Estrategia de seguimiento de tendencia con canales envolventes de media móvil

Resumen

La estrategia de seguimiento de tendencia con canales envolventes de media móvil es una estrategia basada en medias móviles e indicadores de canal para el seguimiento de tendencias. Establece canales de media móvil multinivel para identificar y seguir la tendencia del precio. Además, combina cálculos de medias móviles de diferentes marcos temporales para lograr una fusión multi-tiempo, lo que ayuda a capturar tendencias de mayor magnitud.

Principio de la estrategia

El principio central de la estrategia se basa en la función de seguimiento de tendencia de las medias móviles y el juicio de canal del indicador Envelop. La estrategia utiliza parámetros configurables como el período de la media móvil, el tipo de suavizado, la fuente de precio, etc., para construir una media móvil base. Luego, según el porcentaje de desplazamiento establecido en los parámetros, se crean canales superior e inferior. Cuando el precio rompe el canal inferior, se abre una posición larga; cuando rompe el canal superior, se abre una posición corta. Al mismo tiempo, la estrategia introduce una media móvil independiente como línea de stop loss.

En concreto, la estrategia tiene las siguientes características:

- Admite operaciones tanto largas como cortas, determinando la dirección de la tendencia a través de los canales superior e inferior.

- Permite abrir hasta 4 posiciones, utilizando una pirámide escalonada para aumentar posiciones y buscar mayores ganancias.

- Puede configurar medias móviles independientes para apertura y cierre de posiciones, logrando un stop loss preciso.

- Soporta cálculos de medias móviles en diferentes marcos temporales (desde 1 minuto hasta 1 día), logrando una fusión multi-tiempo.

- Ofrece 6 modos de suavizado diferentes para las medias móviles de apertura y cierre, optimizables según el activo y el período.

- Permite ingresar desplazamientos positivos o negativos para ajustar los canales, buscando rupturas más precisas.

La lógica de trading específica es la siguiente:

- Se calcula la media móvil base de apertura y, según el porcentaje de parámetro, se obtienen 4 líneas de ruptura.

- Cuando el precio rompe el canal inferior, se abren posiciones largas en orden; cuando rompe el canal superior, se abren posiciones cortas en orden.

- Se calcula una media móvil independiente para el cierre, que actúa como línea de stop loss. Cuando el precio vuelve a caer por debajo de ella, se cierran las posiciones largas gradualmente; cuando el precio vuelve a subir por encima, se cierran las posiciones cortas gradualmente.

- Se pueden abrir hasta 4 posiciones, utilizando una pirámide escalonada para aumentar posiciones y buscar mayores ganancias.

Según el principio de la estrategia, esta combina el seguimiento de tendencia de las medias móviles, las señales de ruptura de canales y la configuración de una línea de stop loss independiente, formando un sistema de tendencia riguroso y completo.

Análisis de ventajas

Basado en el código y la lógica de la estrategia, esta estrategia de seguimiento de tendencia con canales envolventes de media móvil tiene las siguientes ventajas:

-

Fusión multi-tiempo, mayor probabilidad de capturar tendencias de gran escala. La estrategia admite cálculos de medias móviles en marcos temporales desde 1 minuto hasta 1 día, permitiendo configurar diferentes períodos para las medias móviles de apertura y stop loss, fusionando la capacidad de juicio de tendencia de múltiples marcos temporales, lo que favorece la captura de tendencias de gran escala.

-

Pirámide de aumento de posiciones, buscando mayores ganancias. La estrategia permite abrir hasta 4 posiciones, equilibrando la relación riesgo-beneficio mediante el aumento escalonado, buscando mayores ganancias bajo control de riesgo.

-

6 modos de media móvil seleccionables, alta adaptabilidad. Las medias móviles de apertura y stop loss admiten 6 modos como SMA/EMA/MMA, optimizables según el activo y el período, mejorando la adaptabilidad.

-

Canales ajustables, rupturas precisas. La estrategia permite ingresar un parámetro de porcentaje de desplazamiento del canal para ajustar su anchura, optimizándolo según el activo o el entorno de mercado, mejorando la precisión de las rupturas.

-

Línea de stop loss independiente, ayuda al control de riesgo. La estrategia calcula una media móvil independiente como línea de cierre para detener pérdidas en posiciones largas o cortas, reduciendo significativamente el riesgo de trading y evitando pérdidas excesivas.

