गतिशील ढलान प्रवृत्ति रेखा व्यापार रणनीति

सिंहावलोकन

इस रणनीति का मुख्य विचार मूल्य प्रवृत्ति की दिशा निर्धारित करने के लिए गतिशील ढलान का उपयोग करना है, और ट्रेडिंग सिग्नल उत्पन्न करने के लिए ब्रेकआउट निर्णय के साथ इसे जोड़ना है। विशेष रूप से, यह वास्तविक समय में मूल्य के नए उच्च और नए निम्न बिंदुओं को ट्रैक करता है, विभिन्न समय अंतरालों में मूल्य परिवर्तन के आधार पर गतिशील ढलान की गणना करता है, और फिर मूल्य द्वारा ट्रेंड लाइनों के ब्रेकआउट के साथ इसे जोड़कर लॉन्ग/शॉर्ट सिग्नल निर्धारित करता है।

रणनीति का सिद्धांत

यह रणनीति मुख्य रूप से निम्नलिखित चरणों में विभाजित है:

-

उच्चतम मूल्य और निम्नतम मूल्य का निर्धारण: एक निश्चित अवधि (जैसे 20 कैंडलस्टिक) के भीतर उच्चतम और निम्नतम मूल्य को ट्रैक करें, और यह निर्धारित करें कि क्या यह नया उच्च या नया निम्न है।

-

गतिशील ढलान की गणना: नए उच्च या नए निम्न बनाने वाली कैंडलस्टिक की संख्या रिकॉर्ड करें, और नए उच्च/निम्न बिंदु से एक निश्चित अवधि (जैसे 9 कैंडलस्टिक) के बाद उच्च/निम्न बिंदु तक गतिशील ढलान की गणना करें।

-

ट्रेंड लाइनें खींचना: गतिशील ढलान के आधार पर, ऊपर की ओर और नीचे की ओर की ट्रेंड लाइनें खींचें।

-

ट्रेंड लाइनों का विस्तार और अद्यतन: जब मूल्य ट्रेंड लाइन को तोड़ता है, तो ट्रेंड लाइनों का विस्तार और अद्यतन किया जाता है।

-

ट्रेडिंग सिग्नल: मूल्य द्वारा ट्रेंड लाइनों के ब्रेकआउट के साथ, लॉन्ग और शॉर्ट सिग्नल निर्धारित किए जाते हैं।

रणनीति के लाभ

इस रणनीति के निम्नलिखित लाभ हैं:

-

प्रवृत्ति की दिशा का गतिशील रूप से निर्धारण, बाजार परिवर्तनों के लिए लचीला अनुकूलन।

-

स्टॉप लॉस का उचित नियंत्रण, कम ड्रॉडाउन।

-

स्पष्ट ब्रेकआउट ट्रेडिंग सिग्नल, सरल कार्यान्वयन।

-

अनुकूलन योग्य पैरामीटर, उच्च अनुकूलन क्षमता।

-

स्पष्ट कोड संरचना, समझने और पुनर्विकास में आसान।

जोखिम और समाधान

इस रणनीति में कुछ जोखिम भी हैं:

-

प्रवृत्ति में उतार-चढ़ाव होने पर बार-बार लॉन्ग/शॉर्ट सिग्नल, फ़िल्टर शर्तें जोड़ने की सिफारिश की जाती है।

-

ब्रेकआउट के झूठे सिग्नल अधिक हो सकते हैं, पैरामीटर को उचित रूप से समायोजित किया जा सकता है या फ़िल्टर शर्तें जोड़ी जा सकती हैं।

-

बाजार में तीव्र उतार-चढ़ाव के दौरान स्टॉप लॉस का जोखिम, स्टॉप लॉस की सीमा बढ़ाई जा सकती है।

-

सीमित अनुकूलन स्थान, सीमित लाभप्रदता, अल्पकालिक ट्रेडिंग के लिए उपयुक्त।

अनुकूलन दिशाएँ

इस रणनीति के अनुकूलन के क्षेत्रों में शामिल हैं:

