Estrategia de RSI Estocástico Suavizado de Ehlers

Resumen

La idea principal de esta estrategia es utilizar el filtro SuperSmoother de Ehlers para procesar el indicador Stochastic RSI, filtrando así muchas señales falsas y obteniendo señales de trading más confiables. El principio básico consiste en calcular primero el Stochastic RSI, luego suavizarlo con el filtro SuperSmoother de Ehlers y, finalmente, utilizar los cruces con su propia media móvil para generar señales de compra y venta.

Principio de la Estrategia

La estrategia primero calcula el RSI del precio de cierre logarítmico y luego, basándose en el RSI, calcula el indicador Stochastic, que es un indicador típico de sobrecompra/sobreventa. Para filtrar señales falsas, se aplica el filtro SuperSmoother de Ehlers al Stochastic RSI. Finalmente, se generan señales de compra cuando la línea del Stochastic RSI cruza al alza su propia media móvil (cruce dorado) y de venta cuando cruza a la baja (cruce de la muerte). Por lo tanto, los puntos clave de esta estrategia son: 1) Calcular el indicador Stochastic RSI; 2) Utilizar el filtro SuperSmoother de Ehlers; 3) Generar señales de trading mediante el cruce con la media móvil.

Análisis de Ventajas

La mayor ventaja de esta estrategia es el uso del filtro SuperSmoother de Ehlers, que puede filtrar eficazmente muchas señales falsas, haciendo que las señales de trading sean más confiables. Además, el indicador Stochastic RSI en sí mismo tiene una buena capacidad de ruptura y seguimiento de tendencia. Por lo tanto, esta estrategia puede identificar correctamente la tendencia, abrir posiciones en el momento adecuado y cerrarlas también oportunamente.

Análisis de Riesgos

El principal riesgo de esta estrategia es que en mercados con fuertes oscilaciones laterales puede generar señales erróneas. Cuando el precio fluctúa ampliamente dentro de un rango estrecho, el indicador Stochastic RSI produce muchas señales falsas al alza y a la baja, y el efecto del filtro SuperSmoother de Ehlers también se ve reducido. Además, en ciertas condiciones de mercado volátiles, el retraso del indicador puede conllevar cierto riesgo.

Para reducir estos riesgos, se pueden ajustar los parámetros adecuadamente, como aumentar el período del indicador Stochastic o disminuir la suavidad, para filtrar aún más las señales falsas. También se puede considerar la combinación con otros indicadores o patrones para formar múltiples condiciones de filtrado y evitar el riesgo de señales erróneas.

Direcciones de Optimización

Esta estrategia se puede optimizar principalmente en los siguientes aspectos:

- Optimización de Parámetros. Se pueden probar minuciosamente parámetros como la longitud del Stochastic RSI y la constante de suavizado para encontrar la mejor combinación de parámetros.

- Incorporación de Mecanismo de Stop Loss. Se puede establecer un stop loss móvil o un stop loss fijo para asegurar ganancias y reducir la reducción máxima.

- Combinación con Otros Indicadores o Patrones. Se puede considerar la combinación con indicadores de volatilidad, medias móviles, etc., para formar múltiples condiciones de filtrado y reducir aún más el riesgo.

- Ajuste del Tamaño de Posición Basado en Análisis de Marco Temporal Mayor. Se puede ajustar dinámicamente el tamaño de cada operación según los resultados del análisis de tendencia en un marco temporal superior.

Conclusión

Esta estrategia primero calcula el indicador Stochastic RSI, luego lo procesa con el filtro SuperSmoother de Ehlers y, finalmente, genera señales de trading mediante el cruce con su propia media móvil, logrando un juicio correcto de la tendencia. La ventaja de la estrategia radica en la combinación del indicador y el filtro, que puede filtrar eficazmente las señales falsas y obtener oportunidades de trading de alta probabilidad. Los riesgos principales provienen de una configuración inadecuada de parámetros y la falta de un mecanismo de stop loss. Mediante la optimización de parámetros, la adición de stop loss y la combinación con otros elementos, se puede mejorar aún más la estabilidad y la rentabilidad de la estrategia.