-

Código estructurado, fácil de modificar. La estrategia está escrita en Pine Script, con una estructura clara y fácil de entender y modificar. Los usuarios pueden seguir optimizando parámetros o agregando otra lógica basada en el marco existente.

Análisis de riesgos

Aunque la estrategia es rigurosa en lógica y control de riesgos, existen ciertos riesgos de trading que deben tenerse en cuenta:

-

Riesgo de reversión de tendencia de gran escala. La hipótesis central de la estrategia es que el precio continuará avanzando, con cierta tendencia. Sin embargo, una reversión de tendencia de gran escala puede causar un impacto significativo en las ganancias. En ese caso, es necesario aplicar stop loss a tiempo para controlar pérdidas.

-

Riesgo de ruptura fallida. En mercados laterales o de consolidación, el precio puede romper el canal y luego volver a caer. Esto puede provocar pérdidas, y es necesario optimizar parámetros para reducir esta ocurrencia.

-

Riesgo de gestión de expectativas. La estrategia busca mayores ganancias con 4 capas de aumento de posiciones, lo que mejora significativamente las ganancias en tendencias favorables, pero reduce las expectativas en pérdidas. Esto requiere una gestión profesional de la psicología del inversor.

-

Riesgo de optimización de señales. La estrategia implica el ajuste de varios parámetros como la anchura del canal, el período de las medias móviles, etc., lo que requiere experiencia en optimización por parte de analistas cuantitativos para evitar el sobreajuste.

-

Riesgo de condiciones extremas de mercado. Eventos como gaps rápidos o días límite de corto plazo pueden alterar gravemente la lógica de la estrategia. En tales casos, es necesario monitorear los indicadores de riesgo del sistema y aplicar stop loss oportunamente.

En resumen, la estrategia depende principalmente de tendencias de gran escala para obtener ganancias, y solo es adecuada para activos y entornos de mercado con características de continuación a largo plazo. Además, la optimización de múltiples parámetros y el control de la psicología son clave para asegurar ganancias estables.

Direcciones de optimización

Para esta estrategia de seguimiento de tendencia con canales envolventes de media móvil, las principales direcciones de optimización futuras incluyen:

-

Optimización adaptativa del canal y la línea de stop loss basada en algoritmos de aprendizaje automático. Se pueden utilizar modelos como LSTM o predicción de trayectorias para entrenar modelos de canal y stop loss, logrando una predicción de precios y evasión de riesgos más inteligente.

-

Incorporación de indicadores de sentimiento, ratios de tenencia de cartera, etc., para optimizar la lógica de aumento de posiciones. Se pueden agregar indicadores como la volatilidad absoluta o el sentimiento del mercado para controlar el riesgo de la cartera y optimizar la pirámide de aumento de posiciones.

-

Inclusión de modelos de costos de transacción y deslizamiento para mejorar la realismo del backtest. Actualmente, el backtest no considera los costos de transacción, que son un factor importante en el trading real; se necesita un modelo matemático para incorporarlos.

-

Ampliación del análisis de correlación entre activos similares para construir un sistema unificado de control de riesgos. Extender la estrategia a múltiples mercados similares como materias primas o criptomonedas, unificando el control de riesgos a través del análisis de correlación para mejorar la estabilidad.

-

Aumento de la explicabilidad de la estrategia para mejorar la usabilidad para los usuarios. Utilizar métodos como SHAP para analizar el impacto de cada variable de entrada en los resultados, mostrando rankings de importancia, haciendo que la lógica de la estrategia sea más transparente y comprensible para los usuarios.

Mediante la introducción de aprendizaje automático, modelos multifactoriales y otros algoritmos, continuar optimizando la estabilidad, realismo y facilidad de uso de la estrategia son las principales direcciones de mejora futuras.

Conclusión

En resumen, esta estrategia de seguimiento de tendencia con canales envolventes de media móvil combina tres elementos centrales: el seguimiento de tendencia de las medias móviles, el juicio de tendencia mediante canales envolventes y el control de riesgo con una línea de stop loss independiente. En mercados con tendencia definida, la estrategia puede proporcionar rendimientos estables con cierto beneficio por rupturas. Sin embargo, los usuarios deben prestar atención al control del entorno de mercado de gran escala, realizar una buena optimización de parámetros y gestión de riesgos, para que la estrategia pueda adaptarse a mercados complejos y cambiantes. En general, la estrategia ofrece una solución de seguimiento de tendencia relativamente completa y rigurosa, siendo un marco cuantitativo muy adecuado para la autoconstrucción y el desarrollo secundario.

