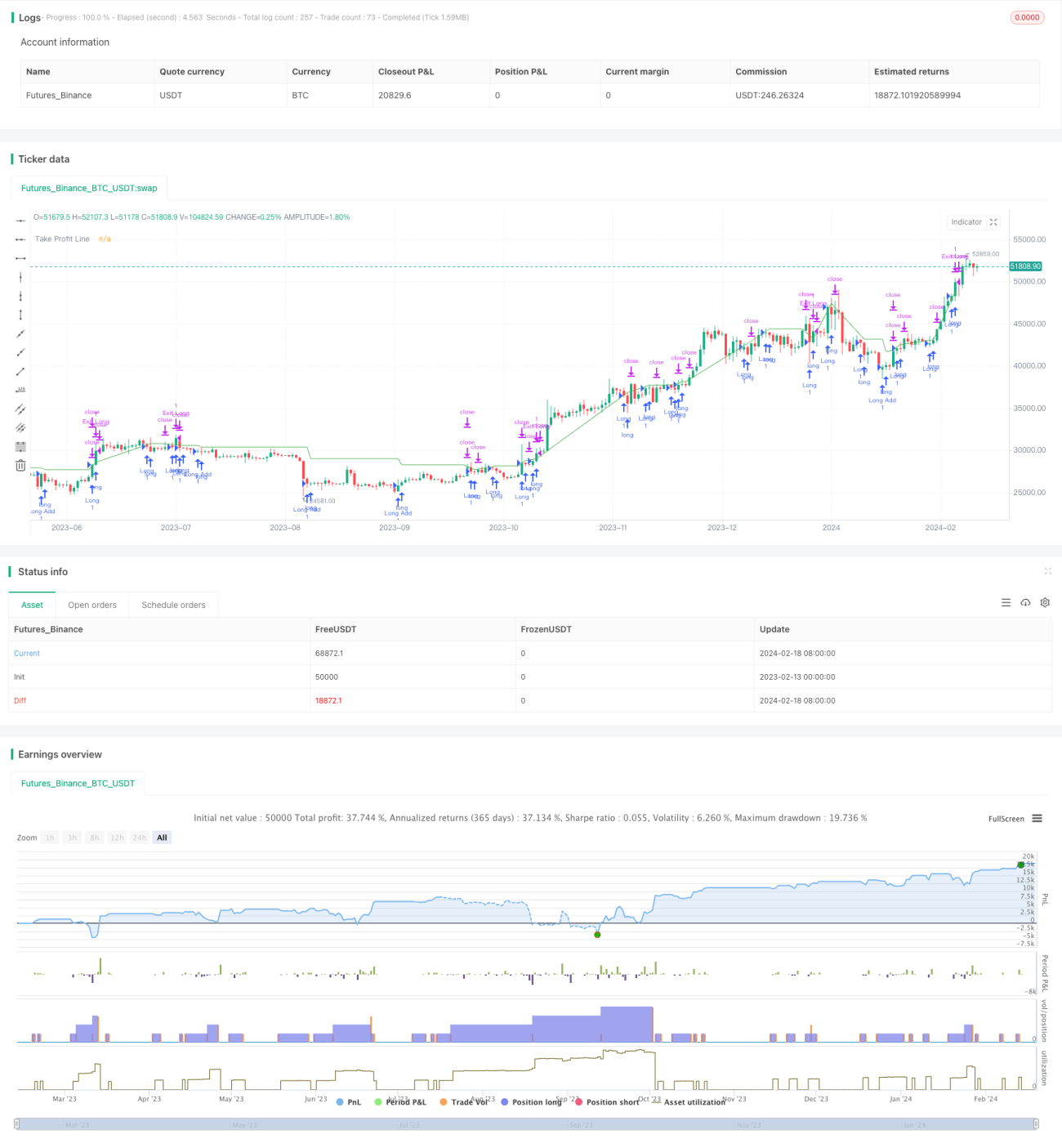

Estrategia de trading cuantitativa basada en múltiples factores

Resumen

Esta estrategia utiliza múltiples indicadores técnicos como RSI, MACD, OBV, CCI, CMF, MFI y VWMACD para detectar divergencias entre el precio y el volumen, identificando posibles puntos de entrada. La estrategia también incorpora un indicador de detección de caídas definido por el usuario, que emite señales de trading cuando se cumplen condiciones de alta volatilidad y profundidad o VFI. La estrategia solo opera en largo, utilizando un trailing stop para agregar posiciones gradualmente.

Principio de la estrategia

-

Calcula indicadores como RSI, MACD, OBV, CCI, CMF, MFI y VWMACD, y mediante un método de regresión lineal adaptativa detecta divergencias entre cada indicador y el precio histórico. Cuando un indicador alcanza un nuevo mínimo pero el precio no lo sigue, se genera una señal de compra.

-

Basándose en umbrales de volatilidad y porcentaje de profundidad proporcionados por el usuario, junto con un filtro del indicador VFI, emite señales en las velas que cumplen condiciones de alta volatilidad y prueba de profundidad.

-

Tras la primera operación larga, si el precio cae por debajo de un cierto porcentaje (configurable) del último precio de compra, se añade otra posición larga.

-

Utiliza un trailing stop; cuando se alcanza el porcentaje de take profit configurado, se cierra la posición.

Ventajas

-

Combinación multifactorial, integrando indicadores de precio y volumen para aumentar la fiabilidad de las señales.

-

El método de regresión lineal adaptativa para detectar divergencias evita la subjetividad en el juicio humano.

-

La incorporación de indicadores de volatilidad y profundidad/VFI ayuda a identificar oportunidades de reversión.

-

La acumulación gradual de posiciones aprovecha las correcciones de precio, y el trailing stop facilita la fijación de ganancias.

Análisis de riesgos

-

El juicio multifactorial es complejo; la optimización de parámetros y la efectividad de la detección de divergencias pueden afectar el rendimiento real.

-

El riesgo de mantener posiciones unidireccionales es alto; un error de juicio puede causar pérdidas significativas.

-

En el modo de adición repetida de posiciones, las pérdidas también se amplifican, requiriendo un control cuidadoso del tamaño de la posición.

-

Es necesario considerar el impacto de las comisiones de trading en las ganancias reales.

Direcciones de optimización

-

Probar diferentes combinaciones de parámetros e indicadores para seleccionar la configuración óptima.

-

Agregar una estrategia de stop loss para controlar pérdidas individuales y máximas.

-

Considerar oportunidades de trading en ambos sentidos para diversificar el riesgo.

-

Utilizar métodos de aprendizaje automático para optimizar automáticamente los parámetros.

Conclusión

Esta estrategia combina múltiples indicadores técnicos para identificar puntos de entrada, mientras utiliza condiciones definidas por el usuario y el filtro VFI para descartar señales falsas. La estrategia aprovecha las correcciones de precio para acumular posiciones, lo que ayuda a capturar oportunidades en tendencias. Sin embargo, también enfrenta riesgos de juicio erróneo y posiciones unidireccionales, por lo que es necesario optimizar parámetros de indicadores y estrategias de stop loss para reducir el riesgo y aumentar el potencial de ganancias.

- 1