Stratégie de trading de suivi de chandeliers en grille bidirectionnelle

Aperçu

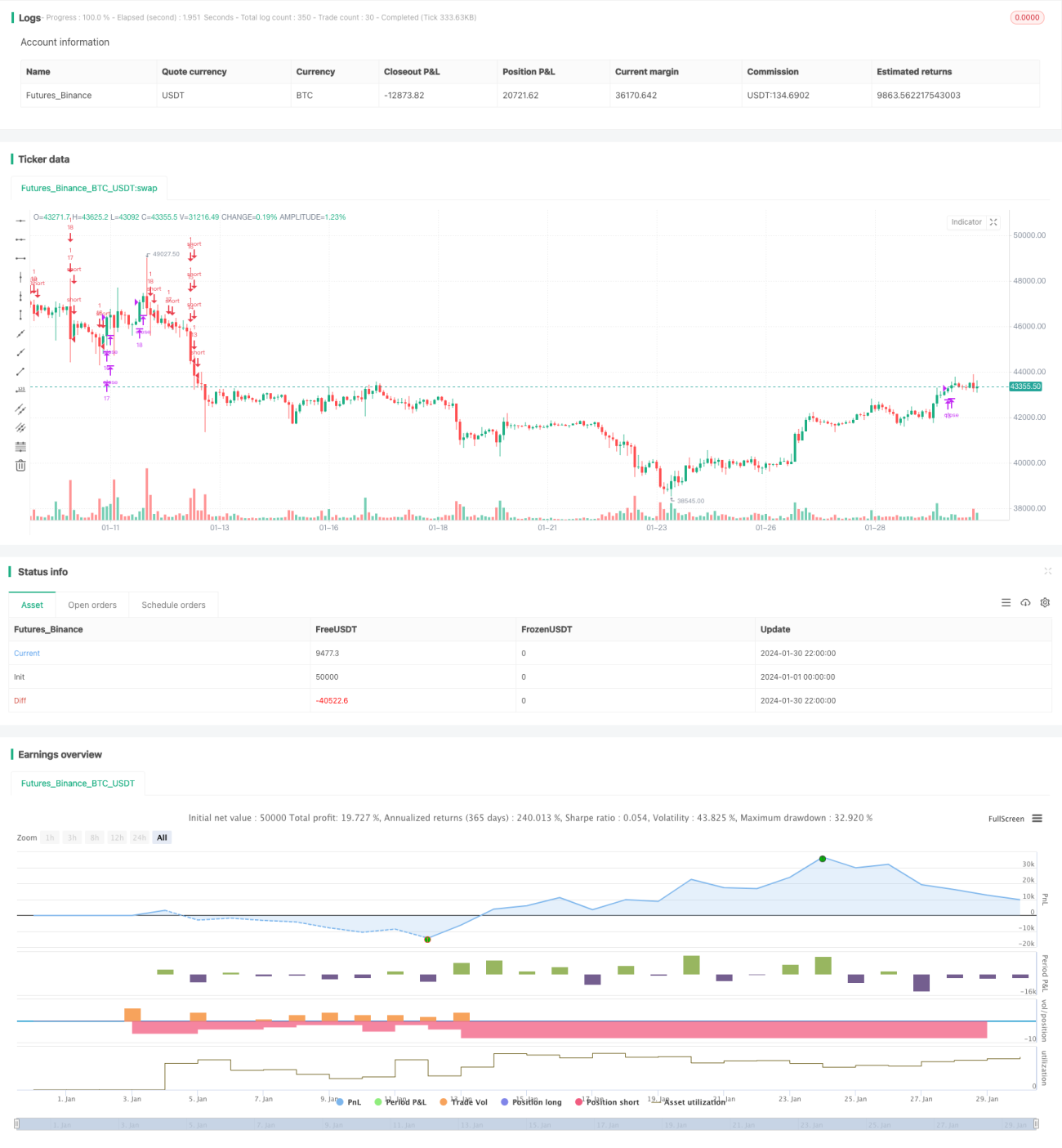

Cette stratégie est une stratégie de trading en grille bidirectionnelle basée sur les variations en temps réel des bougies. Elle permet d'obtenir des bénéfices stables aussi bien en marché haussier qu'en marché baissier.

Principe de la stratégie

-

En fonction du nombre de grilles défini par l'utilisateur, elle calcule automatiquement la plage de prix de la grille et chaque prix de grille.

-

Lorsque le prix franchit un prix de grille, une position longue est ouverte avec une quantité fixe ; lorsque le prix tombe en dessous d'un prix de grille, la position longue est fermée et une position courte est ouverte.

-

Ainsi, lorsque le prix oscille dans l'intervalle de la grille, il est possible de réaliser des bénéfices en suivant les variations de prix.

Analyse des avantages

-

Calcul automatique d'une plage de grille raisonnable, sans nécessité de déterminer manuellement les supports et résistances.

-

Trading bidirectionnel, adaptable aux conditions de marché changeantes.

-

Quantité d'ouverture fixe, favorable au contrôle des risques.

-

Code intuitif et concis, facile à comprendre et à modifier.

Analyse des risques

-

Des fluctuations violentes du marché peuvent entraîner une amplification des pertes.

-

L'accumulation des frais de transaction affecte également le bénéfice final.

-

Il est nécessaire de déterminer raisonnablement le nombre de grilles ; trop de grilles augmentent le nombre de transactions mais chaque profit est limité.

Pistes d'optimisation

-

Ajouter une stratégie de stop loss pour éviter l'aggravation des pertes.

-

Ajouter une fonction d'ajustement dynamique du nombre de grilles.

-

Envisager d'ajouter un effet de levier pour amplifier les volumes de transactions.

Conclusion

L'idée générale de cette stratégie est claire et concise, permettant d'obtenir des revenus stables grâce au trading en grille bidirectionnelle, tout en présentant certains risques de trading. Grâce à une optimisation continue, elle pourrait donner de meilleurs résultats.

- 1