Estrategia de seguimiento de tendencia con bandas de Bollinger adaptativas bidireccionales

Resumen

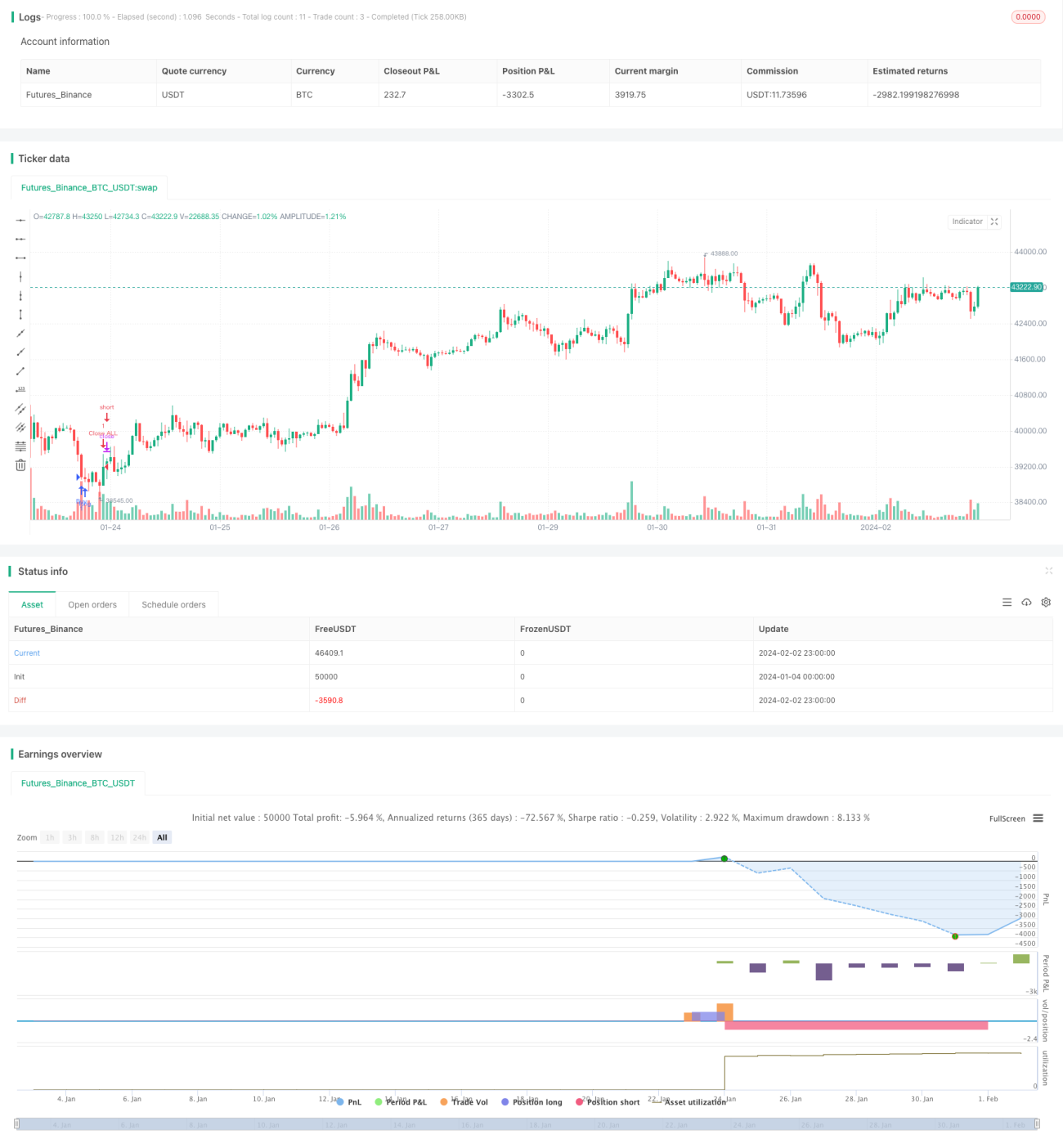

Esta estrategia utiliza el indicador de Bandas de Bollinger adaptativas bidireccionales para identificar la dirección de la tendencia, y combina órdenes de mercado para realizar un trailing stop, logrando un seguimiento de tendencia de alta eficiencia.

Principio de la estrategia

- Calcular la banda media, la banda superior y la banda inferior de Bollinger según un período determinado.

- Si el precio supera la banda superior, se abre una posición larga con trailing; si rompe la banda inferior, se abre una posición corta con trailing.

- Utilizar órdenes de mercado para entrar rápidamente.

- Establecer niveles de stop loss y take profit para la gestión de la posición.

Análisis de ventajas

- El indicador de Bandas de Bollinger adaptativas es sensible a la volatilidad del mercado y puede detectar rápidamente los cambios de tendencia.

- El uso de órdenes de mercado permite una entrada rápida, reduciendo el riesgo de deslizamiento.

- Stop loss y take profit automáticos para controlar estrictamente el riesgo y asegurar ganancias.

Análisis de riesgos

- Las Bandas de Bollinger tienen un rezago inherente y no pueden evitar completamente las falsas rupturas.

- Las órdenes de mercado no permiten controlar el precio de ejecución.

- Es necesario configurar adecuadamente los niveles de stop loss y take profit.

Direcciones de optimización

- Ajustar los parámetros de las Bandas de Bollinger para optimizar la sensibilidad en la detección de tendencias.

- Agregar indicadores como el volumen o el MACD para filtrar falsas rupturas.

- Optimizar la configuración de los niveles de stop loss y take profit.

Conclusión

Esta estrategia aprovecha al máximo la capacidad de las Bandas de Bollinger para identificar la dirección y los cambios de tendencia, combinada con órdenes de mercado de salida rápida para un seguimiento bidireccional, obteniendo rendimientos excesivos bajo un control de riesgo adecuado. Mediante una mayor optimización de los parámetros de las Bandas de Bollinger, la incorporación de indicadores de filtrado auxiliares y el ajuste de la lógica de stop loss y take profit, se puede lograr un mejor rendimiento de la estrategia. Esta estrategia es clara y fácil de implementar, constituyendo una estrategia de seguimiento de tendencia eficiente y confiable.

- 1