Estrategia de seguimiento de tendencia por cruce de medias móviles

Resumen

La estrategia de seguimiento de tendencia con cruce de medias móviles es una estrategia de trading cuantitativo que persigue las tendencias del mercado. Esta estrategia calcula una media móvil rápida y una media móvil lenta, y genera señales de trading cuando se cruzan, con el objetivo de capturar los puntos de inflexión de la tendencia del mercado.

Principio de la estrategia

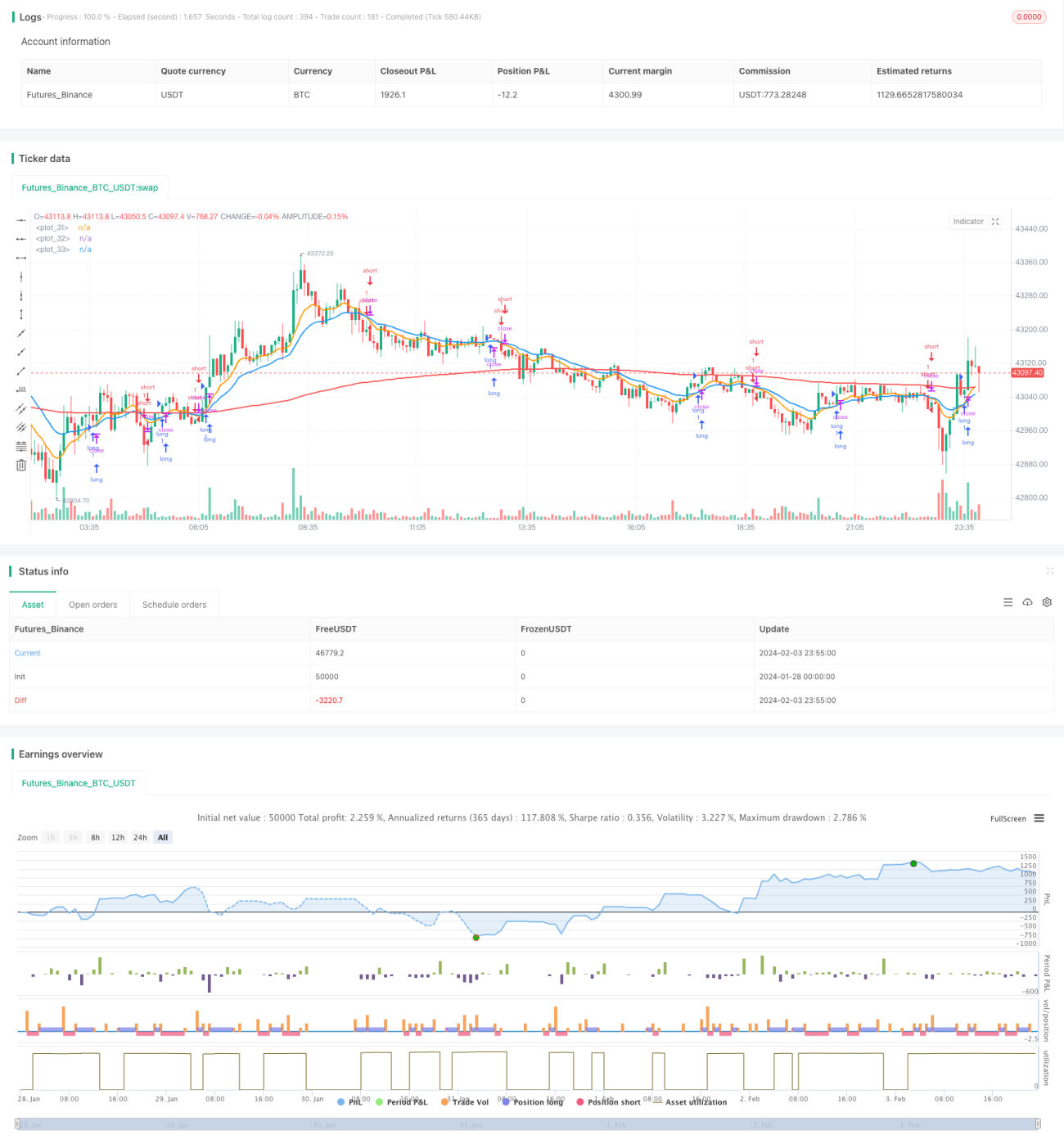

El principio central de esta estrategia es utilizar medias móviles exponenciales (EMA) con diferentes parámetros para determinar la tendencia del mercado. La estrategia define una EMA rápida y una EMA lenta. Cuando la EMA rápida cruza por encima de la EMA lenta desde abajo, indica que la tendencia del mercado se vuelve alcista; cuando la EMA rápida cruza por debajo de la EMA lenta desde arriba, indica que la tendencia del mercado se vuelve bajista.

En el cruce al alza, la estrategia abre una posición larga; en el cruce a la baja, abre una posición corta. La estrategia mantiene la posición hasta que se active un take profit o stop loss, o hasta que se produzca nuevamente una señal de cruce en dirección contraria.

Análisis de ventajas

Esta estrategia tiene las siguientes ventajas:

- La lógica de la estrategia es simple y clara, fácil de entender e implementar, adecuada para principiantes;

- Al utilizar EMA para suavizar los precios, puede filtrar eficazmente el ruido del mercado e identificar tendencias;

- Los parámetros se pueden ajustar de manera flexible para adaptarse a mercados de diferentes períodos;

- Se puede expandir a una versión de múltiples marcos temporales para mejorar la estabilidad.

Análisis de riesgos

Esta estrategia también presenta algunos riesgos:

- En mercados laterales, pueden ocurrir múltiples stops, afectando la rentabilidad;

- No puede identificar eficazmente el tipo de tendencia (alcista o bajista), lo que podría generar pérdidas significativas;

- Una configuración inadecuada de los parámetros de la EMA puede provocar una frecuencia de trading excesiva o un retraso en la identificación.

Para reducir el riesgo, se puede considerar combinar otros indicadores para identificar el tipo de tendencia, o establecer un stop loss más amplio.

Direcciones de optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

- Agregar juicio sobre el tipo de tendencia para evitar abrir posiciones en dirección contraria;

- Incorporar múltiples marcos temporales para mejorar la calidad de las señales;

- Ajustar dinámicamente los ratios de take profit y stop loss para optimizar los puntos de salida;

- Combinar otros indicadores para filtrar señales y reducir operaciones erróneas.

Conclusión

En general, la estrategia de seguimiento de tendencia con cruce de medias móviles es una estrategia de trading de tendencias simple y práctica. Su idea central es clara y fácil de poner en práctica, aunque también tiene cierto margen de optimización. Mediante el ajuste de parámetros, el juicio de múltiples marcos temporales y el stop loss dinámico, se puede mejorar continuamente la estabilidad y la rentabilidad de la estrategia.

- 1