Stratégie de suivi de momentum adaptatif multi-facteurs

Aperçu

La stratégie de suivi de momentum adaptatif multi-facteurs identifie les tendances du marché et les niveaux clés de support/résistance en intégrant plusieurs indicateurs techniques, permettant un trading automatisé sur des actifs très volatils comme les crypto-monnaies. Cette stratégie utilise des indicateurs tels que RSI, MACD, Stochastic pour déterminer les moments d'achat/vente, tout en combinant les pourcentages de variation de prix pour une reconnaissance plus précise des formations.

Principe de la stratégie

Le cœur de la stratégie de suivi de momentum adaptatif multi-facteurs réside dans l'intégration de multiples indicateurs techniques. La stratégie repose principalement sur les éléments suivants :

-

L'indicateur RSI pour identifier les conditions de surachat/survente. En combinant différents paramètres, il permet de détecter les signaux RSI standard ou les signaux RSI de Connor améliorés, afin d'identifier d'éventuelles opportunités de retournement.

-

L'indicateur MACD aide à déterminer la direction de la tendance. Un croisement à la hausse ou à la baisse de la ligne MACD avec la ligne de signal génère des signaux d'achat et de vente.

-

L'indicateur Stochastic repère les zones de surachat/survente. Les signaux de croisement (golden cross / death cross) entre la ligne K et la ligne D permettent de juger d'un éventuel retournement.

-

Le pourcentage de variation de prix vérifie la validité d'une cassure. En calculant le pourcentage de variation du plus haut, du plus bas et du cours de clôture sur une période donnée, on détermine si une cassure réelle s'est produite.

-

L'indicateur EMA identifie la tendance long-terme (haussière/baissière). Un croisement à la hausse de la moyenne rapide au-dessus de la moyenne lente est un signal haussier, l'inverse étant baissier.

La stratégie choisit de prendre une position longue ou courte en fonction de l'état haussier/baissier du marché, puis fixe un stop-loss et un take-profit après l'entrée en position pour contrôler efficacement le risque. Lorsqu'un signal de retournement apparaît, la position est fermée. L'ensemble du processus de décision combine plusieurs facteurs pour un jugement plus précis.

Analyse des avantages

Cette stratégie présente les avantages suivants :

-

Avantage décisionnel multi-facteurs : par rapport à un seul indicateur, la combinaison de plusieurs indicateurs permet une validation croisée, rendant les résultats plus précis et fiables, réduisant ainsi les coûts de trading inutiles.

-

Conditions strictes pour éviter les erreurs de trading : la stratégie impose des conditions rigoureuses pour les signaux d'achat/vente, nécessitant que plusieurs indicateurs donnent simultanément un signal, ce qui filtre une grande partie du bruit et évite les transactions erronées.

-

Hyperparamètres adaptatifs réduisant l'intervention manuelle : la stratégie intègre la capacité de calculer dynamiquement les paramètres des indicateurs, évitant la subjectivité du choix manuel des hyperparamètres, rendant les paramètres de la stratégie plus scientifiques et objectifs.

-

Mécanisme de stop-loss et take-profit pour contrôler le risque : après ouverture d'une position, la stratégie calcule et trace en temps réel les niveaux de stop-loss et de take-profit, ce qui permet de limiter efficacement les pertes sur une seule transaction et d'éviter un effondrement du compte.

Analyse des risques

Cette stratégie comporte également certains risques à prendre en compte :

-

Probabilité de signaux erronés des indicateurs : bien que la validation multi-indicateurs réduise considérablement le taux de faux signaux, elle ne l'élimine pas complètement. Cela peut entraîner des pertes inutiles.

-

Risque de dépassement du stop-loss : dans des conditions de marché extrêmes, le prix peut chuter brutalement, provoquant un dépassement du stop-loss initialement fixé, entraînant des pertes importantes.

-

Sur-optimisation due à l'optimisation des paramètres : bien que les paramètres dynamiques évitent la subjectivité du choix manuel, ils peuvent aussi conduire à une sur-optimisation des paramètres, réduisant la capacité de généralisation.

Solutions correspondantes :

- Renforcer la rigueur des conditions de filtrage des signaux pour réduire le taux de faux signaux.

- Utiliser une construction de position par fractions pour éviter un stop-loss trop important sur une seule transaction.

- Augmenter la taille de l'échantillon de test et évaluer strictement la stabilité des paramètres.

Pistes d'optimisation de la stratégie

La stratégie de suivi de momentum adaptatif multi-facteurs peut être améliorée selon les axes suivants :

-

Ajouter davantage de facteurs de jugement : intégrer des signaux provenant d'autres types d'indicateurs, comme la volatilité, le volume, etc., pour une décision auxiliaire.

-

Optimiser l'algorithme de stop-loss : introduire des algorithmes de stop-loss plus avancés tels que le stop-loss suiveur (trailing stop) ou le stop-loss par seuil de volatilité, afin de réduire encore la probabilité de dépassement du stop-loss.

