Estrategia de trading de línea de tendencia de pendiente dinámica

Resumen

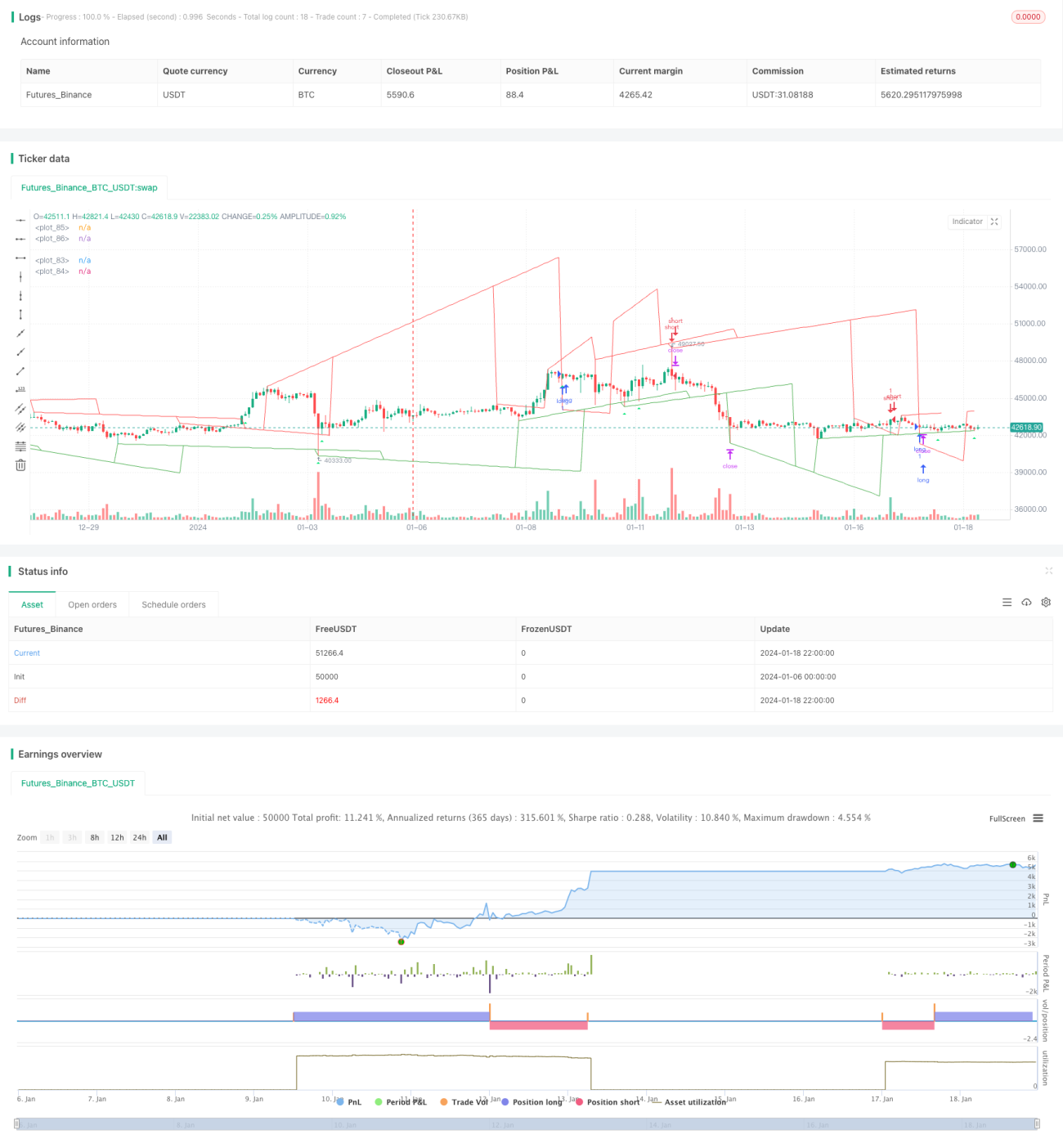

La idea central de esta estrategia es utilizar la pendiente dinámica para determinar la dirección de la tendencia del precio, combinada con la ruptura para generar señales de trading. Específicamente, realiza un seguimiento en tiempo real de los nuevos máximos y mínimos del precio, calcula la pendiente dinámica en función de los cambios de precio en diferentes períodos de tiempo y luego combina la ruptura del precio con la línea de tendencia para determinar señales largas o cortas.

Principio de la estrategia

Esta estrategia se divide principalmente en los siguientes pasos:

- Determinar los precios máximos y mínimos: Realiza un seguimiento del precio máximo y mínimo dentro de un período determinado (por ejemplo, 20 velas) para determinar si se ha alcanzado un nuevo máximo o mínimo.

- Calcular la pendiente dinámica: Registra el número de vela en la que se alcanza un nuevo máximo o mínimo y calcula la pendiente dinámica desde el punto de máximo/mínimo hasta un punto después de un período determinado (por ejemplo, 9 velas).

- Dibujar líneas de tendencia: Según la pendiente dinámica, dibuja líneas de tendencia ascendentes y descendentes.

- Extender y actualizar líneas de tendencia: Cuando el precio rompe la línea de tendencia, se extiende y actualiza la línea de tendencia.

- Señal de trading: En combinación con la ruptura del precio de la línea de tendencia, se determinan las señales de compra y venta.

Ventajas de la estrategia

Esta estrategia tiene las siguientes ventajas:

- Determina dinámicamente la dirección de la tendencia, respondiendo de manera flexible a los cambios del mercado.

- Puede controlar razonablemente el stop-loss, con pequeñas reducciones.

- Señales de ruptura claras e implementación sencilla.

- Parámetros personalizables, alta adaptabilidad.

- Estructura de código clara, fácil de entender y desarrollar sobre ella.

Riesgos y soluciones

Esta estrategia también presenta algunos riesgos:

- Múltiples señales falsas durante la consolidación de la tendencia: Se recomienda añadir condiciones de filtro.

- Posibles muchas señales falsas de ruptura: Se pueden ajustar los parámetros o añadir condiciones de filtro.

- Riesgo de stop-loss durante movimientos bruscos del mercado: Se puede aumentar el margen del stop-loss.

- Espacio de optimización limitado, rentabilidad restringida, adecuada para trading a corto plazo.

Direcciones de optimización

Los aspectos optimizables de esta estrategia incluyen:

- Añadir más indicadores técnicos para filtrar señales.

- Optimizar combinaciones de parámetros para encontrar los parámetros óptimos.

- Intentar mejorar la estrategia de stop-loss para reducir el riesgo.

- Añadir una función de ajuste automático de la amplitud de entrada.

- Intentar combinar con otras estrategias para descubrir más oportunidades.

Conclusión

En general, esta estrategia es una estrategia eficiente de trading a corto plazo basada en la pendiente dinámica para determinar la tendencia y operar en rupturas. Es precisa en su determinación, tiene un riesgo controlable y es adecuada para capturar oportunidades a corto plazo en el mercado. Mediante una mayor optimización de parámetros y la adición de condiciones de filtro, se pueden mejorar la tasa de acierto y el nivel de rentabilidad de la estrategia.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1