Donchian Channel Breakout Strategy

Overview

The Donchian channel breakout strategy is a trend following strategy. It forms a price channel by calculating the highest and lowest prices over a certain period of time and uses the channel boundaries as buy and sell signals. It goes short when the price breaks through the upper rail and goes long when the price breaks through the lower rail. This strategy is suitable for highly volatile cryptocurrency trading.

Strategy Logic

This strategy uses the Donchian Channel indicator to determine price trends and calculate entry and exit points. The Donchian Channel consists of an upper rail, lower rail and middle rail. The upper rail is the highest price over a certain period, the lower rail is the lowest price, and the middle rail is the average price.

The entry and exit period lengths can be configured independently. When the price breaks through the lower rail upward, it goes long. When the price breaks through the upper rail downward, it goes short. The exit point is when the price touches the corresponding rail again. The middle rail can also be used as a stop loss line.

In addition, the strategy also sets a take profit point. The take profit price for long positions is the entry price multiplied by (1 + take profit percentage), and vice versa for short positions. Enabling this feature locks in profits and prevents losses from expanding.

In summary, while judging the trend, this strategy ensures sufficient room to set stops and take profits. This makes it particularly suitable for highly volatile assets like cryptocurrencies.

Advantage Analysis

The advantages of this strategy include:

- Clear signal logic and simple/reliable signal generation.

- The Donchian Channel indicator is insensitive to price fluctuations, which helps capture the trend.

- Customizable channel parameters to suit different assets and timeframes.

- Built-in stop loss/take profit functions effectively control risk.

- High profit potential for volatile assets like cryptocurrencies.

Risk Analysis

The risks of this strategy include:

- Unable to fully avoid risks from huge price swings despite stop loss.

- Improper parameter settings may lead to over-trading, increasing costs.

- Insensitive to price fluctuations, may miss some trading opportunities.

To mitigate the above risks:

- Appropriately size positions and diversify across assets to control overall risk.

- Optimize parameters to find the best combination, possibly using machine learning.

- Incorporate additional indicators to determine signal reliability.

Optimization Directions

This strategy can be further optimized in the following dimensions:

- Test and optimize more parameter combinations to find the optimum values. Key parameters include channel periods, take profit percentage, allowing long/short etc.

- Incorporate machine learning models to automatically identify optimal parameters, e.g. using reinforcement learning.

- Combine other indicators like moving averages and volume to determine trend and signal reliability.

- Develop more advanced stop loss strategies e.g. trailing stop loss, Chandelier Exit etc. to better control risks.

- Expand strategy across more asset classes to find the best fit.

Conclusion

In conclusion, the Donchian channel breakout strategy provides clear signals and controllable risks for trend trading. It is especially suitable for volatile assets like cryptocurrencies with great profit potential. There are also possibilities to further optimize parameters and incorporate other indicators, which are avenues for future enhancements. With continuous innovations, this strategy has the potential to become an important algorithmic trading strategy for cryptocurrencies.

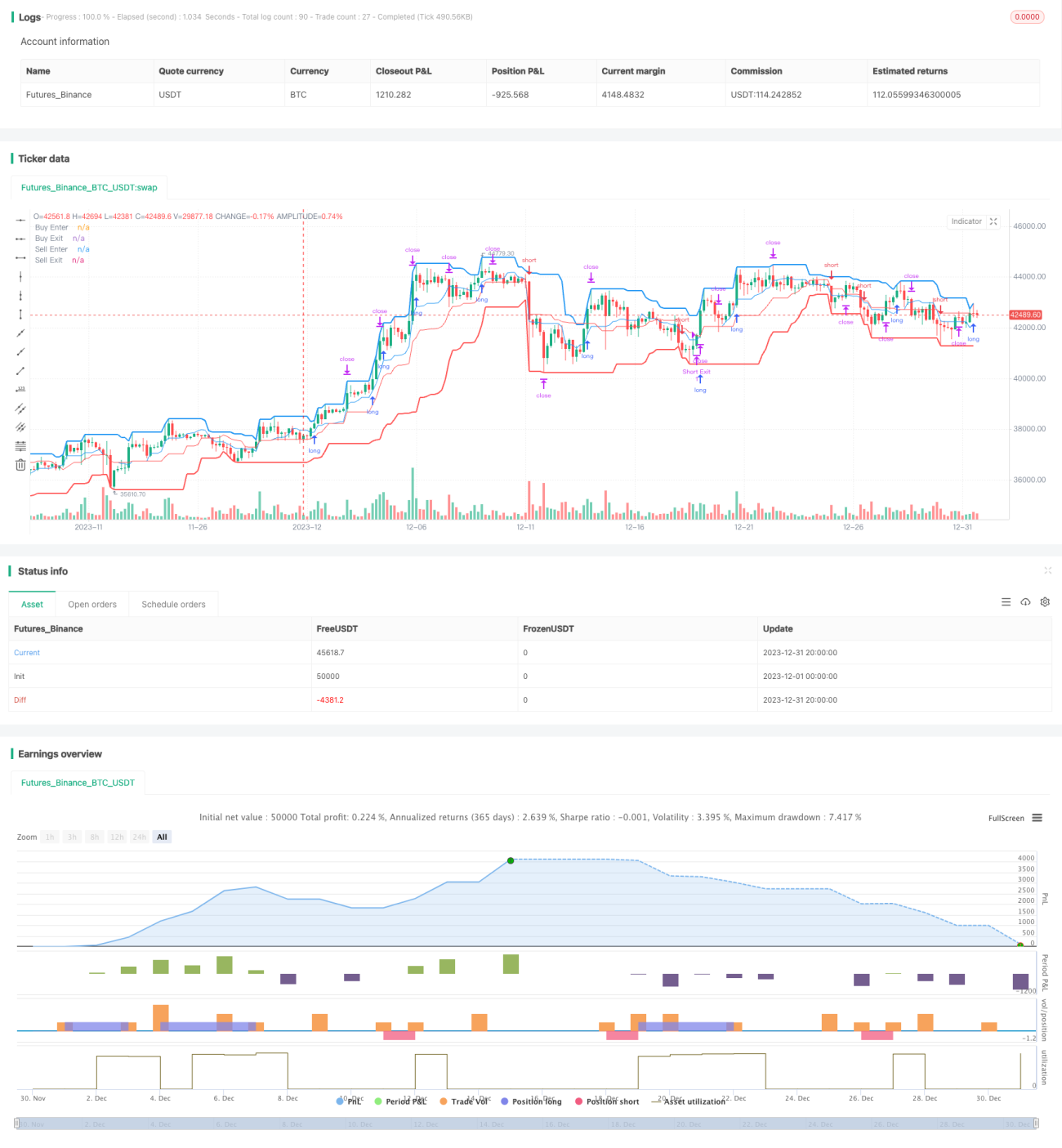

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © algotradingcc

// Strategy testing and optimisation for free trading bot

- 1