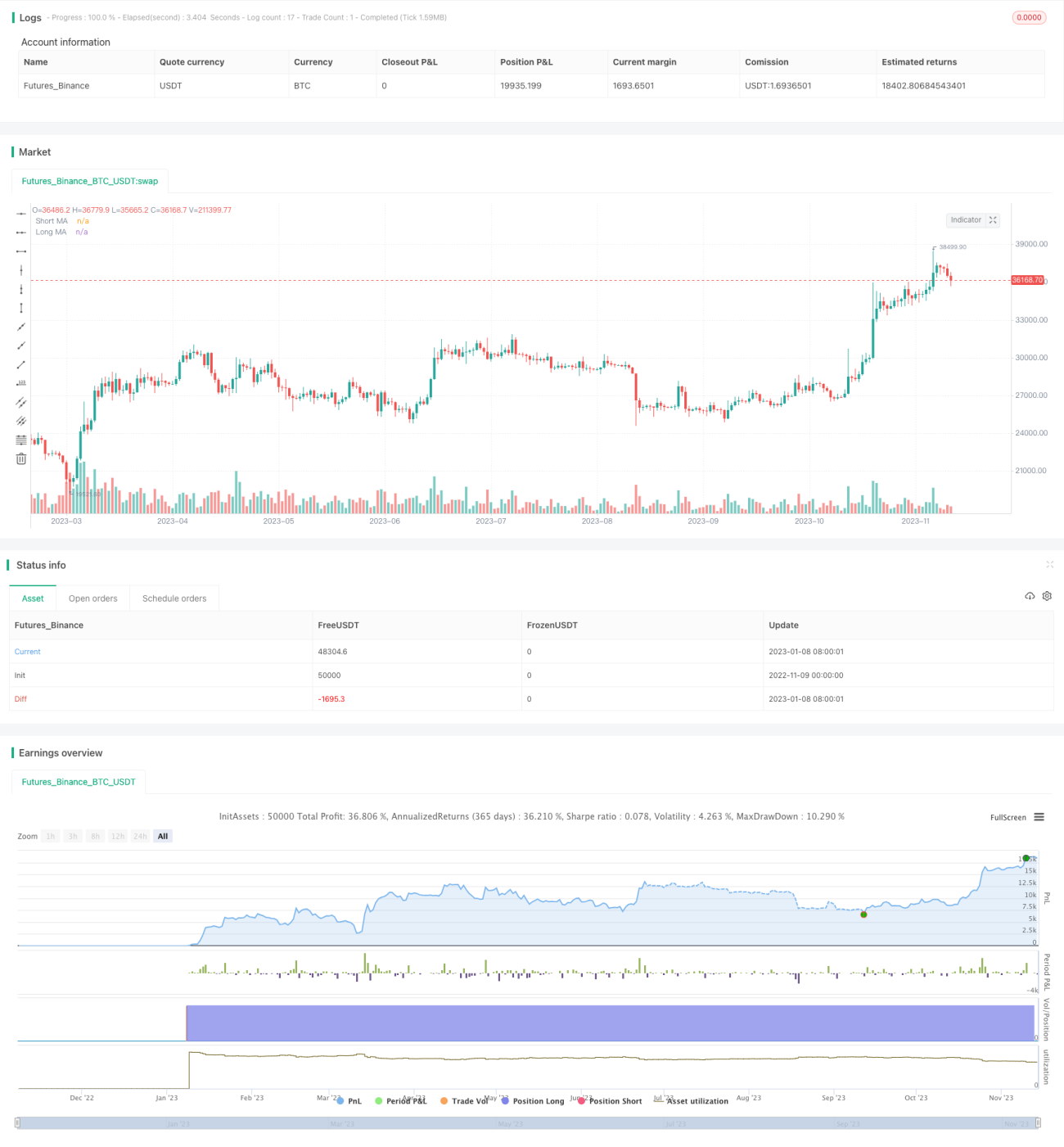

Strategi Perdagangan Kuantitatif DCA dengan Pembobotan Elemen Progresif

Ikhtisar

Strategi Perdagangan Kuantitatif DCA dengan Pembobotan Elemen Progresif adalah strategi perdagangan kuantitatif yang menggabungkan sinyal pemicu indikator moving average dengan mekanisme dollar cost averaging (DCA) berbobot progresif. Strategi ini bertujuan untuk memperoleh keuntungan yang lebih stabil di pasar dengan tren yang kuat melalui penilaian tren dan pemerataan biaya.

