एक रणनीति जो विभिन्न तकनीकी संकेतकों का उपयोग करके मात्रात्मक व्यापार करती है

अवलोकन

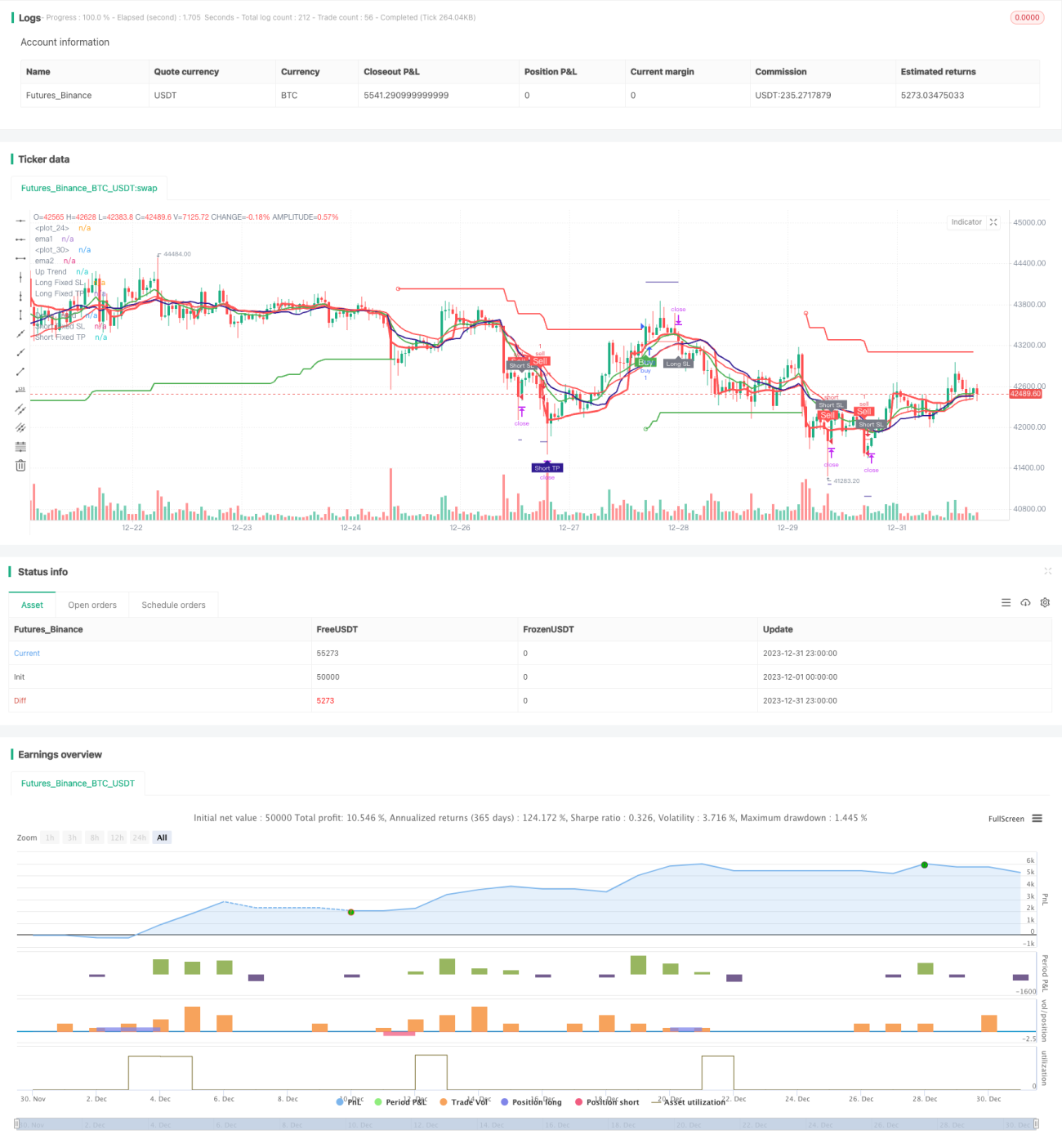

यह रणनीति एक मात्रात्मक व्यापार रणनीति है जो विभिन्न तकनीकी संकेतकों का उपयोग करती है। मुख्य रूप से EMA मूविंग एवरेज क्रॉसओवर, SuperTrend संकेतक, RSI संकेतक, MACD संकेतक आदि का संयोजन करके व्यापार संकेत उत्पन्न किए जाते हैं।

रणनीति का सिद्धांत

इस रणनीति का मुख्य व्यापार तर्क निम्नलिखित पहलुओं पर आधारित है:

-

EMA मूविंग एवरेज क्रॉसओवर: तेज़ EMA1 और धीमी EMA2 की गणना करें। जब तेज़ रेखा धीमी रेखा को ऊपर से पार करती है तो खरीद संकेत उत्पन्न होता है, और जब तेज़ रेखा धीमी रेखा को नीचे से पार करती है तो बिक्री संकेत उत्पन्न होता है।

