Stratégie quantitative de suivi de tendance basée sur Wave Trend et VWMA

Aperçu

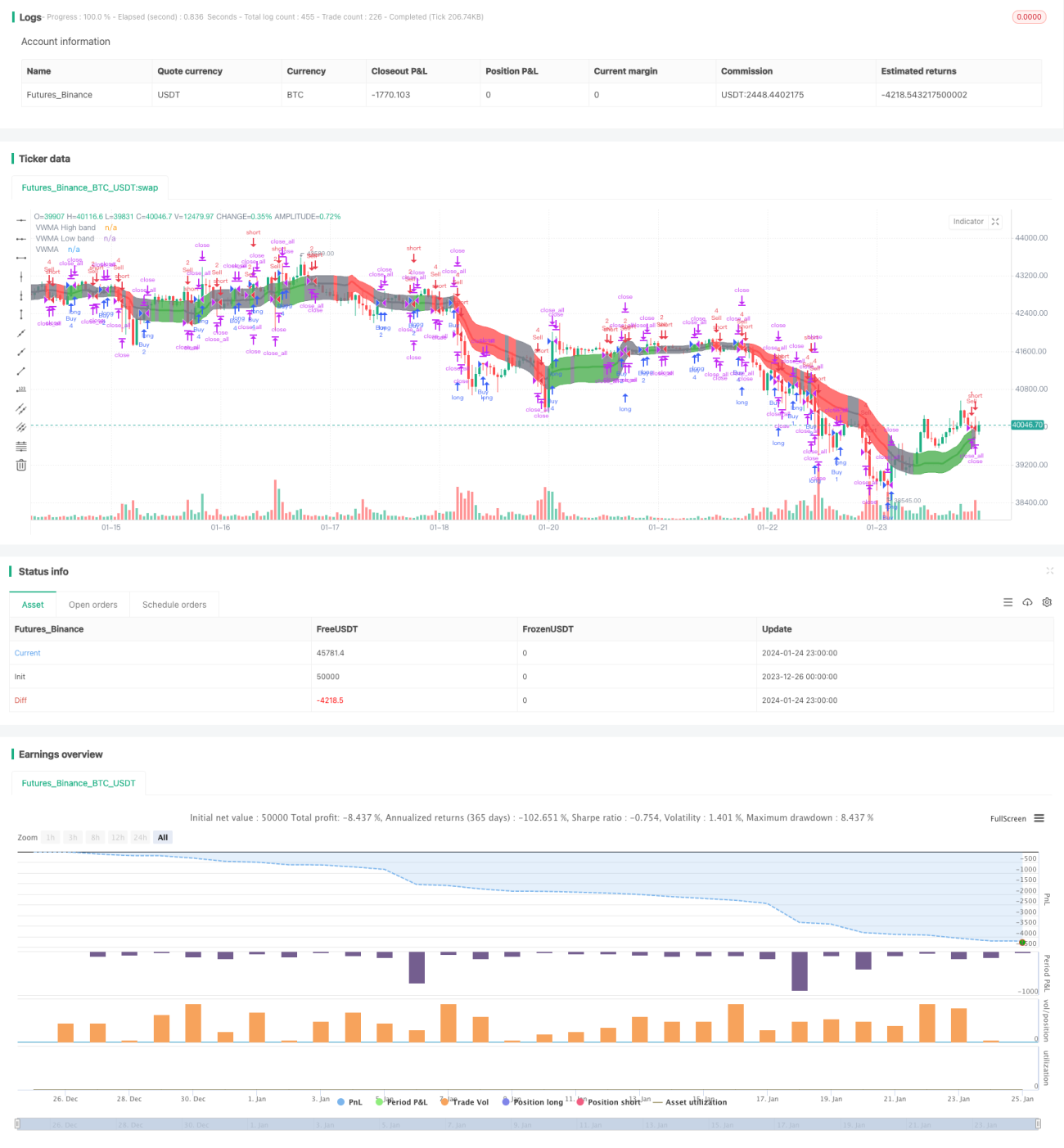

Cette stratégie combine l'oscillateur Wave Trend et l'indicateur VWMA pour mettre en œuvre une stratégie de trading quantitatif de suivi de tendance. Elle permet d'identifier la tendance du marché et de prendre des décisions d'achat ou de vente en fonction des signaux de l'oscillateur Wave Trend. De plus, la taille des transactions est déterminée par les signaux de l'indicateur VWMA.

Principe de la stratégie

La stratégie repose principalement sur deux indicateurs :

-

Oscillateur Wave Trend : Cet indicateur, porté sur TradingView par LazyBear, permet d'identifier les "vagues" des fluctuations de prix et génère des signaux d'achat/vente. Le calcul est le suivant : on calcule d'abord le prix moyen

ap, puis l'EMA deap(appeléesa), ensuite l'EMA de la valeur absolue de la différence entreapetesa(appeléd), et enfin l'indice de cohérenceci = (ap - esa) / (0.015 * d). L'EMA decidonne le Wave Trend (wt1), et la SMA sur 4 périodes dewt1donnewt2. Le croisement haussier dewt1au-dessus dewt2est un signal d'achat, et le croisement baissier en dessous est un signal de vente. -

Indicateur VWMA : Il s'agit d'une moyenne mobile pondérée par le volume. Selon que le prix se situe à l'intérieur ou à l'extérieur des bandes VWMA (bandes haute et basse du VWMA), un signal de +1 (position longue), 0 (neutre) ou -1 (position courte) est généré.

Les moments d'achat et de vente sont déterminés par le signal du Wave Trend. La quantité exacte de chaque transaction est définie en fonction du signal long/court de l'indicateur VWMA.

Avantages de la stratégie

- La combinaison des signaux de deux indicateurs améliore la précision des décisions.

- L'indicateur VWMA, basé sur le volume, permet d'évaluer le rapport de force sur le marché.

- La période de trading peut être personnalisée pour éviter les fortes fluctuations liées aux événements d'actualité importants.

- La taille des transactions est ajustée en fonction du signal VWMA, ce qui réduit le risque de trading.

Risques de la stratégie

- L'indicateur Wave Trend peut générer de faux signaux.

- Des données de volume imprécises peuvent affecter l'indicateur VWMA.

- Un historique de données long est nécessaire pour le calcul des indicateurs.

- Aucune stratégie de stop-loss n'est intégrée.

Pistes d'optimisation

- Tester différentes combinaisons de paramètres pour trouver les valeurs optimales.

- Ajouter une stratégie de stop-loss.

- Envisager de combiner d'autres indicateurs pour filtrer les signaux.

- Tester différents réglages de période de trading.

- Ajuster dynamiquement le mode de calcul de la taille des transactions.

Résumé

Cette stratégie intègre des indicateurs de tendance et de volume pour former une stratégie de suivi de tendance relativement avancée. Elle présente certains avantages, mais comporte également des risques à ne pas négliger. L'optimisation des paramètres et des règles pourrait améliorer davantage sa stabilité et son rendement.

- 1