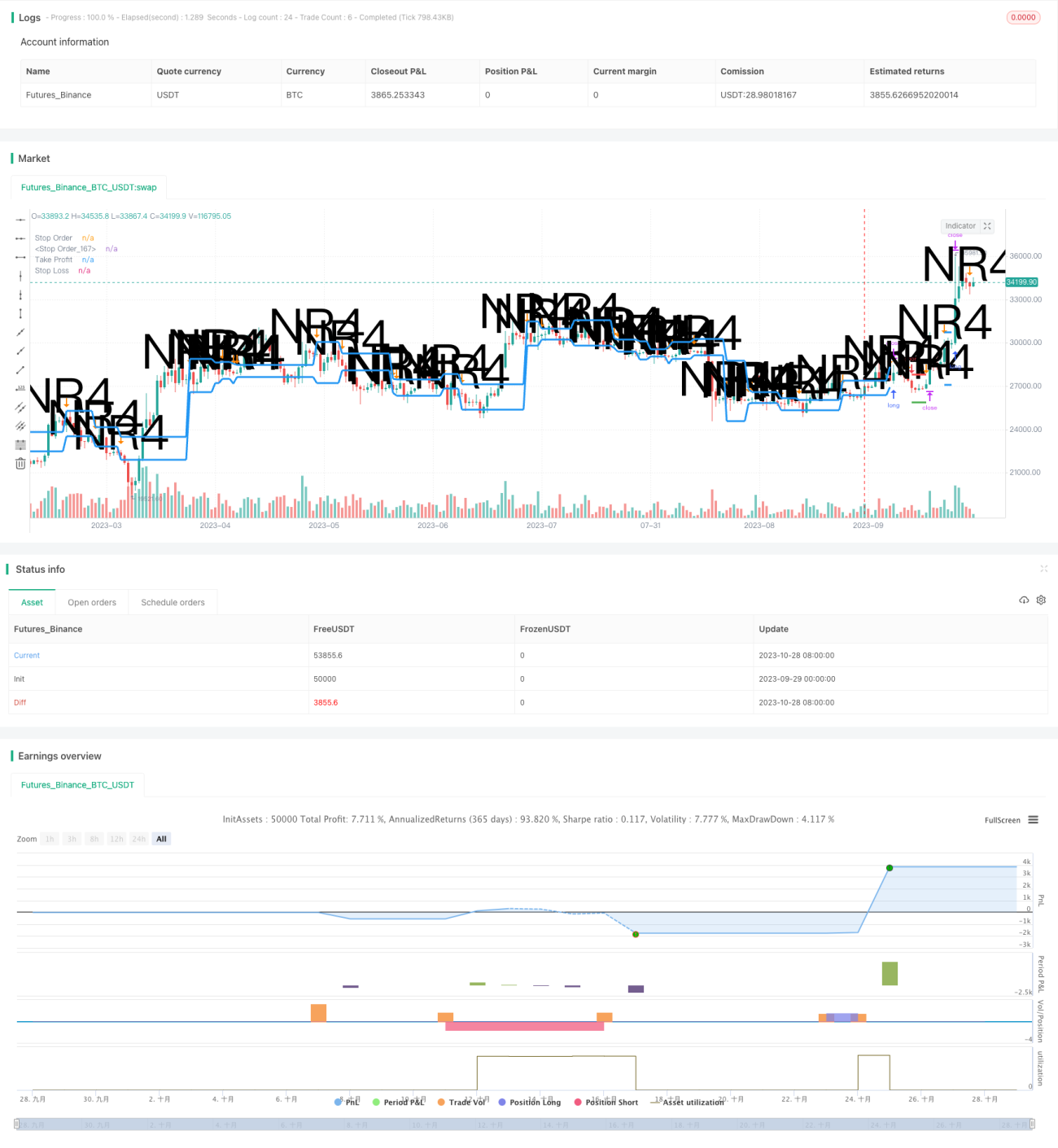

Estrategia de reversión de rango latente

Resumen

La estrategia de reversión del rango de latencia utiliza períodos de baja volatilidad del precio como señales de entrada, y cierra posiciones con ganancias cuando la volatilidad vuelve a aumentar. Identifica situaciones en las que el precio se limita a un rango estrecho y latente, para capturar tendencias de precios que están a punto de estallar. Esta estrategia suele ser aplicable cuando la volatilidad actual es baja pero existe potencial de explosión futura.

