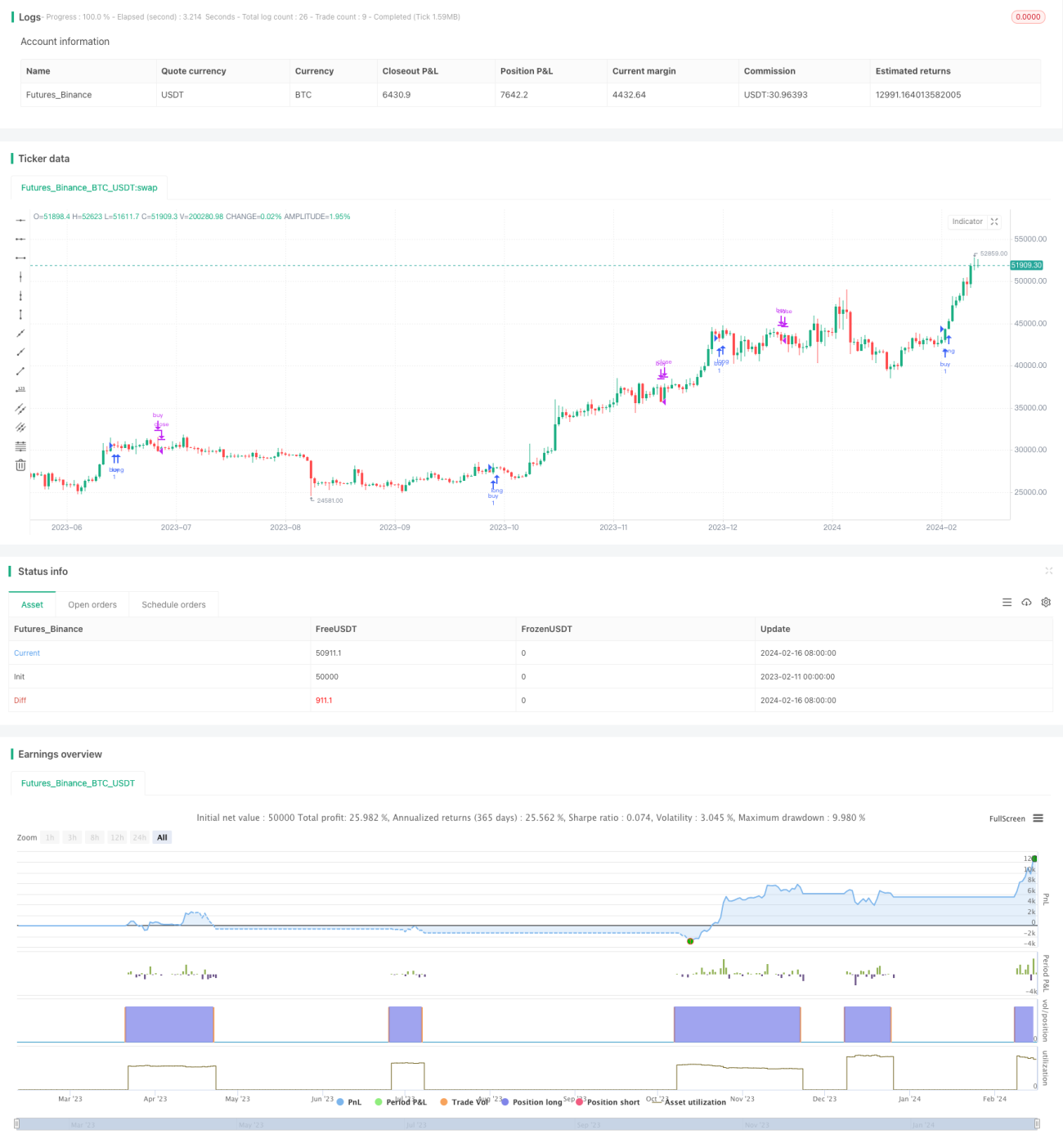

Estrategia de trading basada en el Índice de Fuerza Relativa y el Estocástico RSI

Resumen

Esta estrategia de trading combina dos indicadores técnicos: el índice de fuerza relativa (RSI) y el RSI estocástico (Stochastic RSI) para generar señales de trading. Además, utiliza la acción del precio de las criptomonedas en un marco temporal superior para confirmar la tendencia, mejorando así la fiabilidad de las señales.

Nombre de la estrategia

Estrategia de trading RSI-SRSI de múltiples marcos temporales (Multi Timeframe RSI-SRSI Trading Strategy)

Principio de la estrategia

La estrategia utiliza los valores del RSI para determinar condiciones de sobrecompra y sobreventa. Cuando el RSI está por debajo de 30, se considera una señal de sobreventa; por encima de 70, una señal de sobrecompra. El indicador Stochastic RSI observa la volatilidad del propio RSI. Un Stochastic RSI por debajo de 5 indica sobreventa, y por encima de 50, sobrecompra.

La estrategia también combina la acción del precio de la criptomoneda en un marco temporal superior (por ejemplo, semanal). Solo cuando el RSI del marco temporal superior supera un umbral (por ejemplo, 45) se genera una señal de compra. Este ajuste filtra las señales de sobreventa no persistentes que ocurren durante una tendencia bajista general.

Tras activarse, las señales de compra y venta requieren una confirmación de un cierto período (por ejemplo, 8 velas) para evitar señales engañosas.

Ventajas de la estrategia

- Método clásico de análisis técnico que utiliza el RSI para identificar sobrecompra/sobreventa.

- Combina el Stochastic RSI para detectar reversiones del propio RSI.

- Aplica un análisis de múltiples marcos temporales para filtrar señales engañosas y mejorar la calidad de las señales.

Riesgos de la estrategia y soluciones

- El RSI puede generar señales falsas con facilidad.

- Combinar con otros indicadores para filtrar señales engañosas.

- Aplicar técnicas de confirmación de tendencia.

- Si los umbrales no se configuran adecuadamente, se pueden generar demasiadas señales de trading.

- Optimizar la combinación de parámetros para encontrar los valores óptimos.

- Las señales de compra/venta requieren un tiempo de confirmación.

- Encontrar un período de confirmación equilibrado que filtre señales engañosas sin perder oportunidades.

Direcciones de optimización de la estrategia

- Probar más combinaciones de indicadores para buscar señales más sólidas.

- Por ejemplo, añadir el indicador MACD a la estrategia.

- Intentar usar métodos de aprendizaje automático para encontrar parámetros óptimos.

- Utilizar algoritmos genéticos/algoritmos evolutivos para la optimización automática.

- Agregar una estrategia de stop loss para controlar el riesgo por operación.

- Detener la pérdida cuando el precio rompe un nivel de soporte.

Resumen

Esta estrategia se basa principalmente en los dos indicadores clásicos RSI y Stochastic RSI para generar señales de trading. Además, introduce un marco temporal superior para la confirmación de la tendencia, lo que filtra eficazmente las señales engañosas y mejora la calidad de las señales. Mediante la optimización de parámetros y la aplicación de stop loss, se puede mejorar aún más el rendimiento de la estrategia. Esta estrategia es simple, directa y fácil de entender e implementar, lo que la convierte en un excelente punto de partida para el trading cuantitativo.

- 1