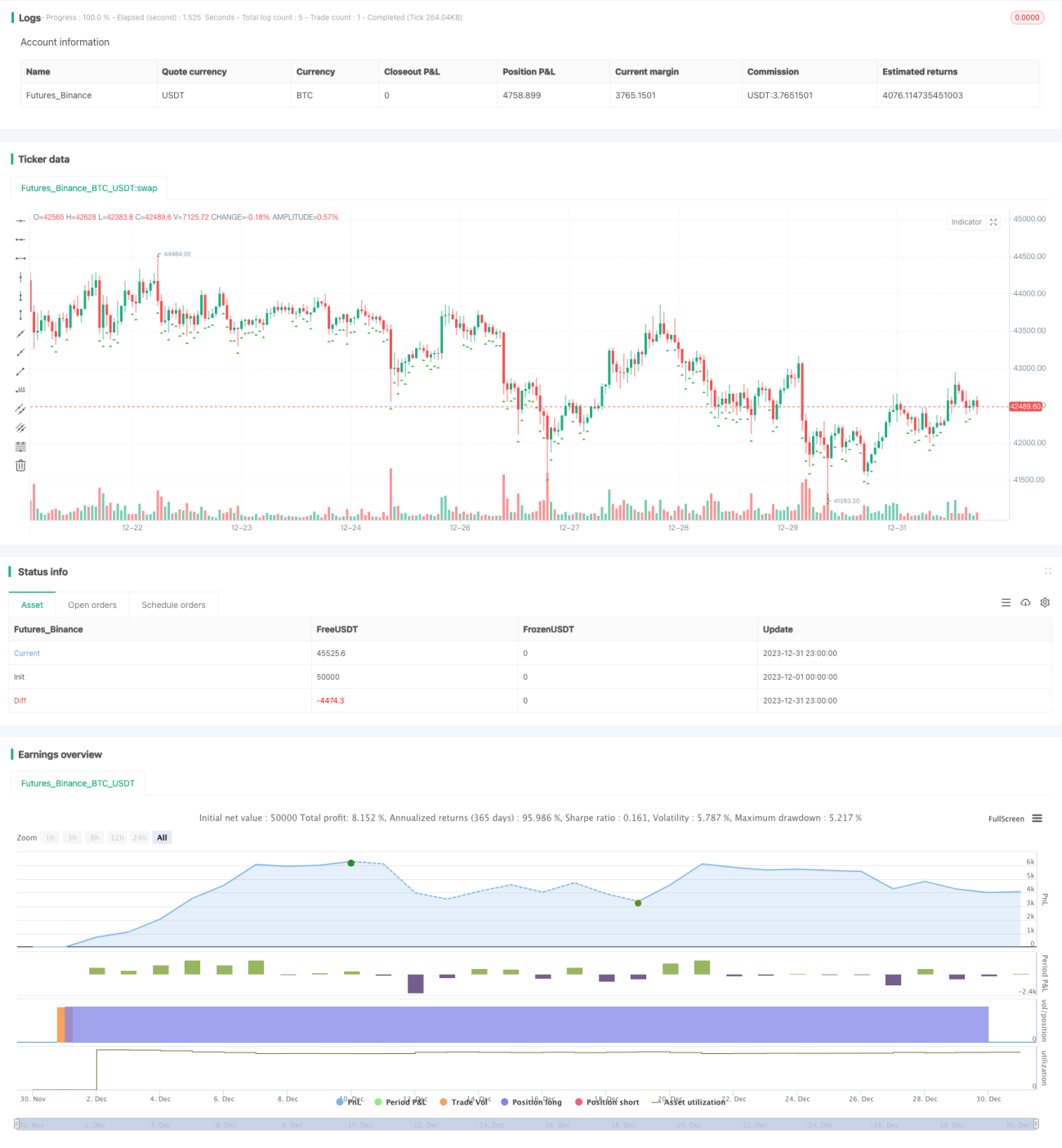

Estrategia de trading de succión del indicador RSI

Resumen

La estrategia de trading de succión con el indicador RSI es un método de trading en cuadrícula fija que integra los indicadores RSI y CCI. La estrategia determina el momento de entrada según los valores de los indicadores RSI y CCI, y utiliza un porcentaje de beneficio fijo y un número fijo de cuadrículas para establecer órdenes de toma de ganancias y de adición de posiciones. Además, integra un mecanismo de cobertura frente a movimientos de precios de ruptura.

Principio de la estrategia

Condiciones de entrada

Cuando los indicadores RSI de 5 minutos y 30 minutos están por debajo del umbral establecido, y el indicador CCI de 1 hora también está por debajo del valor establecido, se genera una señal de compra. En ese momento se registra el precio actual de cierre como precio de entrada, y se calcula el tamaño de la primera posición en función del capital de la cuenta y el número de cuadrículas.

Condiciones de toma de ganancias

Tomando el precio de entrada como referencia, se calcula el precio de beneficio según el porcentaje objetivo de ganancia establecido, y se coloca una orden de toma de ganancias en ese nivel de precio.

Condiciones de adición de posiciones

Excepto la primera posición, las órdenes de adición de las posiciones fijas restantes se lanzan una tras otra después de la señal de entrada, hasta alcanzar el número de cuadrículas establecido.

Mecanismo de cobertura

Si el precio sube más allá del porcentaje umbral de cobertura establecido respecto al precio de entrada, se cierran todas las posiciones mediante cobertura.

Mecanismo de reversión

Si el precio baja más allá del porcentaje umbral de reversión establecido respecto al precio de entrada, se cancelan todas las órdenes no ejecutadas y se espera una nueva oportunidad de entrada.

Análisis de ventajas

- Combinación de los indicadores RSI y CCI para aumentar la probabilidad de beneficio.

- Uso de cuadrículas fijas para establecer objetivos de ganancia, lo que aumenta la certeza de los beneficios.

- Integración de un mecanismo de cobertura para prevenir eficazmente el riesgo de fluctuaciones bruscas del precio.

- Incorporación de un mecanismo de reversión que puede reducir las pérdidas.

Análisis de riesgos

- Probabilidad de que los indicadores generen señales falsas.

- Fluctuaciones bruscas del precio que superen el umbral de cobertura.

- Imposibilidad de volver a entrar tras una reversión si el precio se da la vuelta de nuevo.

Estos riesgos pueden reducirse ajustando los parámetros de los indicadores, ampliando el margen de cobertura y reduciendo el margen de reversión.

Direcciones de optimización

- Se pueden probar más combinaciones de indicadores.

- Se puede investigar un mecanismo de toma de ganancias adaptativo.

- Se puede optimizar la lógica de adición de posiciones.

Resumen

La estrategia de trading de succión con el indicador RSI determina el momento de entrada mediante indicadores, y utiliza cuadrículas fijas para la toma de ganancias y la adición de posiciones con el fin de asegurar beneficios estables. Además, la estrategia cuenta con mecanismos de cobertura ante grandes fluctuaciones y de reingreso tras reversiones. Esta estrategia que integra múltiples mecanismos puede utilizarse para reducir el riesgo de trading y aumentar la tasa de ganancias. Mediante una mayor optimización de los indicadores y el ajuste de parámetros, se pueden obtener mejores resultados en el trading real.

- 1