-

फ़िल्टर सिग्नल निर्धारित करने के लिए अधिक तकनीकी संकेतक जोड़ना।

-

पैरामीटर संयोजनों का अनुकूलन, सर्वोत्तम पैरामीटर खोजना।

-

जोखिम कम करने के लिए स्टॉप लॉस रणनीति में सुधार का प्रयास।

-

प्रवेश आयाम के स्वचालित समायोजन की क्षमता जोड़ना।

-

अधिक अवसर खोजने के लिए अन्य रणनीतियों के साथ संयोजन का प्रयास।

सारांश

कुल मिलाकर, यह रणनीति एक गतिशील ढलान पर आधारित प्रवृत्ति निर्धारण और ब्रेकआउट ट्रेडिंग का एक कुशल अल्पकालिक रणनीति है। इसका निर्णय सटीक है, जोखिम नियंत्रित है, और बाजार में अल्पकालिक अवसरों को कैप्चर करने के लिए उपयुक्त है। पैरामीटर के आगे अनुकूलन और फ़िल्टर शर्तों को जोड़कर, रणनीति की जीत दर और लाभ स्तर में सुधार किया जा सकता है।

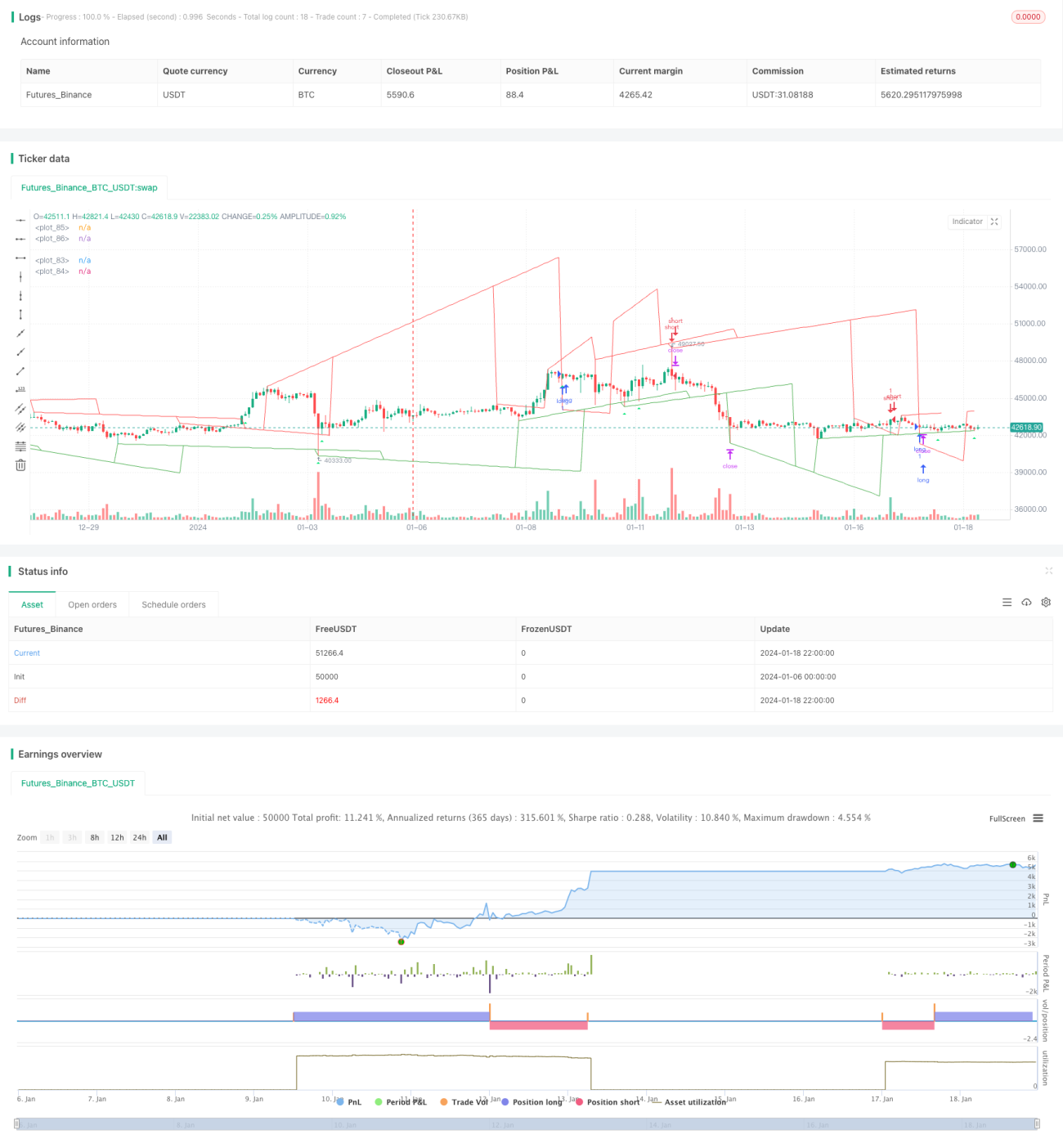

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1