Principio de la estrategia

Primero, la estrategia identifica el rango de latencia, es decir, la situación en la que el precio se limita dentro del rango de precios del día de negociación anterior. Esto indica que la volatilidad actual ha disminuido en comparación con los días anteriores. Comparamos el precio máximo del día de negociación actual con el precio máximo de hace n días (generalmente 4 días), y el precio mínimo del día actual con el precio mínimo de hace n días para determinar si se cumple la condición del rango de latencia.

Una vez confirmado el rango de latencia, la estrategia coloca dos órdenes pendientes simultáneamente: una orden de compra cerca del máximo del rango y una orden de venta cerca del mínimo del rango. Luego espera a que el precio rompa el rango de latencia para continuar al alza o a la baja. Si el precio rompe al alza, se activa la orden de compra y se abre una posición larga; si rompe a la baja, se activa la orden de venta y se abre una posición corta.

Una vez abierta la posición, la estrategia establece órdenes de stop loss y take profit. La orden de stop loss limita el riesgo a la baja, mientras que la orden de take profit cierra la posición con ganancias. La distancia de la orden de stop loss desde el precio de entrada es un porcentaje determinado por el parámetro de gestión de riesgos; la distancia de la orden de take profit desde el precio de entrada es el tamaño del rango de latencia, ya que se espera que el movimiento del precio tenga una magnitud similar a la volatilidad anterior.

Finalmente, la estrategia incluye un módulo de gestión de capital. Utiliza el método de multiplicador fijo para ajustar el volumen de las órdenes, aumentando la utilización del capital en operaciones rentables y reduciendo el riesgo en operaciones perdedoras.

Análisis de ventajas

Esta estrategia presenta las siguientes ventajas:

- Utiliza momentos de baja volatilidad como señales de entrada, lo que permite capturar oportunidades antes de que ocurra una tendencia de precios.

- Establece órdenes de trading tanto largas como cortas, pudiendo capturar tendencias alcistas o bajistas.

- Emplea estrategias de stop loss y take profit, controlando eficazmente el riesgo de cada operación.

- Aplica el método de multiplicador fijo para la gestión de capital, mejorando la eficiencia del uso del capital.

- La lógica de la estrategia es clara y sencilla de implementar.

Análisis de riesgos

Esta estrategia también presenta algunos riesgos a considerar:

- Riesgo de error en la dirección de la ruptura del rango de latencia. El precio podría no romper claramente ni al alza ni a la baja, lo que llevaría a una dirección de entrada incorrecta.

- Riesgo de que la ruptura no continúe en la dirección esperada. La ruptura podría ser solo un fenómeno de reversión a corto plazo.

- Riesgo de que se active el stop loss. Movimientos extremadamente grandes del precio podrían superar directamente el nivel de stop loss.

- Riesgo de ampliación de pérdidas por el método de multiplicador fijo al añadir posiciones. Se puede reducir el valor del multiplicador fijo para disminuir el riesgo.

- Una parametrización inadecuada podría resultar en un rendimiento deficiente de la estrategia.

Direcciones de optimización

La estrategia se puede optimizar en los siguientes aspectos:

- Agregar filtros de señal, como divergencias en la ruptura, para evitar rupturas falsas.

- Mejorar la estrategia de stop loss, por ejemplo, usando stop loss móvil o stop loss con órdenes pendientes.

- Incorporar indicadores de tendencia para evitar entrar en reversiones.

- Optimizar el valor del multiplicador fijo para equilibrar la relación ganancias/pérdidas.

- Combinar el análisis de múltiples marcos temporales para aumentar la probabilidad de ganancias.

- Utilizar métodos de aprendizaje automático para optimizar parámetros automáticamente.

Resumen

La estrategia de reversión del rango de latencia tiene una idea general clara y un cierto potencial de ganancias. Mediante la optimización de parámetros, la gestión de riesgos y el filtrado de señales, se puede mejorar aún más la estabilidad de la estrategia. Sin embargo, cualquier estrategia de reversión de tendencia conlleva cierto riesgo, por lo que debe utilizarse con precaución y ajustar adecuadamente el tamaño de las posiciones. Esta estrategia es adecuada para traders familiarizados con operaciones de reversión y con conciencia de riesgo.

- 1