-

Introduire des modèles d'apprentissage automatique : utiliser des modèles comme RNN, LSTM pour modéliser les données historiques et assister les décisions d'achat/vente.

-

Assemblage de stratégies : utiliser plusieurs sous-stratégies et les intégrer via des méthodes d'apprentissage ensembliste pour obtenir une performance globale plus stable.

Résumé

La stratégie de suivi de momentum adaptatif multi-facteurs combine plusieurs indicateurs techniques pour identifier les moments d'achat/vente. Par rapport à un seul indicateur, cette stratégie offre un jugement plus précis, tout en intégrant un mécanisme d'adaptation des paramètres et de stop-loss pour contrôler le risque. Les prochaines étapes consisteront à renforcer l'efficacité de la stratégie en introduisant davantage de facteurs auxiliaires, des algorithmes de stop-loss avancés et des méthodes d'apprentissage automatique.

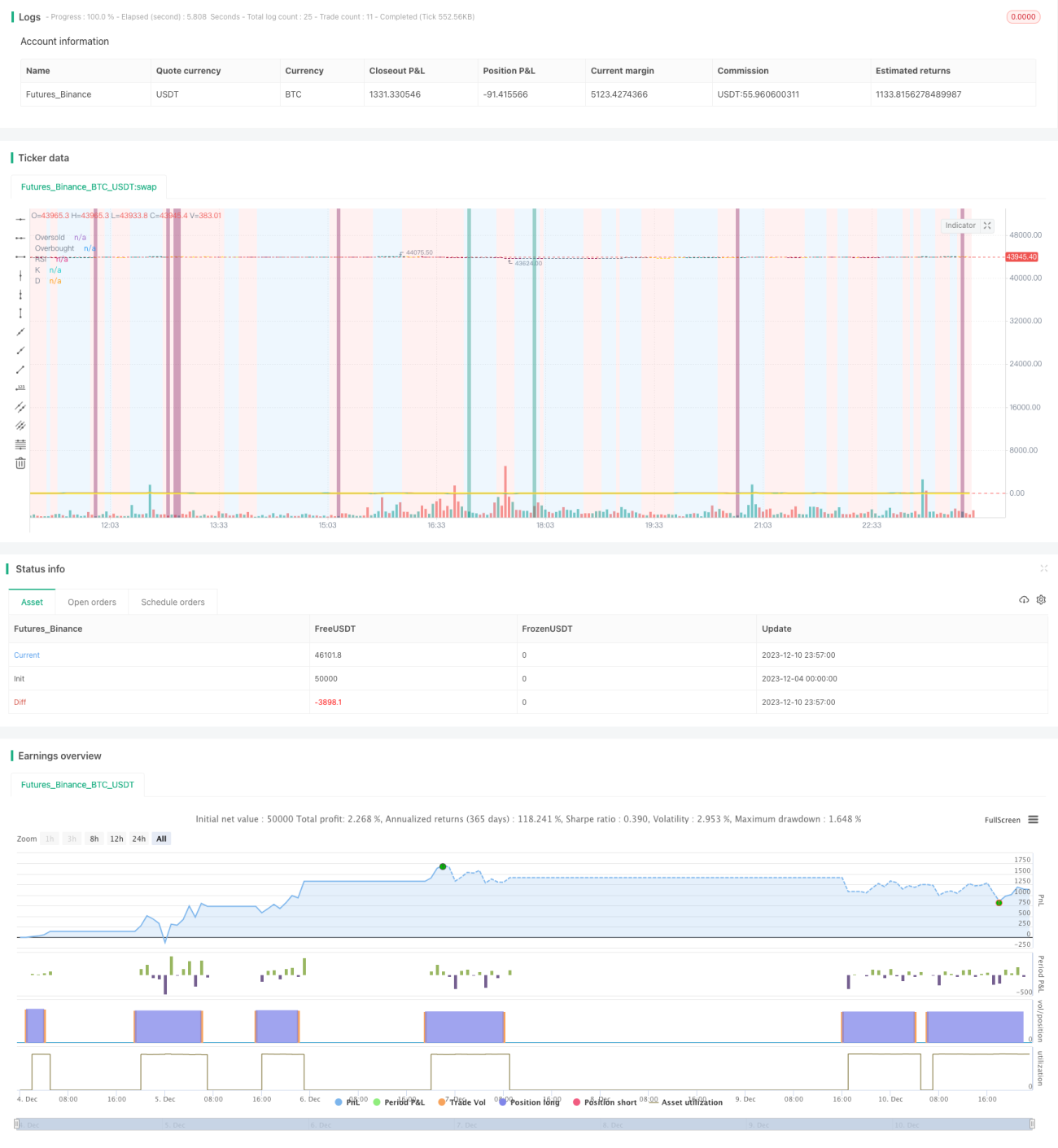

/*backtest

start: 2023-12-04 00:00:00

end: 2023-12-11 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

// ██████╗██████╗ ███████╗ █████╗ ████████╗███████╗██████╗ ██████╗ ██╗ ██╗ - 1