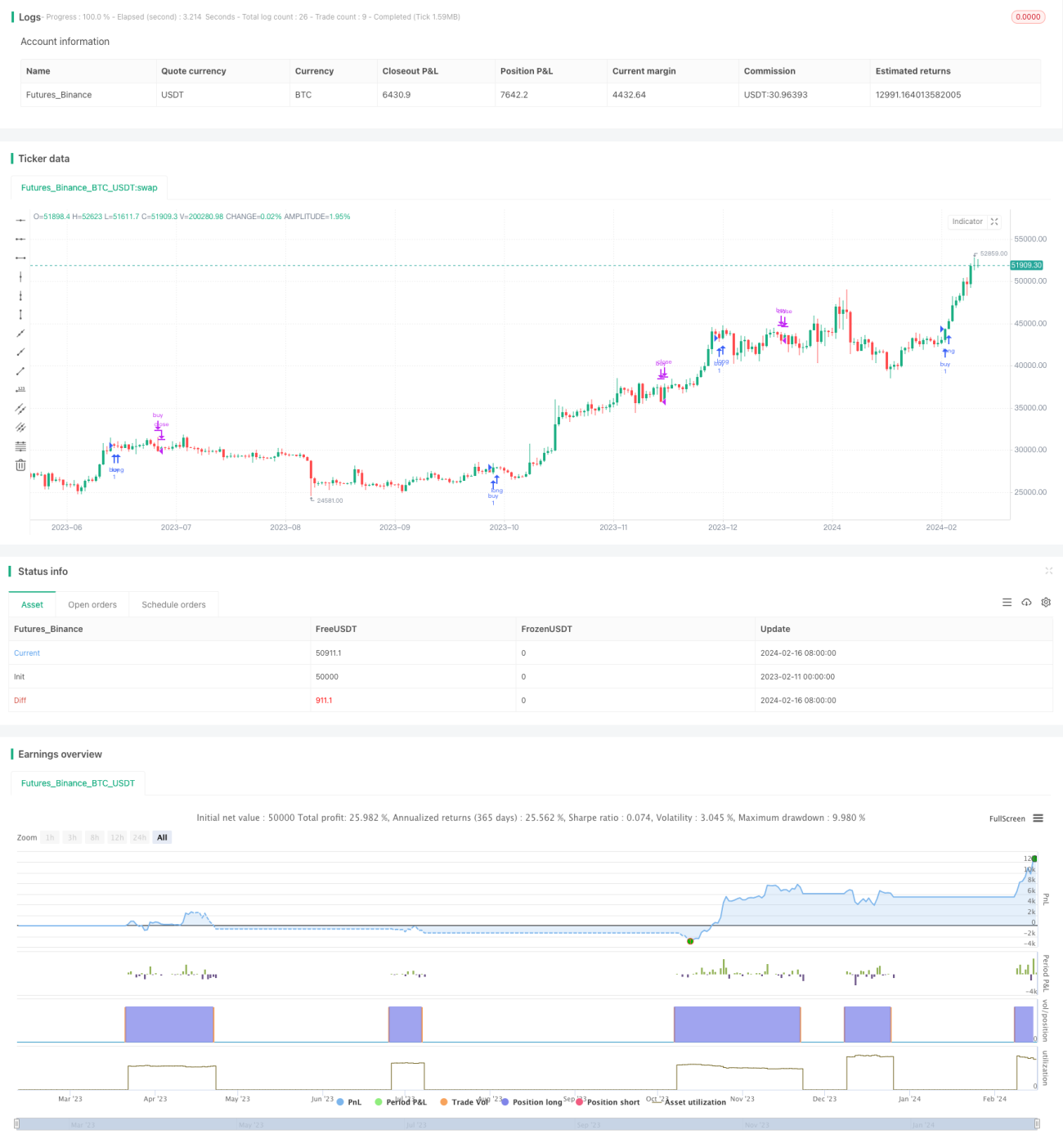

Stratégie de trading basée sur l'indice de force relative (RSI) et l'indice de force relative stochastique (Stochastic RSI)

Aperçu

Cette stratégie de trading combine l'utilisation de deux indicateurs techniques, le Relative Strength Index (RSI) et le Stochastic RSI, pour générer des signaux de trading. La stratégie exploite en outre l'évolution des prix des crypto-monnaies sur une période plus élevée pour confirmer la tendance, afin d'améliorer la fiabilité des signaux.

Nom de la stratégie

Stratégie de trading RSI-SRSI multi-timeframes (Multi Timeframe RSI-SRSI Trading Strategy)

Principe de la stratégie

Cette stratégie détermine les conditions de surachat et de survente en fonction des valeurs de l'indicateur RSI. Lorsque le RSI est inférieur à 30, c'est un signal de survente ; lorsqu'il est supérieur à 70, c'est un signal de surachat. L'indicateur Stochastic RSI observe quant à lui la volatilité du RSI lui-même. Un Stochastic RSI inférieur à 5 est un signal de survente, tandis qu'un Stochastic RSI supérieur à 50 est un signal de surachat.

La stratégie intègre également l'évolution des prix des crypto-monnaies sur une période plus élevée (par exemple, hebdomadaire). Un signal d'achat n'est généré que lorsque le RSI de la période plus élevée dépasse un seuil (par exemple, 45). Ce réglage permet de filtrer les signaux de survente non persistants qui apparaissent lorsque la tendance globale est baissière.

Les signaux d'achat et de vente nécessitent une confirmation sur une certaine période (par exemple, 8 bougies) après leur déclenchement, afin d'éviter les signaux trompeurs.

Avantages de la stratégie

- Méthode classique d'analyse technique utilisant le RSI pour identifier les conditions de surachat et de survente

- Combinaison avec le Stochastic RSI pour détecter les retournements du RSI lui-même

- Utilisation de l'analyse multi-timeframes pour filtrer les signaux trompeurs et améliorer la qualité des signaux

Risques de la stratégie et solutions

- Le RSI peut générer de faux signaux

- Combinaison avec d'autres indicateurs pour filtrer les signaux trompeurs

- Application de techniques de confirmation de tendance

- Des seuils mal paramétrés peuvent générer trop de signaux

- Optimisation des combinaisons de paramètres pour trouver les meilleurs réglages

- Les signaux d'achat/vente nécessitent un délai de confirmation

- Trouver un équilibre dans la période de confirmation pour filtrer les signaux trompeurs sans manquer les opportunités

Pistes d'optimisation

- Tester davantage de combinaisons d'indicateurs pour obtenir des signaux plus robustes

- Par exemple, ajouter l'indicateur MACD à la stratégie

- Utiliser des méthodes d'apprentissage automatique pour trouver les paramètres optimaux

- Employez des algorithmes génétiques/évolutifs pour une optimisation automatique

- Ajouter une stratégie de stop-loss pour contrôler le risque par transaction

- Stop-loss lorsque le prix casse un support

Conclusion

Cette stratégie repose principalement sur deux indicateurs classiques, le RSI et le Stochastic RSI, pour générer des signaux de trading. L'introduction d'une période plus élevée pour confirmer la tendance permet de filtrer efficacement les signaux trompeurs et d'améliorer la qualité des signaux. L'optimisation des paramètres et l'ajout d'une stratégie de stop-loss peuvent encore renforcer les performances de la stratégie. L'approche est simple, directe, facile à comprendre et à mettre en œuvre, ce qui en fait un excellent point de départ pour le trading quantitatif.

- 1