बहु-अवधि SMA संकेतक पर आधारित प्रवृत्ति अनुसरण रणनीति

अवलोकन

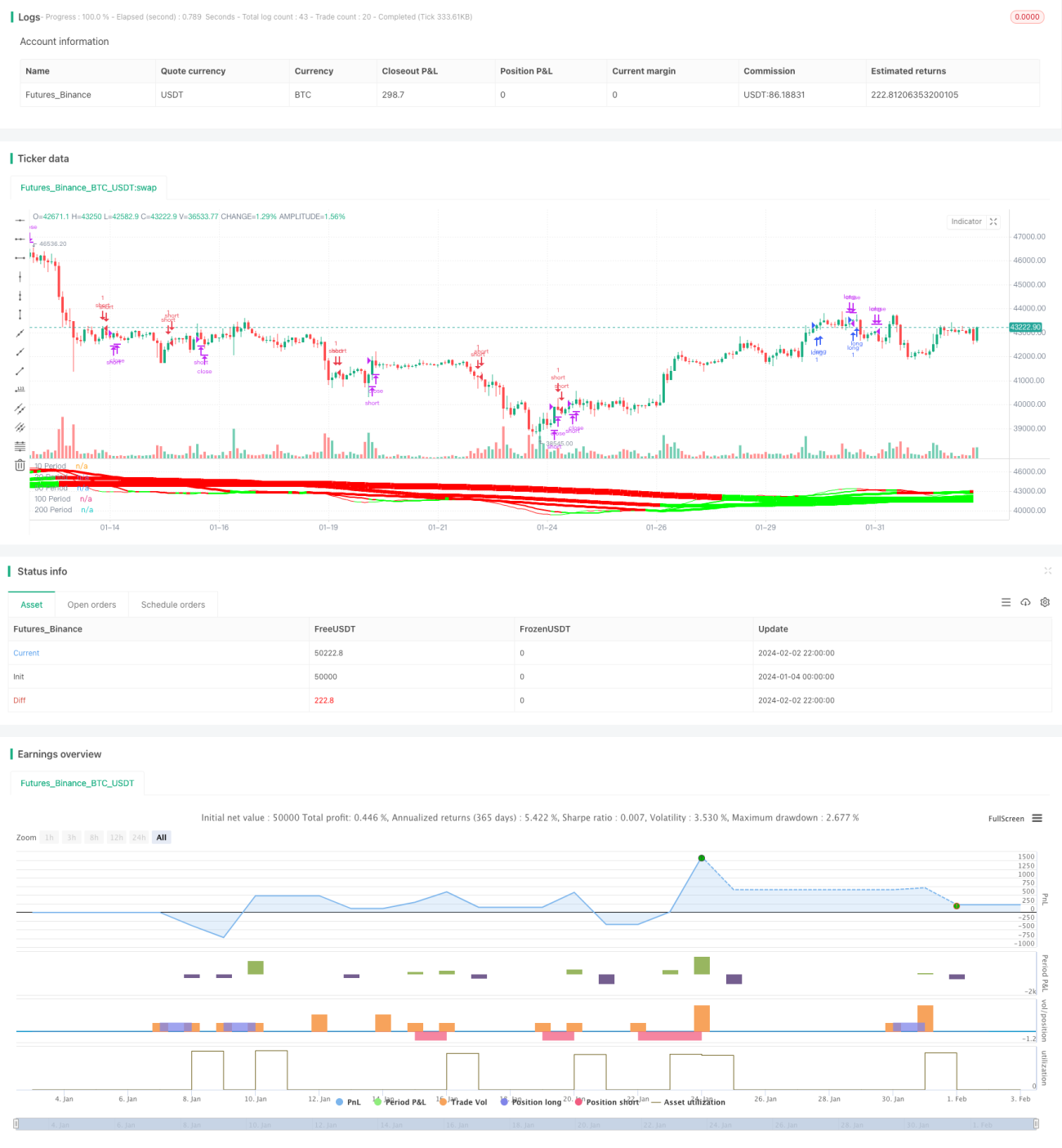

यह रणनीति विभिन्न अवधियों के कई SMA मूविंग एवरेज को संयोजित करके प्रवृत्ति का आकलन और अनुसरण करती है। मुख्य विचार यह है: विभिन्न अवधियों के SMA के ऊपर और नीचे की दिशाओं की तुलना करके प्रवृत्ति का निर्धारण करना; जब छोटी अवधि का SMA लंबी अवधि के SMA को ऊपर से क्रॉस करता है, तो लॉन्ग (खरीदारी) करें; जब छोटी अवधि का SMA लंबी अवधि के SMA को नीचे से क्रॉस करता है, तो शॉर्ट (बिक्री) करें। साथ ही, प्रवेश और निकास की पुष्टि के लिए ZeroLagEMA इंडिकेटर का उपयोग किया जाता है।

रणनीति का सिद्धांत

- विभिन्न अवधियों के 5 SMA मूविंग एवरेज का उपयोग किया जाता है, जो क्रमशः 10-अवधि, 20-अवधि, 50-अवधि, 100-अवधि और 200-अवधि हैं।

