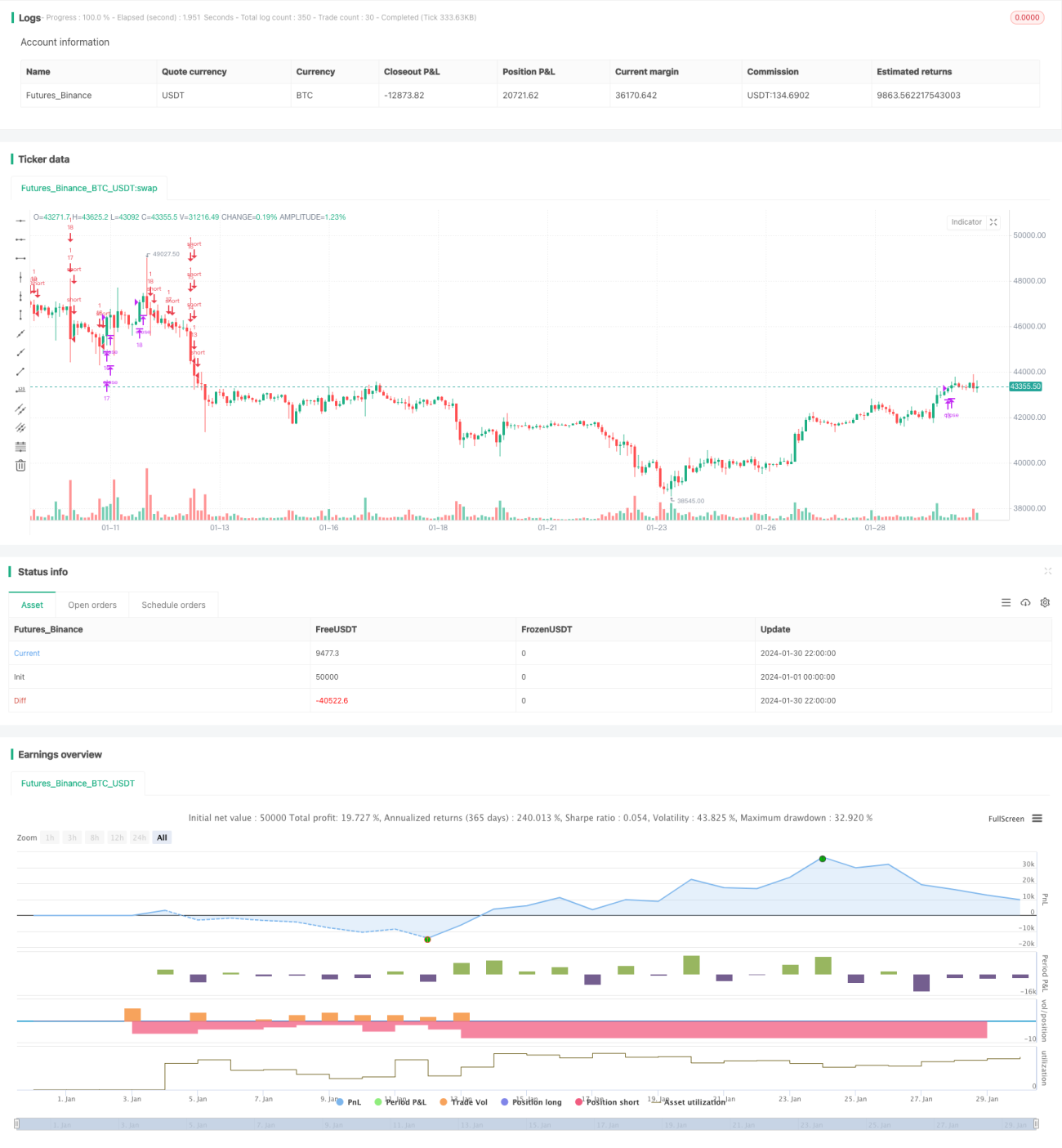

Estrategia de seguimiento de velas en cuadrícula bidireccional

Resumen

Esta estrategia es una estrategia de trading de rejilla bidireccional basada en cambios en tiempo real de las velas. Puede obtener ganancias estables tanto en mercados alcistas como bajistas.

Principio de la estrategia

-

Basado en la cantidad de rejillas configurada por el usuario, calcula automáticamente el rango de precios de la rejilla y el precio de cada rejilla.

-

Cuando el precio supera el precio de la rejilla, abre una posición larga con una cantidad fija; cuando el precio cae por debajo del precio de la rejilla, cierra la posición larga y abre una posición corta.

-

De esta manera, cuando el precio oscila dentro del rango de la rejilla, se pueden obtener ganancias siguiendo los cambios de precio.

Análisis de ventajas

-

Calcula automáticamente un rango de rejilla razonable, sin necesidad de determinar manualmente los soportes y resistencias.

-

Operación bidireccional, adaptable a entornos de mercado cambiantes.

-

Cantidad fija de apertura de posiciones, favorable para el control de riesgos.

-

Código intuitivo y conciso, fácil de entender y modificar.

Análisis de riesgos

-

Las fluctuaciones violentas del mercado pueden provocar pérdidas ampliadas.

-

La acumulación de comisiones de transacción también afecta las ganancias finales.

-

Es necesario determinar razonablemente la cantidad de rejillas; demasiadas rejillas aumentan la frecuencia de operaciones pero cada ganancia es limitada.

Direcciones de optimización

-

Incorporar una estrategia de stop loss para evitar la ampliación de pérdidas.

-

Agregar una función de ajuste dinámico de la cantidad de rejillas.

-

Considerar la inclusión de apalancamiento para ampliar el volumen de operaciones.

Conclusión

La idea general de esta estrategia es clara y concisa. Obtiene ganancias estables mediante el trading de rejilla bidireccional, aunque también conlleva ciertos riesgos comerciales. Mediante una optimización continua, se espera lograr mejores resultados.

- 1