Strategi Pasangan Momentum dan Pembalikan Rel Ganda

Ikhtisar

Strategi ini menggabungkan berbagai indikator teknis untuk mewujudkan momentum reversal dan pasangan dual-track, sehingga menghasilkan sinyal trading. Strategi ini menggunakan pola 123 untuk menentukan titik balik, dan dipasangkan dengan indikator ergodic CSI untuk menghasilkan sinyal pasangan, sehingga memungkinkan trend following. Strategi ini bertujuan menangkap tren jangka pendek-menengah untuk memperoleh profit yang lebih tinggi.

Prinsip Strategi

Strategi ini terdiri dari dua bagian:

- Pola 123 untuk menentukan titik balik

- Indikator ergodic CSI menghasilkan sinyal pasangan

Pola 123 menentukan pembalikan harga berdasarkan hubungan harga penutupan tiga candle terakhir. Logika penentuan spesifiknya adalah:

Jika harga penutupan candle kedua lebih tinggi dari candle pertama, dan stoch fast serta slow saat ini keduanya di bawah 50, maka itu adalah sinyal beli.

Jika harga penutupan candle kedua lebih rendah dari candle pertama, dan stoch fast serta slow saat ini keduanya di atas 50, maka itu adalah sinyal jual.

Indikator ergodic CSI mempertimbangkan harga, true range, indikator tren, dan faktor lainnya untuk menilai pergerakan pasar secara komprehensif, menghasilkan zona beli dan jual.

Ketika indikator berada di atas zona beli, menghasilkan sinyal beli; ketika di bawah zona jual, menghasilkan sinyal jual.

Terakhir, sinyal pembalikan dari pola 123 dan sinyal jalur dari ergodic CSI digabungkan dengan operasi "AND" untuk mendapatkan sinyal strategi akhir.

Kelebihan Strategi

- Menangkap tren jangka pendek-menengah, potensi profit yang besar

- Penentuan pola pembalikan, dapat secara efektif menangkap titik balik

- Pasangan dual-track, dapat mengurangi sinyal palsu

Risiko Strategi

- Harga saham individual mungkin menyimpang, menyebabkan stop loss

- Pola pembalikan mudah terpengaruh oleh pasar yang bergejolak

- Ruang optimasi parameter terbatas, efeknya fluktuatif

Arah Optimasi

- Optimasi parameter untuk meningkatkan profitabilitas strategi

- Menambahkan logika stop loss untuk mengurangi kerugian per transaksi

- Menggabungkan model multi-faktor untuk meningkatkan kualitas pemilihan saham

Kesimpulan

Strategi ini secara efektif melacak tren jangka pendek-menengah melalui pola pembalikan dan pasangan dual-track. Dibandingkan dengan indikator teknis tunggal, strategi ini memiliki stabilitas dan tingkat profit yang lebih tinggi. Langkah selanjutnya adalah mengoptimalkan parameter lebih lanjut, serta menambahkan modul stop loss dan pemilihan saham untuk mengurangi drawdown dan meningkatkan efek keseluruhan.

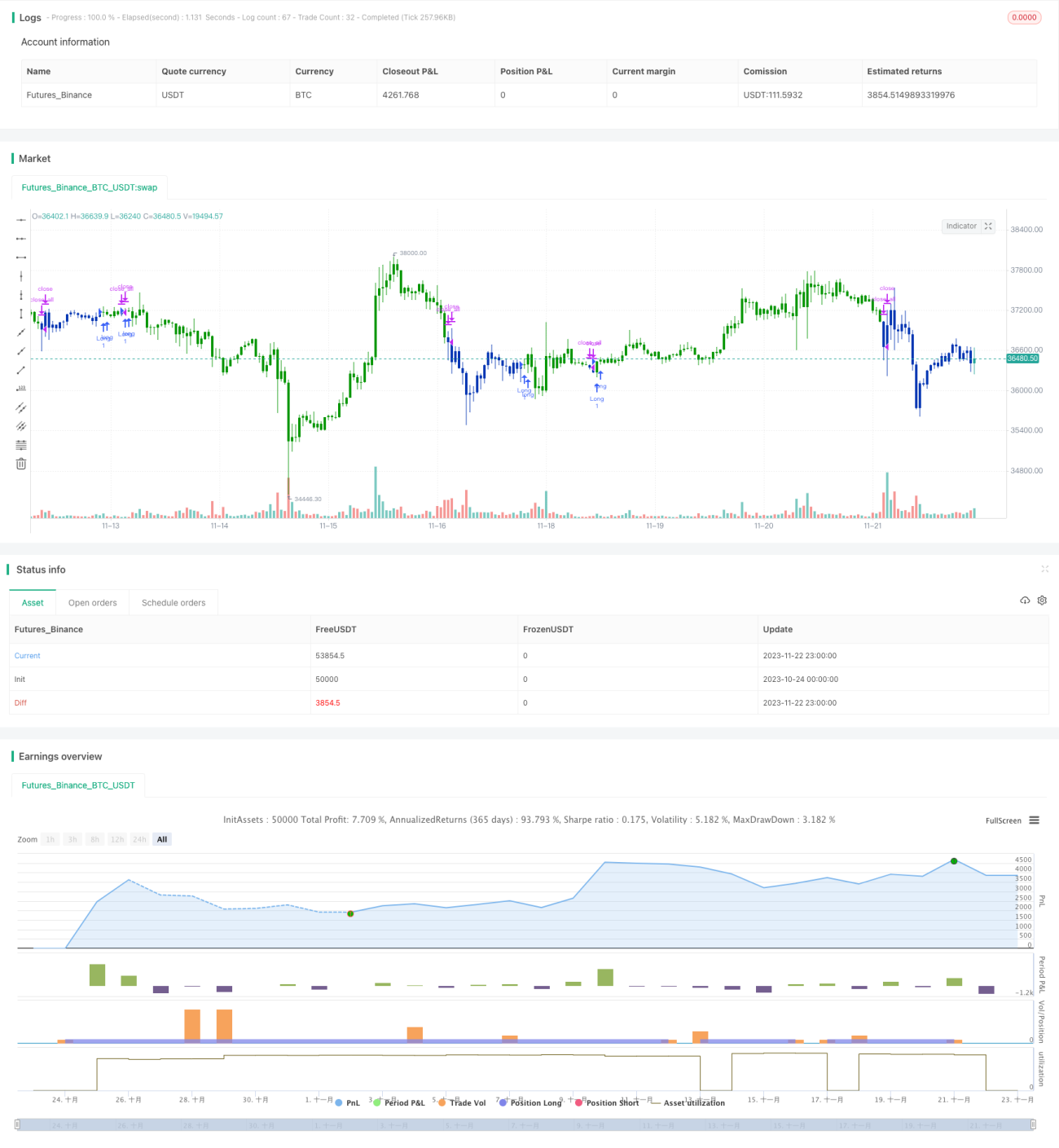

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/07/2020

// This is combo strategies for get a cumulative signal. - 1