Prinsip

Strategi ini terutama terdiri dari tiga bagian:

-

Penentuan Sinyal Masuk

Menggunakan persilangan antara moving average cepat dan moving average lambat sebagai sinyal untuk masuk. Berdasarkan pengaturan pengguna, dapat dipilih SMA, EMA, atau HMA sebagai moving average cepat/lambat. Ketika moving average cepat menembus moving average lambat dari bawah, dihasilkan sinyal beli; ketika moving average cepat menembus moving average lambat dari atas, dihasilkan sinyal jual.

-

DCA Berbobot Progresif

Setelah sinyal beli terpicu, strategi akan segera membuka posisi untuk membangun posisi dasar. Selanjutnya, jika harga terus turun, strategi akan menambah posisi aman berikutnya dengan cara berbobot progresif. Harga untuk setiap penambahan posisi aman baru akan diturunkan dengan persentase tertentu secara berurutan mengacu pada harga posisi aman sebelumnya. Pada saat yang sama, jumlah dana untuk posisi aman baru juga akan diperbesar secara berurutan.

Dengan cara menambah posisi secara progresif, pemerataan biaya dapat dicapai sampai batas tertentu, sehingga memperoleh harga biaya yang lebih optimal sambil menjaga risiko perdagangan tetap terkendali.

-

Take Profit dan Stop Loss

Ketika harga naik melebihi garis take profit, strategi akan memilih take profit; ketika harga turun melebihi garis stop loss, strategi akan memilih stop loss.

Garis take profit ditetapkan secara tetap sebagai harga rata-rata transaksi posisi dasar dikalikan dengan (1 + rasio tetap).

Garis stop loss berfluktuasi seiring dengan harga posisi aman terakhir. Sinyal stop loss dikonfirmasi berdasarkan persentase tertentu di bawah harga transaksi posisi aman terakhir.

Keunggulan

-

Menggabungkan penilaian tren dengan pemerataan biaya membuat strategi lebih stabil

Penilaian tren dapat menghindari pasar yang bergerak sideways tanpa arah, sedangkan pemerataan biaya dapat memperoleh biaya yang lebih optimal dalam suatu tren.

-

Penambahan posisi secara progresif dapat mengendalikan risiko

Ukuran posisi setiap penambahan memiliki kisaran tertentu, dan posisi berikutnya memiliki persyaratan penarikan tertentu, sehingga risiko dapat dikendalikan.

-

Pemantauan real-time terhadap dana yang digunakan strategi

Kode dilengkapi dengan label pemantauan real-time, sehingga pengguna mengetahui dengan jelas batas atas dana yang digunakan strategi, menghindari penggunaan berlebih yang menyebabkan posisi dilikuidasi paksa.

-

Take profit dan stop loss yang fleksibel untuk setiap posisi

Posisi dasar dan posisi aman masing-masing dapat di-take profit dan di-stop loss, untuk mengunci laba dan mengendalikan risiko.

Risiko dan Optimasi

-

Fluktuasi harga yang tajam dapat menyebabkan penambahan posisi berkali-kali

Pada saat fluktuasi harga yang tajam, penambahan posisi mungkin terpicu beberapa kali sehingga meningkatkan kerugian. Hal ini dapat dikurangi dengan memperbesar persyaratan penarikan antara posisi aman berikutnya.

-

Pemilihan parameter moving average perlu dioptimalkan

Parameter moving average secara langsung mempengaruhi waktu masuk, sehingga perlu diuji untuk menentukan parameter yang sesuai pada instrumen yang berbeda.

-

Rasio take profit dan stop loss perlu diuji dan dioptimalkan

Rasio take profit dan stop loss berkaitan dengan tingkat pengembalian dan kontrol penarikan, dan perlu dioptimalkan melalui data backtest.

-

Dapat menetapkan kondisi likuidasi paksa berdasarkan penarikan atau waktu

Dapat diuji dengan menambahkan kondisi likuidasi paksa ketika penarikan maksimum terlampaui atau waktu holding melebihi batas, untuk lebih mengendalikan risiko.

Kesimpulan

Strategi Perdagangan Kuantitatif DCA dengan Pembobotan Elemen Progresif menggabungkan keunggulan penilaian tren dan pemerataan biaya, sehingga dapat memperoleh keuntungan yang stabil dalam tren yang kuat. Dengan mengoptimalkan pengaturan parameter, menyesuaikan ukuran posisi dan persyaratan penarikan antar posisi, perdagangan yang stabil dengan risiko terkendali dapat dicapai. Strategi ini dapat diterapkan pada hedge fund, CTA fund, dan dalam desain beberapa strategi kontrarian.

- 1