Estrategia de ruptura de supertendencia en marcos temporales cruzados

Resumen

Esta estrategia combina el indicador Super Trend de múltiples marcos temporales con las Bandas de Bollinger para identificar la dirección de la tendencia y los niveles clave de soporte y resistencia, realizando entradas en rupturas de volatilidad y saliendo de las posiciones basándose en cruces. La estrategia es adecuada principalmente para futuros de materias primas de alta volatilidad, como oro, plata, petróleo crudo, etc.

Principio de la Estrategia

Se basa en la función personalizada de Super Trend de múltiples marcos temporales pine_supertrend() escrita en Pine Script, combinando Super Trend de diferentes períodos (por ejemplo, 1 minuto y 5 minutos) para juzgar la dirección de la tendencia en marcos temporales mayores.

Al mismo tiempo, se calculan las bandas superior e inferior de Bollinger para determinar rupturas de canales. Cuando el precio supera la banda superior de Bollinger, se considera una ruptura alcista; cuando el precio cae por debajo de la banda inferior, se considera una ruptura bajista.

Señales de la estrategia:

- Señal larga: Precio de cierre > banda superior de Bollinger y precio de cierre > indicador Super Trend de múltiples marcos temporales.

- Señal corta: Precio de cierre < banda inferior de Bollinger y precio de cierre < indicador Super Trend de múltiples marcos temporales.

Stop loss:

- Stop loss largo: Precio de cierre < indicador Super Trend de 5 minutos.

- Stop loss corto: Precio de cierre > indicador Super Trend de 5 minutos.

Por lo tanto, la estrategia captura las rupturas de confluencia entre el indicador Super Trend y las Bandas de Bollinger, realizando operaciones en mercados de alta volatilidad.

Ventajas

- Utiliza el indicador Super Trend de múltiples marcos temporales para determinar la dirección de la tendencia en marcos mayores, mejorando la calidad de las señales.

- Las bandas superior e inferior de Bollinger actúan como niveles clave de soporte y resistencia, reduciendo falsas rupturas.

- El indicador Super Trend se utiliza como nivel de stop loss, reduciendo pérdidas y controlando el riesgo.

Análisis de Riesgos

- El indicador Super Trend tiene rezago, lo que podría hacer que se pierdan puntos de reversión de tendencia.

- Una configuración inadecuada de los parámetros de las Bandas de Bollinger podría generar señales demasiado frecuentes o muy pocas operaciones.

- En sesiones nocturnas de futuros de materias primas o durante eventos importantes, las fluctuaciones bruscas de precios pueden activar fácilmente el stop loss.

Soluciones a los riesgos:

- Combinar con múltiples indicadores auxiliares para confirmar señales y evitar falsas rupturas.

- Optimizar los parámetros de las Bandas de Bollinger para encontrar el punto de equilibrio óptimo.

- Ajustar la ubicación del stop loss, ampliando la distancia del mismo.

Direcciones de Optimización

- Probar otros indicadores de tendencia, como KDJ, MACD, etc., como juicio auxiliar.

- Incorporar la probabilidad de juicio de modelos de aprendizaje automático como apoyo.

- Realizar optimización de parámetros para encontrar la mejor combinación de hiperparámetros.

Conclusión

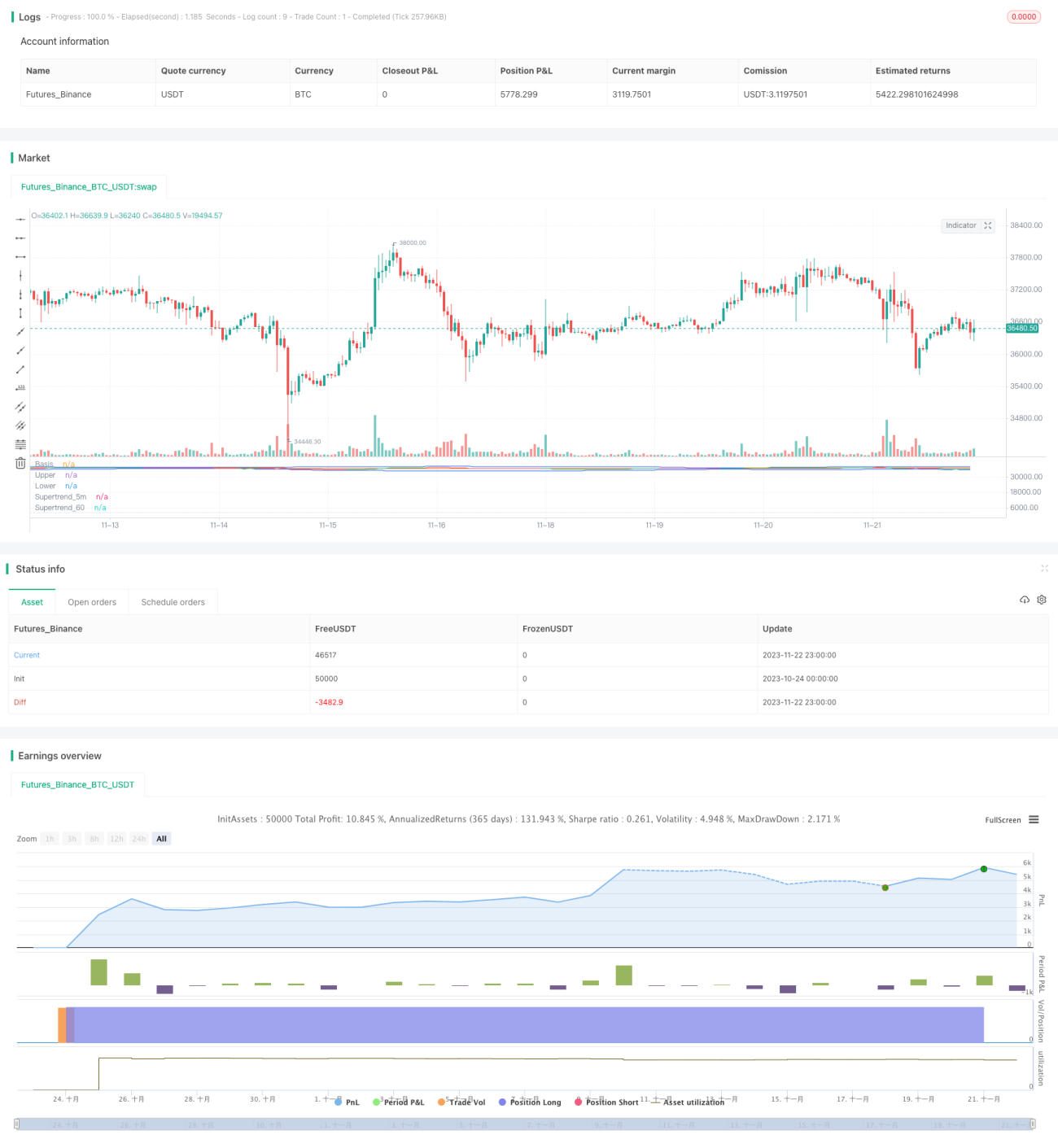

Esta estrategia integra dos indicadores eficientes, Super Trend y Bandas de Bollinger, logrando operaciones de alta probabilidad mediante el análisis entre marcos temporales y la detección de rupturas de canales. La estrategia controla eficazmente el riesgo del capital y ha demostrado obtener buenos rendimientos en instrumentos de alta volatilidad. Con una mayor optimización y la combinación de indicadores, los resultados de la estrategia aún pueden mejorar.

- 1