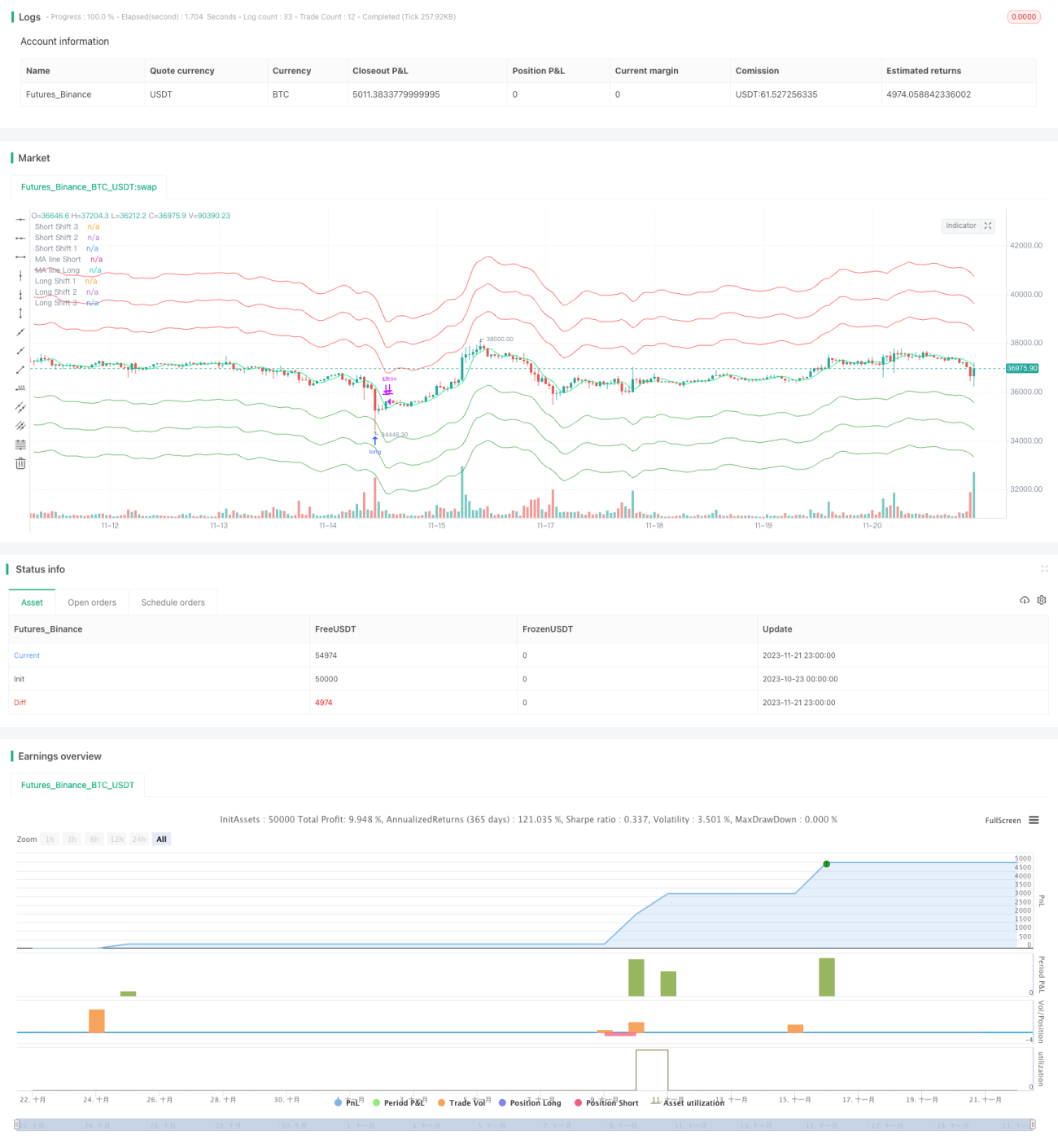

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the GNU Affero General Public License v3.0 at https://www.gnu.org/licenses/agpl-3.0.html

//@version=4

strategy(title = "HatiKO Envelopes", shorttitle = "HatiKO Envelopes", overlay = true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, pyramiding = 4, initial_capital=10, calc_on_order_fills=false)

- 1