धैर्यपूर्वक ट्रेंड फॉलोइंग रणनीति पर नज़र रखें

सिंहावलोकन

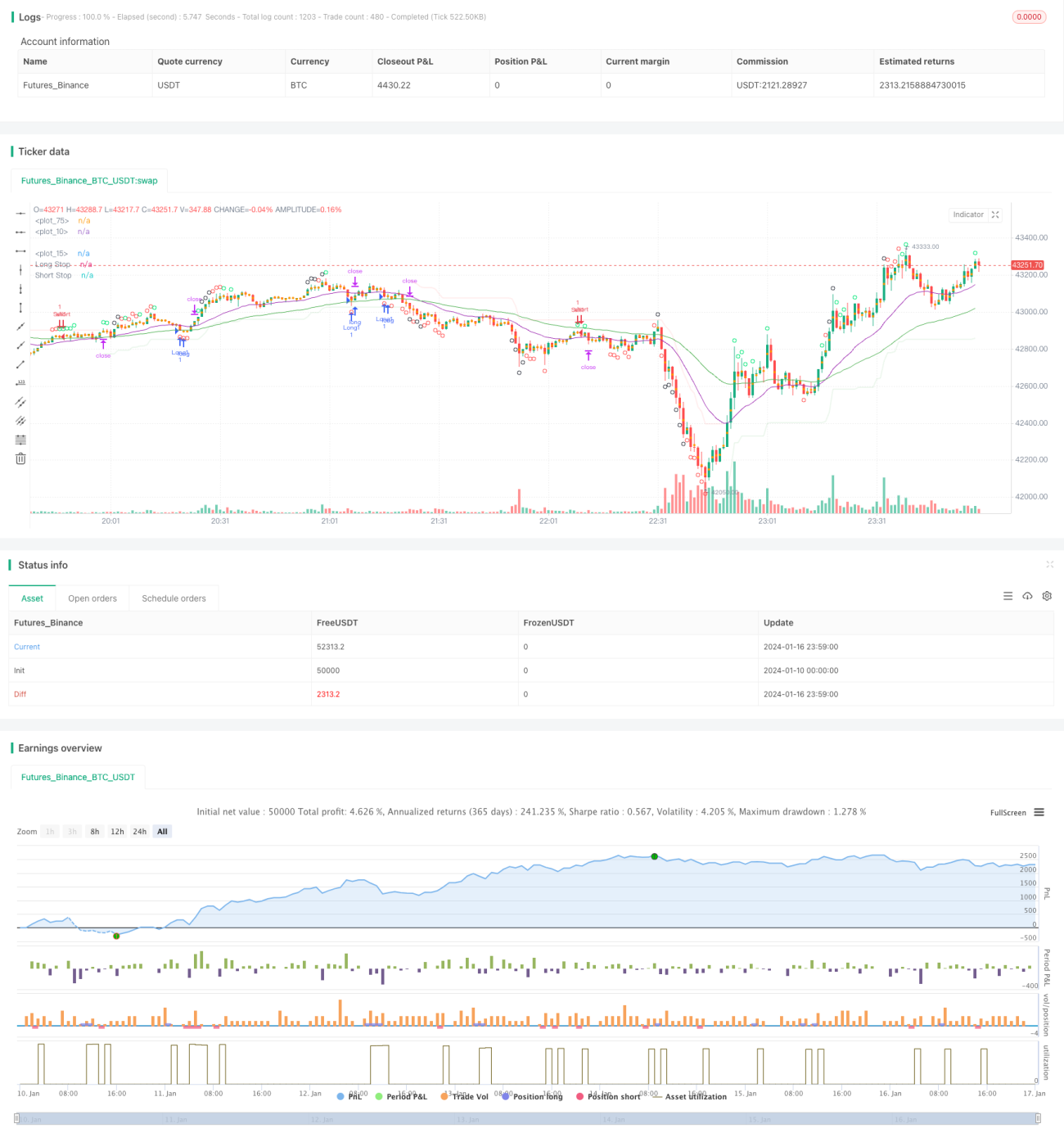

धैर्यपूर्वक प्रवृत्ति का अनुसरण करने वाली यह रणनीति एक प्रवृत्ति-अनुवर्ती रणनीति है। यह चलती औसत संकेतकों के संयोजन का उपयोग करके प्रवृत्ति की दिशा निर्धारित करती है, और अधिक-खरीद/अधिक-बिक्री संकेतक CCI के साथ मिलकर ट्रेडिंग सिग्नल उत्पन्न करती है। यह रणनीति बड़ी प्रवृत्ति का पीछा करती है और साइडवेज़ बाजार में फंसने से प्रभावी रूप से बच सकती है।