-

VWMA मूविंग एवरेज: VWMA मूविंग एवरेज की गणना करें। जब बंद मूल्य इस मूविंग एवरेज को ऊपर से पार करता है तो इसे खरीद संकेत माना जाता है, और जब नीचे से पार करता है तो बिक्री संकेत माना जाता है।

-

SuperTrend संकेतक: ATR और multiplier मापदंडों के अनुसार SuperTrend के ऊपरी और निचले बैंड की गणना करें और प्रवृत्ति दिशा निर्धारित करें। ऊपर की प्रवृत्ति में खरीद संकेत और नीचे की प्रवृत्ति में बिक्री संकेत उत्पन्न होता है।

-

RSI संकेतक: RSI संकेतक की गणना करें। जब RSI अधिक खरीद रेखा से ऊपर होता है तो बिक्री संकेत माना जाता है, और जब RSI अधिक बिक्री क्षेत्र से नीचे होता है तो खरीद संकेत माना जाता है।

-

MACD संकेतक: MACD की तेज़ रेखा, धीमी रेखा और संकेत रेखा की गणना करें। जब तेज़ रेखा संकेत रेखा को ऊपर से पार करती है तो खरीद संकेत उत्पन्न होता है, और जब नीचे से पार करती है तो बिक्री संकेत उत्पन्न होता है।

उपरोक्त कई संकेतकों से व्यापार संकेत प्राप्त करने के बाद, रणनीति "AND" तर्क का उपयोग करके निर्णय लेती है, अर्थात जब कई संकेतक एक साथ संकेत देते हैं तभी अंतिम खरीद और बिक्री संकेत उत्पन्न होते हैं।

रणनीति के लाभ

यह रणनीति बाजार का मूल्यांकन करने के लिए कई संकेतकों को जोड़ती है, जो झूठे संकेतों को प्रभावी ढंग से कम कर सकती है। मुख्य लाभ इस प्रकार हैं:

-

विभिन्न संकेतकों का उपयोग करके मिश्रित फ़िल्टरिंग, जो एकल संकेतक के कारण होने वाले गलत संकेतों को कम कर सकती है।

-

प्रवृत्ति संकेतकों और ऑसिलेटर संकेतकों का संयोजन, जो प्रवृत्ति बाजार में अतिरिक्त लाभ प्राप्त करने में मदद करता है।

-

मजबूत स्टॉप-लॉस तर्क, जो एकल लेन-देन के अधिकतम नुकसान को प्रभावी ढंग से नियंत्रित कर सकता है।

-

मार्टिनगेल (गुणक) तर्क, जो नुकसान के बाद अतिरिक्त ऑर्डर जोड़कर बराबर होने का अवसर प्रदान करता है।

रणनीति के जोखिम

इस रणनीति में मुख्य रूप से निम्नलिखित जोखिम हैं:

-

कई संकेतकों का संयोजन अत्यधिक रूढ़िवादी हो सकता है, जिससे कुछ व्यापार अवसर छूट सकते हैं। संकेतकों के संयोजन को उचित रूप से सरल बनाया जा सकता है।

-

मार्टिनगेल (गुणक) अतिरिक्त ऑर्डर तर्क से नुकसान बढ़ सकता है। ऑर्डर जोड़ने की संख्या पर उचित सीमा निर्धारित की जानी चाहिए।

-

स्टॉप-लॉस के गलत स्थान से अनावश्यक स्टॉप-लॉस हो सकता है। अनुकूली स्टॉप-लॉस स्थान निर्धारित किया जाना चाहिए।

-

मापदंडों का गलत सेटिंग बहुत अधिक गलत संकेत उत्पन्न कर सकता है। सर्वोत्तम पैरामीटर संयोजन प्राप्त करने के लिए उन्हें अनुकूलित किया जाना चाहिए।

रणनीति अनुकूलन की दिशा

इस रणनीति को निम्नलिखित पहलुओं से और अधिक अनुकूलित किया जा सकता है:

-

विभिन्न मापदंडों के संयोजन वाले संकेतकों के प्रभाव का मूल्यांकन करें और उनके भार का चयन करें।

-

विभिन्न संकेतक मापदंडों के सेटिंग का परीक्षण करें।

-

अनुकूली स्टॉप-लॉस तर्क जोड़ें।

-

गतिशील पोजीशन प्रबंधन तंत्र शामिल करें।

-

मशीन लर्निंग विधियों का उपयोग करके मापदंडों और मॉडल को अनुकूलित करें।

निष्कर्ष

यह रणनीति कुल मिलाकर एक बहुत ही व्यावहारिक मात्रात्मक व्यापार रणनीति है। यह कई क्लासिक तकनीकी संकेतकों की शक्तियों को जोड़ती है, और बाजार का प्रभावी ढंग से मूल्यांकन कर सकती है। मापदंड अनुकूलन और मॉडल पुनरावृत्ति के माध्यम से, यह रणनीति बेहतर व्यापार परिणाम प्राप्त कर सकती है।

- 1