Rastreador de Tendencia de Ruptura V2

Resumen

Esta estrategia es una variante de otra estrategia de seguimiento de ruptura de tendencia que desarrollé anteriormente. En la otra estrategia, se puede utilizar una media móvil como filtro para las operaciones (es decir, si el precio está por debajo de la media móvil, no se toma una posición larga). Después de crear una herramienta para detectar la tendencia en marcos temporales superiores, quise ver si podría ser un filtro mejor que la media móvil.

Por lo tanto, esta estrategia permite observar la tendencia en marcos temporales superiores (es decir, ¿hay máximos más altos y mínimos más bajos? Si es así, es una tendencia alcista). Solo se opera en la dirección de la tendencia. Se pueden seleccionar hasta dos tendencias como filtro. Cada dirección de tendencia se muestra en una tabla en el gráfico para facilitar la referencia. Los niveles actuales de soporte y resistencia se dibujan en el gráfico, de modo que se pueda ver cuándo podría producirse una ruptura de la tendencia del marco temporal actual y de la tendencia de nivel superior.

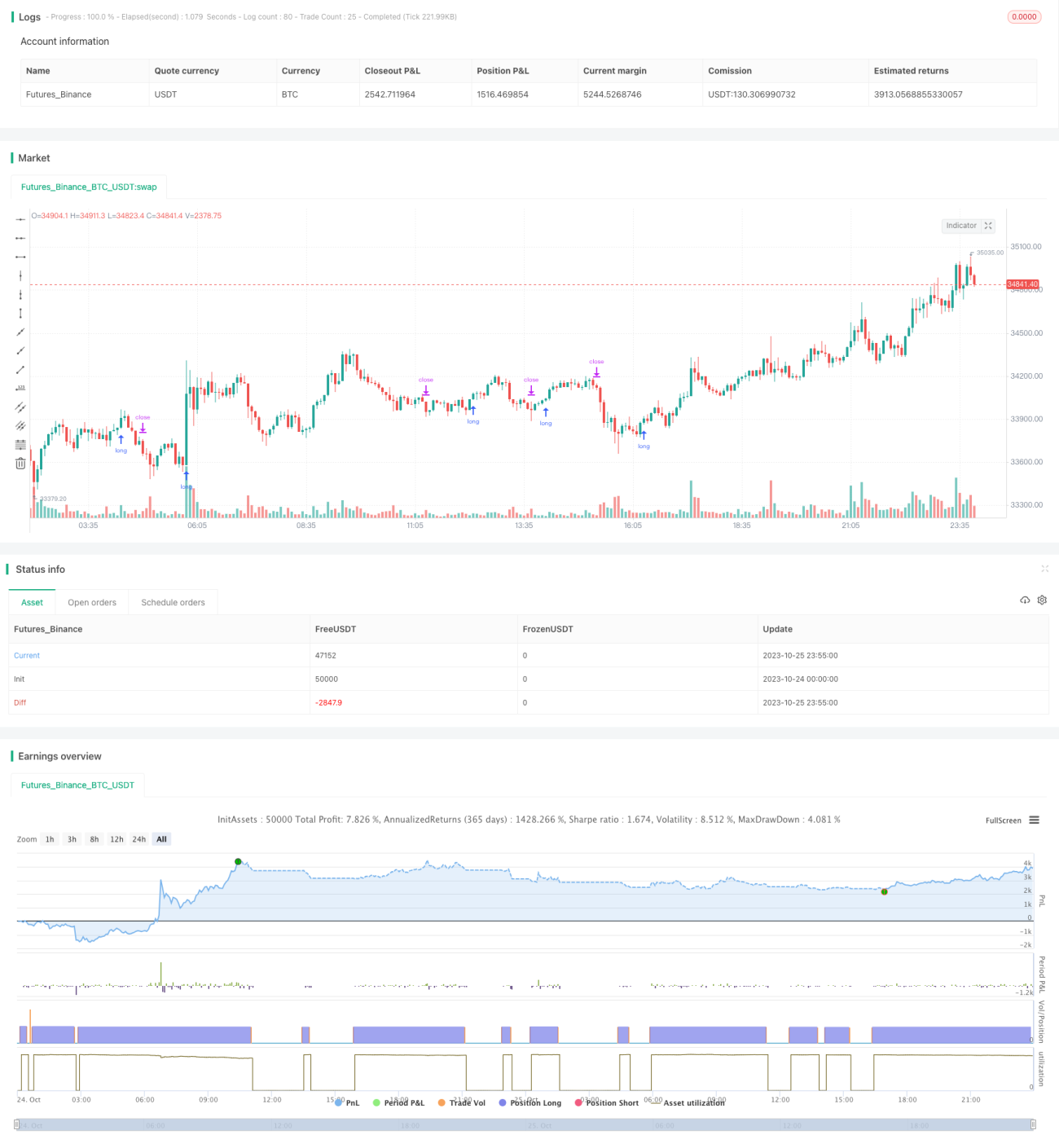

He observado que, en comparación con otras estrategias, el rendimiento de esta generalmente no es muy bueno, pero parece ser más selectiva con las operaciones. Muestra una tasa de aciertos más alta y un mejor factor de beneficio. Solo realiza unas pocas operaciones, y el beneficio neto tampoco es muy bueno.

Principio de la Estrategia

La lógica central de la estrategia es utilizar la ruptura de los niveles de soporte y resistencia en marcos temporales superiores para identificar la tendencia y operar según su dirección.