- इन 5 रेखाओं के बढ़ने और घटने की दिशाओं की तुलना करके प्रवृत्ति की दिशा निर्धारित की जाती है। उदाहरण के लिए, जब 10-अवधि, 20-अवधि, 100-अवधि और 200-अवधि SMA सभी एक साथ बढ़ रहे हों, तो इसे ऊपरी प्रवृत्ति माना जाता है; जब सभी एक साथ गिर रहे हों, तो इसे नीचे की प्रवृत्ति माना जाता है।

- विभिन्न अवधियों के SMA के मानों की तुलना करके ट्रेडिंग सिग्नल उत्पन्न किए जाते हैं। उदाहरण के लिए, जब 10-अवधि SMA 20-अवधि SMA को ऊपर से क्रॉस करता है, तो लॉन्ग करने का प्रवेश सिग्नल मिलता है; जब 10-अवधि SMA 20-अवधि SMA को नीचे से क्रॉस करता है, तो शॉर्ट करने का प्रवेश सिग्नल मिलता है।

- प्रवेश की पुष्टि और निकास सिग्नल के लिए ZeroLagEMA का उपयोग किया जाता है। जब तेज़ अवधि का ZeroLagEMA धीमी अवधि को ऊपर से क्रॉस करता है, तो लॉन्ग करें; नीचे से क्रॉस करने पर लॉन्ग पोजीशन बंद करें। शॉर्ट सिग्नल के लिए इसके विपरीत तरीका अपनाया जाता है।

रणनीति के लाभ

- विभिन्न अवधियों के कई SMA मूविंग एवरेज के संयोजन का उपयोग करके बाजार की प्रवृत्ति की दिशा का प्रभावी ढंग से आकलन किया जा सकता है।

- अवधि के SMA मानों की तुलना से ट्रेडिंग सिग्नल उत्पन्न होते हैं, जो मात्रात्मक प्रवेश और निकास नियम बनाते हैं।

- ZeroLagEMA फ़िल्टर अनावश्यक ट्रेडों से बचने में मदद करता है, जिससे रणनीति की स्थिरता बढ़ती है।

- प्रवृत्ति निर्धारण और ट्रेडिंग सिग्नलों को मिलाकर ट्रेंड फॉलोइंग ट्रेडिंग प्राप्त की गई है।

रणनीति के जोखिम और समाधान

- जब बाजार साइडवे या कंसोलिडेशन चरण में प्रवेश करता है, तो SMA सिग्नल बार-बार क्रॉसओवर दे सकते हैं, जिससे कई अप्रभावी ट्रेड और नुकसान का जोखिम होता है।

- समाधान: अप्रभावी सिग्नलों के प्रवेश से बचने के लिए ZeroLagEMA के फ़िल्टरिंग पैरामीटर बढ़ाएँ।

- चूंकि कई अवधियों के SMA पर निर्भरता है, सिग्नलों में कुछ देरी होती है, जिससे अल्पकालिक तीव्र मूल्य परिवर्तनों पर तुरंत प्रतिक्रिया नहीं दी जा सकती।

- समाधान: MACD जैसे अधिक संवेदनशील संकेतकों को शामिल करके सहायता लें।

रणनीति अनुकूलन की दिशाएँ

- SMA अवधि मापदंडों को अनुकूलित करके सर्वोत्तम पैरामीटर संयोजन खोजें।

- स्टॉप-लॉस रणनीति जोड़ें, जैसे ट्रेलिंग स्टॉप, ताकि प्रति ट्रेड हानि को और नियंत्रित किया जा सके।

- पोजीशन साइज़ प्रबंधन तंत्र जोड़ें, जिससे मजबूत प्रवृत्ति के दौरान पोजीशन बढ़ाई जा सके और साइडवे बाजार में पोजीशन घटाई जा सके।

- MACD, KDJ जैसे अधिक सहायक संकेतकों को शामिल करके समग्र रणनीति स्थिरता में सुधार करें।

सारांश

यह रणनीति कई अवधियों के SMA मूविंग एवरेज को संयोजित करके बाजार की प्रवृत्ति की दिशा का प्रभावी आकलन करती है और मात्रात्मक ट्रेडिंग सिग्नल उत्पन्न करती है। साथ ही, ZeroLagEMA के उपयोग से रणनीति की सफलता दर में वृद्धि हुई है। कुल मिलाकर, यह रणनीति ट्रेंड फॉलोइंग पर आधारित मात्रात्मक ट्रेडिंग दृष्टिकोण को लागू करती है और उल्लेखनीय परिणाम दिखाती है। SMA अवधि मापदंडों, स्टॉप-लॉस रणनीति और पोजीशन प्रबंधन के और अनुकूलन से रणनीति के प्रभाव को और बढ़ाया जा सकता है, जो वास्तविक ट्रेडिंग में सत्यापन और उपयोग के योग्य है।

/*backtest

start: 2024-01-04 00:00:00

end: 2024-02-03 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Forex MA Racer - SMA Performance /w ZeroLag EMA Trigger", shorttitle = "FX MA Racer (5x SMA, 2x zlEMA)", overlay=false )

// === INPUTS ===- 1