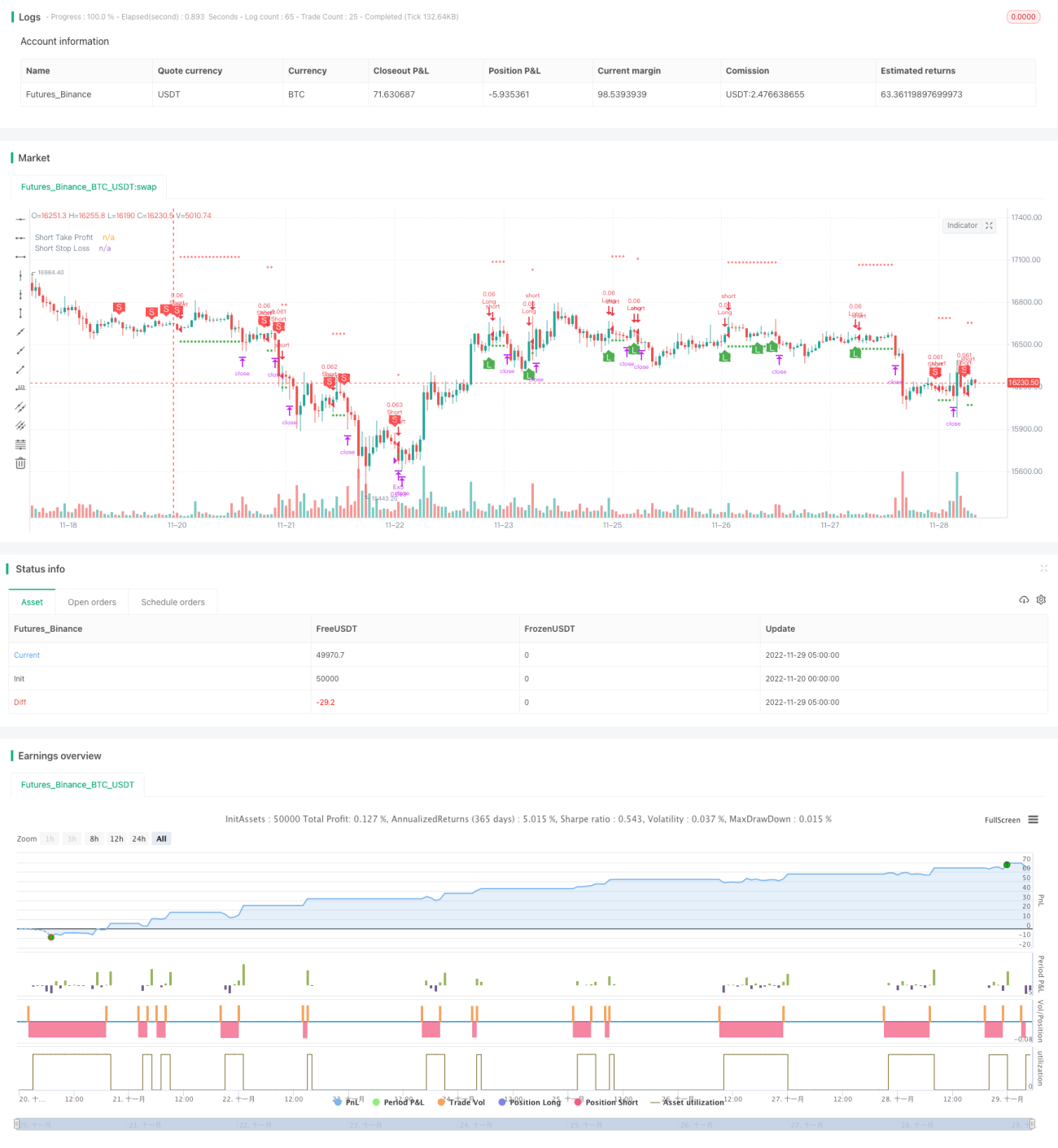

Estrategia de seguimiento de tendencia con doble EMA e indicador Williams

Resumen

Esta estrategia combina dos indicadores EMA (medias móviles exponenciales) y el indicador Williams para identificar la dirección de la tendencia y realizar seguimiento cuando la tendencia es fuerte. Su idea básica es:

- Utilizar un par de EMA para filtrar únicamente las tendencias más fuertes.