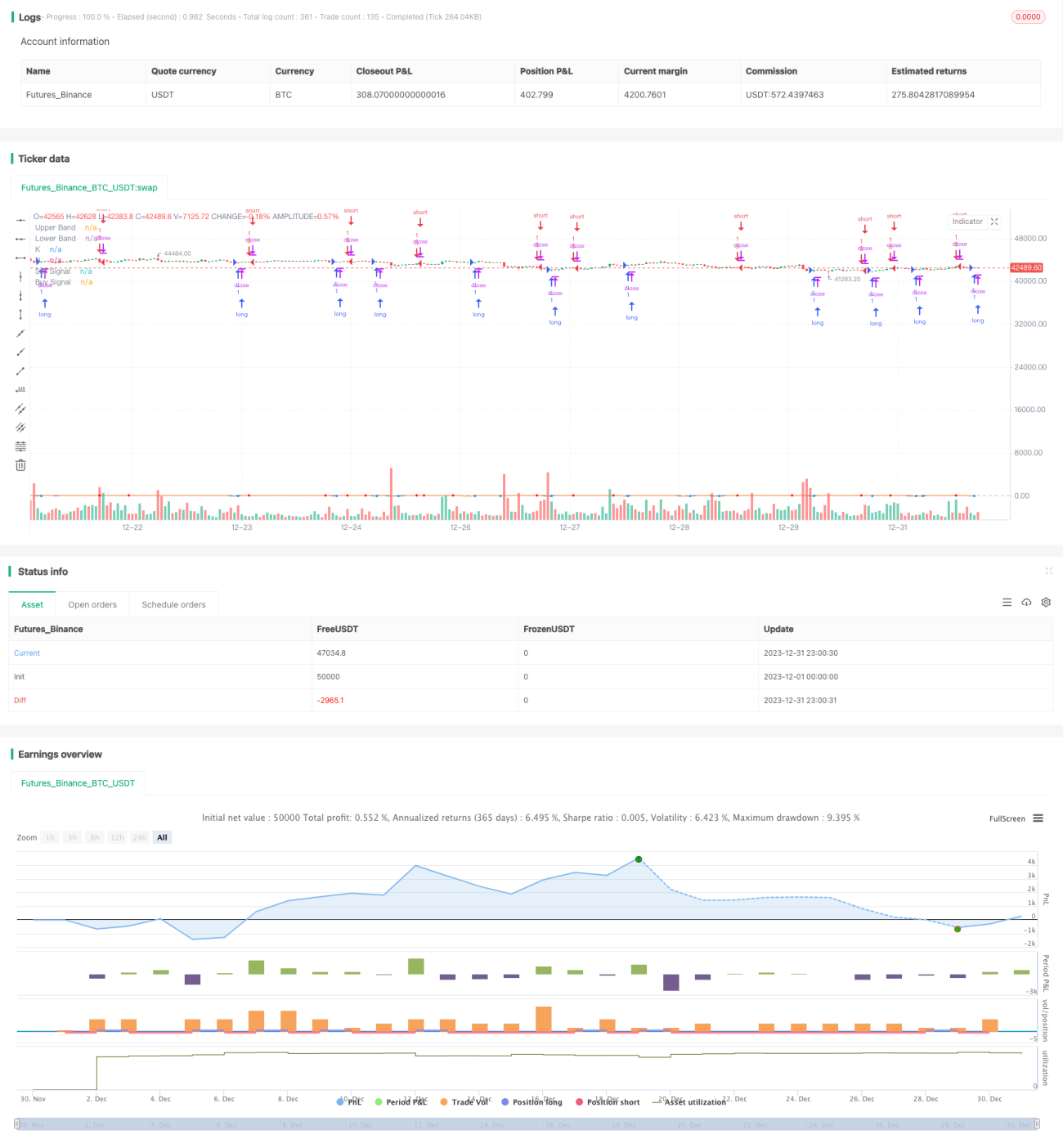

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("ES Stoch RSI Strategy [krypt]", overlay=true, calc_on_order_fills=true, calc_on_every_tick=true, initial_capital=10000, currency='USD')

//Backtest Range- 1