Específicamente, se implementa mediante los siguientes pasos:

-

Calcular los niveles de soporte y resistencia del marco temporal actual (por ejemplo, gráfico de 1 hora). Esto se logra encontrando los precios máximos y mínimos dentro de un período determinado.

-

Calcular los niveles de soporte y resistencia de uno o más marcos temporales superiores (por ejemplo, gráfico de 4 horas y diario). Esto utiliza la misma lógica que para el marco temporal actual.

-

Dibujar líneas horizontales de estos niveles de soporte y resistencia en el gráfico. Cuando el precio rompe estos niveles, la tendencia del marco temporal superior cambia.

-

Determinar la dirección de la tendencia según si el precio ha roto estos niveles clave. Si el precio supera el máximo anterior, se considera una tendencia alcista. Si rompe por debajo del mínimo anterior, se considera una tendencia bajista.

-

Permitir al usuario seleccionar una o más tendencias de marcos temporales superiores como condición de filtro. Es decir, solo se considerará realizar una operación cuando la dirección de la tendencia del marco temporal actual coincida con la de los marcos temporales superiores.

-

Cuando se cumplan las condiciones del filtro de tendencia y el precio actual rompa un nivel clave, se realiza una compra o venta. El nivel de stop loss se establece en el nivel de soporte o resistencia clave anterior.

-

A medida que el precio se mueve, cuando se forman nuevos máximos o mínimos, se desplaza el stop loss al nuevo mínimo para asegurar ganancias y seguir la tendencia.

-

Cuando se activa el stop loss o se rompe un nivel clave de soporte/resistencia, se cierra la posición.

A través de este análisis de tendencia en múltiples marcos temporales, la estrategia intenta operar solo en la dirección de la tendencia más fuerte para aumentar la probabilidad de éxito. Al mismo tiempo, los niveles clave proporcionan señales claras de entrada y stop loss.

Ventajas de la Estrategia

-

Utiliza múltiples marcos temporales para juzgar la tendencia, lo que permite identificar con mayor precisión las direcciones de tendencia más fuertes y evitar ser engañado por el ruido del mercado.

-

Operar solo en la dirección de la tendencia principal puede aumentar significativamente la tasa de aciertos. Según los resultados de las pruebas, en comparación con el filtro simple de media móvil, esta estrategia muestra una mayor tasa de aciertos y una mejor relación riesgo-beneficio.

-

Los niveles de soporte y resistencia proporcionan puntos de entrada y stop loss claros. No es necesario debatir sobre la selección del punto de entrada exacto.

-

Ajustar la posición del stop loss a medida que avanza la tendencia permite maximizar la retención de ganancias.

-

La lógica de la estrategia es simple y clara, fácil de entender y optimizar.

Riesgos de la Estrategia

-

Depende del juicio de la tendencia en marcos temporales largos, por lo que en caso de reversión de la tendencia, es fácil quedar atrapado. Se debe acortar adecuadamente el período de juicio de la tendencia o utilizar otros indicadores como ayuda.

-

No tiene en cuenta el impacto de los fundamentos, lo que puede generar divergencias con el precio de las acciones cuando ocurren eventos importantes. Se pueden agregar filtros como eventos importantes o fechas de informes de resultados.

-

No se ha establecido un control del tamaño de la posición. Se puede ajustar el tamaño de la posición según el tamaño del capital de la cuenta, la volatilidad y otros factores.

-

El período de backtesting es limitado. Se debe ampliar el período de backtesting para probar la solidez en diferentes condiciones de mercado.

-

No se considera el impacto de los costos de transacción. En el trading en vivo, se deben ajustar los parámetros de la estrategia según los costos de transacción específicos.

-

Solo considera operaciones a largo plazo. Se puede combinar con otras estrategias para desarrollar señales de trading a corto plazo y lograr arbitraje en múltiples plazos.

Direcciones de Optimización de la Estrategia

-

Aumentar condiciones de filtro:

-

Datos fundamentales, como informes de resultados, eventos noticiosos, etc.

-

Indicadores, como volumen, stop loss basado en ATR, etc.

-

-

Optimizar parámetros:

-

Ajustar el período de cálculo de los niveles de soporte/resistencia

-

Ajustar los marcos temporales para el juicio de tendencia

-

-

Ampliar el alcance de la estrategia:

-

Desarrollar estrategias de trading a corto plazo

-

Considerar oportunidades de venta en corto

-

Arbitraje entre múltiples instrumentos

-

-

Mejorar la gestión de riesgos:

-

Optimizar el tamaño de la posición según la volatilidad y el tamaño del capital

-

Optimizar la estrategia de stop loss, como stop loss móvil, stop loss con órdenes pendientes, etc.

-

Introducir un mecanismo de recompensa y penalización por riesgo

-

-

Optimizar la lógica de ejecución:

-

Mejorar la selección del momento de entrada

-

Considerar la entrada parcial de posiciones

-

Optimizar la estrategia de desplazamiento del stop loss

-

Resumen

Esta estrategia, mediante el análisis de la tendencia en múltiples marcos temporales, diseña un sistema de ruptura relativamente robusto. En comparación con filtros como la media móvil simple, muestra una mayor tasa de aciertos y una mejor relación riesgo-beneficio. Sin embargo, también tiene aspectos que se pueden optimizar, como un mecanismo de gestión de riesgos incompleto y la falta de consideración de factores fundamentales. Si se optimiza aún más, puede convertirse en una estrategia de seguimiento de tendencia muy práctica. En general, la estrategia está bien diseñada y mejora la precisión del juicio mediante el análisis de múltiples marcos temporales, por lo que merece una mayor investigación y aplicación.

- 1