese Strategie ist klar konzipiert und einfach umzusetzen – eine effiziente und zuverlässige Trendfolge-Handelsstrategie.

- 1