- El indicador Williams confirma si el mercado se encuentra en zona de sobrecompra o sobreventa.

- Combinar con el indicador RSI para evitar comprar en máximos o vender en mínimos.

Principio

La estrategia emplea dos EMA: una de corto plazo y otra de largo plazo. Cuando la EMA de corto plazo cruza al alza la EMA de largo plazo, se genera una señal de compra; cuando la cruza a la baja, se genera una señal de venta. De esta forma se capturan tendencias de mediano y largo plazo.

Además, se incorpora el indicador Williams para identificar situaciones de reversión. Este indicador determina si el precio está en sobrecompra o sobreventa al evaluar los máximos y mínimos del período. Cuando el Williams muestra sobrecompra, se genera señal de venta; cuando muestra sobreventa, señal de compra.

La lógica específica en el código es:

Entrada larga: la EMA corta cruza al alza la EMA media y la EMA larga, el Williams muestra zona de sobreventa y forma un mínimo en dicha zona, lo que indica una oportunidad de reversión. Entonces se genera una señal de compra.

Entrada corta: la EMA corta cruza a la baja la EMA media y la EMA larga, el Williams muestra zona de sobrecompra y forma un máximo en dicha zona, lo que indica una oportunidad de reversión. Entonces se genera una señal de venta.

Además, se introduce el indicador RSI para confirmar las señales y evitar perseguir precios.

Ventajas

La mayor ventaja de esta estrategia es que utiliza el doble EMA para filtrar gran cantidad de tendencias no válidas, seleccionando solo las tendencias de mediano y largo plazo más fuertes, reduciendo así el ruido y las operaciones ineficientes.

Además, la inclusión del indicador Williams es muy efectiva: por un lado, permite identificar oportunidades de reversión para cerrar posiciones a tiempo; por otro, confirma la validez de las señales de tendencia.

La combinación de doble EMA y Williams permite que la estrategia obtenga buenos beneficios de seguimiento en instrumentos de mediano y largo plazo, al tiempo que puede identificar reversiones y limitar pérdidas.

Riesgos

El principal riesgo de esta estrategia es la dificultad para identificar puntos de reversión de la tendencia. Aunque se incorporan el Williams y el RSI para asegurar la efectividad de las operaciones de reversión, estas siguen siendo complejas y no se puede evitar por completo el riesgo de comprar en máximos o vender en mínimos.

Además, el par de EMA en sí mismo tiene cierto retraso. Cuando la tendencia de corto plazo se desvincula de la de mediano y largo plazo, la estrategia puede tener dificultades para identificar la situación.

Optimización

La estrategia puede mejorarse en los siguientes aspectos:

-

Probar más combinaciones de períodos de EMA para encontrar parámetros óptimos.

-

Agregar mecanismos de salida adaptativos, utilizando indicadores como ATR o índice de volatilidad para detectar reversiones de tendencia.

-

Incorporar elementos de aprendizaje automático, como LSTM, para predecir tendencias y reversiones.

-

Utilizar teoría de ondas (Elliott Wave) u otros métodos para perfeccionar las reglas de operaciones de reversión.

-

Introducir gestión de posición adaptativa, ajustando el tamaño de la posición según las condiciones del mercado.

Conclusión

Esta estrategia combina con éxito el doble EMA y el indicador Williams para capturar tendencias de mediano y largo plazo, obteniendo mayores rendimientos en movimientos fuertes. Al mismo tiempo, la inclusión del Williams permite identificar reversiones y detener pérdidas a tiempo. Como próximo paso, se pueden incorporar más indicadores y modelos para optimizarla y fortalecer su estabilidad.

/*backtest

start: 2022-11-20 00:00:00

end: 2022-11-29 05:20:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1