रणनीति का सिद्धांत

यह रणनीति प्रवृत्ति की दिशा निर्धारित करने के लिए 21-अवधि और 55-अवधि के EMA के संयोजन का उपयोग करती है। जब अल्पकालिक EMA दीर्घकालिक EMA से ऊपर होता है, तो इसे अपट्रेंड के रूप में परिभाषित किया जाता है, और जब अल्पकालिक EMA दीर्घकालिक EMA से नीचे होता है, तो इसे डाउनट्रेंड के रूप में परिभाषित किया जाता है।

CCI संकेतक का उपयोग अधिक-खरीद/अधिक-बिक्री की स्थिति का निर्धारण करने के लिए किया जाता है। CCI का -100 रेखा से ऊपर जाना तल पर अधिक-बिक्री का संकेत है, और 100 रेखा से नीचे जाना शीर्ष पर अधिक-खरीद का संकेत है। CCI संकेतक की विभिन्न अधिक-खरीद/अधिक-बिक्री रेखाओं के आधार पर, रणनीति तीन ट्रेडिंग सिग्नल तीव्रता स्तरों में विभाजित होती है।

जब अपट्रेंड की पुष्टि होती है और CCI संकेतक एक मजबूत तल अधिक-बिक्री संकेत देता है, तो लॉन्ग एंट्री की जाती है। जब डाउनट्रेंड की पुष्टि होती है और CCI संकेतक एक मजबूत शीर्ष अधिक-खरीद संकेत देता है, तो शॉर्ट एंट्री की जाती है।

स्टॉप-लॉस रेखा SuperTrend संकेतक पर आधारित होती है, और लक्ष्य लाभ निश्चित अंकों पर सेट किया जाता है।

लाभ विश्लेषण

इस रणनीति के मुख्य लाभ इस प्रकार हैं:

- बड़ी प्रवृत्ति का पीछा करती है, फंसने से बचाती है

- CCI संकेतक प्रभावी रूप से रिवर्सल पॉइंट का निर्धारण कर सकता है

- SuperTrend स्टॉप-लॉस रेखा उचित रूप से सेट की गई है

- निश्चित स्टॉप-लॉस और निश्चित टेक-प्रॉफिट, जोखिम नियंत्रणीय है

जोखिम विश्लेषण

इस रणनीति में मुख्य रूप से निम्नलिखित जोखिम हैं:

- बड़ी प्रवृत्ति के निर्धारण में त्रुटि की संभावना

- CCI संकेतक द्वारा झूठे संकेत देने की संभावना

- स्टॉप-लॉस पॉइंट बहुत छोटा या बहुत बड़ा होने से अनावश्यक स्टॉप-लॉस की संभावना

- निश्चित टेक-प्रॉफिट के कारण प्रवृत्ति के साथ लगातार लाभ न उठा पाने की संभावना

इन जोखिमों के लिए, हम EMA अवधि पैरामीटर, CCI पैरामीटर और स्टॉप-लॉस/टेक-प्रॉफिट पॉइंट को समायोजित करके अनुकूलन कर सकते हैं। साथ ही, रणनीति सिग्नल सत्यापन के लिए अधिक संकेतक शामिल करना भी आवश्यक है।

अनुकूलन दिशाएँ

इस रणनीति के अनुकूलन की मुख्य दिशाएँ हैं:

-

बेहतर प्रवृत्ति निर्धारण और सिग्नल सत्यापन संकेतक खोजने के लिए अधिक संकेतकों के संयोजन का परीक्षण करना।

-

प्रवृत्ति को बेहतर ढंग से ट्रैक करने और जोखिम नियंत्रण के लिए ATR आधारित डायनेमिक स्टॉप-लॉस/टेक-प्रॉफिट का उपयोग करना।

-

प्रवृत्ति संभावना का निर्धारण करने के लिए ऐतिहासिक डेटा पर प्रशिक्षित मशीन लर्निंग मॉडल शामिल करना।

-

विभिन्न उपकरणों के लिए पैरामीटर समायोजन और अनुकूलन करना।

सारांश

धैर्यपूर्वक प्रवृत्ति का अनुसरण करने वाली रणनीति समग्र रूप से एक बहुत ही व्यावहारिक प्रवृत्ति-अनुवर्ती रणनीति है। यह बड़ी प्रवृत्ति की दिशा निर्धारित करने के लिए चलती औसत का उपयोग करती है, CCI संकेतक के साथ रिवर्सल पॉइंट सिग्नल खोजती है, और SuperTrend स्टॉप-लॉस रेखा उचित रूप से सेट करती है। पैरामीटर समायोजन और बहु-संकेतक संयोजन सत्यापन के माध्यम से, इस रणनीति को और अधिक अनुकूलित किया जा सकता है, और यह दीर्घकालिक वास्तविक ट्रेडिंग ट्रैकिंग और सत्यापन के योग्य है।

- 1