Stratégie de break-out de Super Trend multi-timeframes avec oscillation

Aperçu

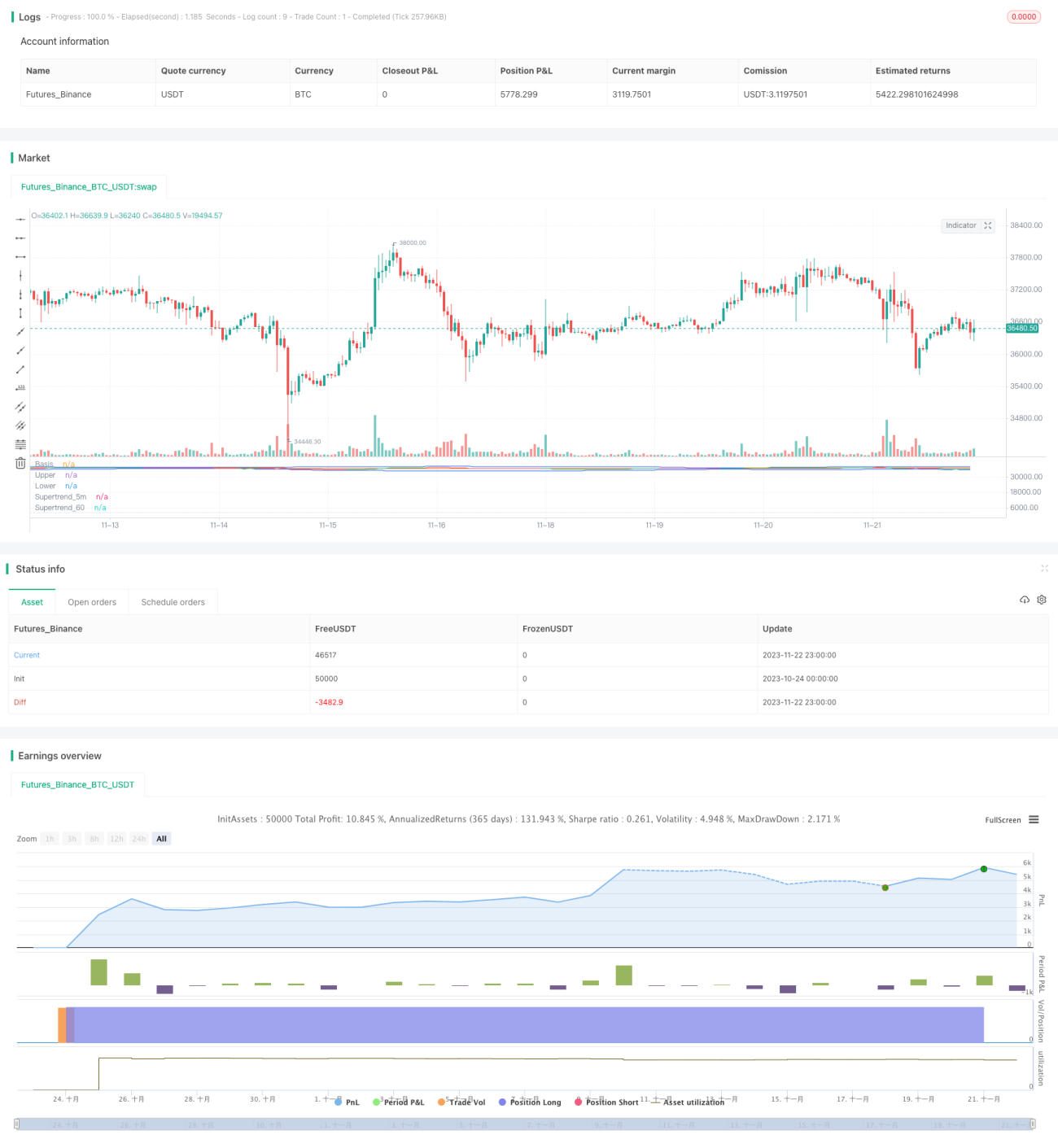

Cette stratégie combine l'indicateur SuperTrend multi-trames avec les bandes de Bollinger pour identifier la direction de la tendance et les niveaux clés de support et de résistance. Elle effectue des entrées lors des cassures en période de volatilité et quitte les positions sur croisement. La stratégie est principalement adaptée aux contrats à terme sur matières premières très volatiles, tels que l'or, l'argent, le pétrole brut, etc.

Principe de la stratégie

Basée sur la fonction personnalisée pine_supertrend(), elle utilise le SuperTrend multi-trames (par exemple 1 minute et 5 minutes) pour déterminer la direction de la tendance sur la période supérieure.

Parallèlement, elle calcule les bandes supérieure et inférieure de Bollinger pour détecter les cassures de canal. Lorsque le prix dépasse la bande supérieure, cela est considéré comme une cassure haussière ; lorsqu'il passe sous la bande inférieure, cela est considéré comme une cassure baissière.

Signaux de la stratégie :

Signal haussier : prix de clôture > bande supérieure de Bollinger ET prix de clôture > indicateur SuperTrend multi-trames.

Signal baissier : prix de clôture < bande inférieure de Bollinger ET prix de clôture < indicateur SuperTrend multi-trames.

Stop-loss :

Stop-loss haussier : prix de clôture < indicateur SuperTrend 5 minutes.

Stop-loss baissier : prix de clôture > indicateur SuperTrend 5 minutes.

Ainsi, la stratégie capture les cassures en résonance entre l'indicateur SuperTrend et les bandes de Bollinger, et exécute des transactions lors des phases de forte volatilité.

Analyse des avantages

- Utilise l'indicateur SuperTrend multi-trames pour déterminer la direction de la tendance sur la période supérieure, améliorant ainsi la qualité des signaux.

- Les bandes supérieure et inférieure de Bollinger servent de niveaux clés de support et de résistance, réduisant les fausses cassures.

- L'indicateur SuperTrend sert de niveau de stop-loss, limitant les pertes et contrôlant le risque.

Analyse des risques

- L'indicateur SuperTrend présente un décalage (lag) et peut manquer les points de retournement de tendance.

- Un paramétrage inapproprié des bandes de Bollinger peut entraîner des transactions trop fréquentes ou au contraire trop peu nombreuses.

- Les séances de nuit ou les événements majeurs sur les marchés de matières premières peuvent provoquer des mouvements de prix violents, déclenchant facilement le stop-loss.

Solutions aux risques :

- Combiner plusieurs indicateurs auxiliaires pour confirmer les signaux et éviter les fausses cassures.

- Optimiser les paramètres des bandes de Bollinger pour trouver le meilleur équilibre.

- Ajuster la position du stop-loss en élargissant l'écart.

Pistes d'optimisation

- Tester d'autres indicateurs de tendance, tels que KDJ, MACD, comme aide à la décision.

- Ajouter un modèle d'apprentissage automatique pour évaluer la probabilité en soutien.

- Effectuer une optimisation des paramètres pour trouver la meilleure combinaison d'hyperparamètres.

Résumé

Cette stratégie intègre deux indicateurs performants, le SuperTrend et les bandes de Bollinger, en s'appuyant sur une analyse multi-trames et la détection de cassures de canal pour réaliser des transactions à haute probabilité. Elle contrôle efficacement le risque et démontre sa capacité à générer de bons rendements sur les actifs très volatils. Grâce à une optimisation supplémentaire et à la combinaison d'indicateurs, son efficacité peut encore être améliorée.

- 1