Strategi Pengikut Tren Multi-Indikator

Ikhtisar

Strategi ini menggabungkan 3 indikator open-source untuk menentukan tren multi-timeframe, serta menetapkan stop loss dan take profit untuk mengunci keuntungan. Secara spesifik, strategi menggunakan indikator AK MACD BB untuk menentukan arah tren jangka pendek, indikator SSL untuk menyaring sebagian sinyal palsu, dan akhirnya menggabungkan indikator volume VSF untuk menilai kekuatan pembelian dan penjualan yang sebenarnya, sehingga menentukan waktu masuk. Selain itu, strategi telah menetapkan titik stop loss dan take profit untuk mengunci keuntungan, secara signifikan mengurangi risiko kerugian pada setiap transaksi.

Prinsip Strategi

-

Indikator AK MACD BB

Indikator ini menerapkan Bollinger Bands pada indikator MACD. Ketika garis indikator MACD menembus pita atas Bollinger Bands, akan menghasilkan sinyal beli; ketika menembus pita bawah, menghasilkan sinyal jual.

-

Indikator SSL

Indikator SSL menentukan apakah harga telah menembus moving average dan mendeteksi sinyal retest. Jika harga melintasi di atas moving average dan indikator SSL berwarna biru, tren naik; jika harga melintasi di bawah moving average dan indikator SSL berwarna merah, tren turun. Ini menghasilkan sinyal trading.

-

Indikator VSF

Indikator VSF menilai kekuatan pembeli dan penjual. Strategi hanya mengeluarkan sinyal ketika kekuatan pembeli atau penjual lebih besar dari 50%, menghindari breakout palsu.

-

Stop Loss dan Take Profit

Strategi ini memiliki 4 level take profit progresif, dari 1,5 kali hingga 3 kali lipat keuntungan. Sementara itu, stop loss tetap sebesar 2% diterapkan untuk mengontrol kerugian maksimum per transaksi.

Analisis Keunggulan

-

Kombinasi multi-indikator, akurasi tinggi

Dengan menggunakan berbagai indikator untuk menentukan tren multi-timeframe, sinyal palsu dapat disaring, sehingga penilaian lebih akurat.

-

Take profit dan stop loss otomatis, risiko terkendali

Strategi ini memiliki pengaturan take profit dan stop loss bawaan yang dapat membatasi kerugian per transaksi sekitar 2%, menghindari kerugian besar.

-

Data backtest yang sangat baik

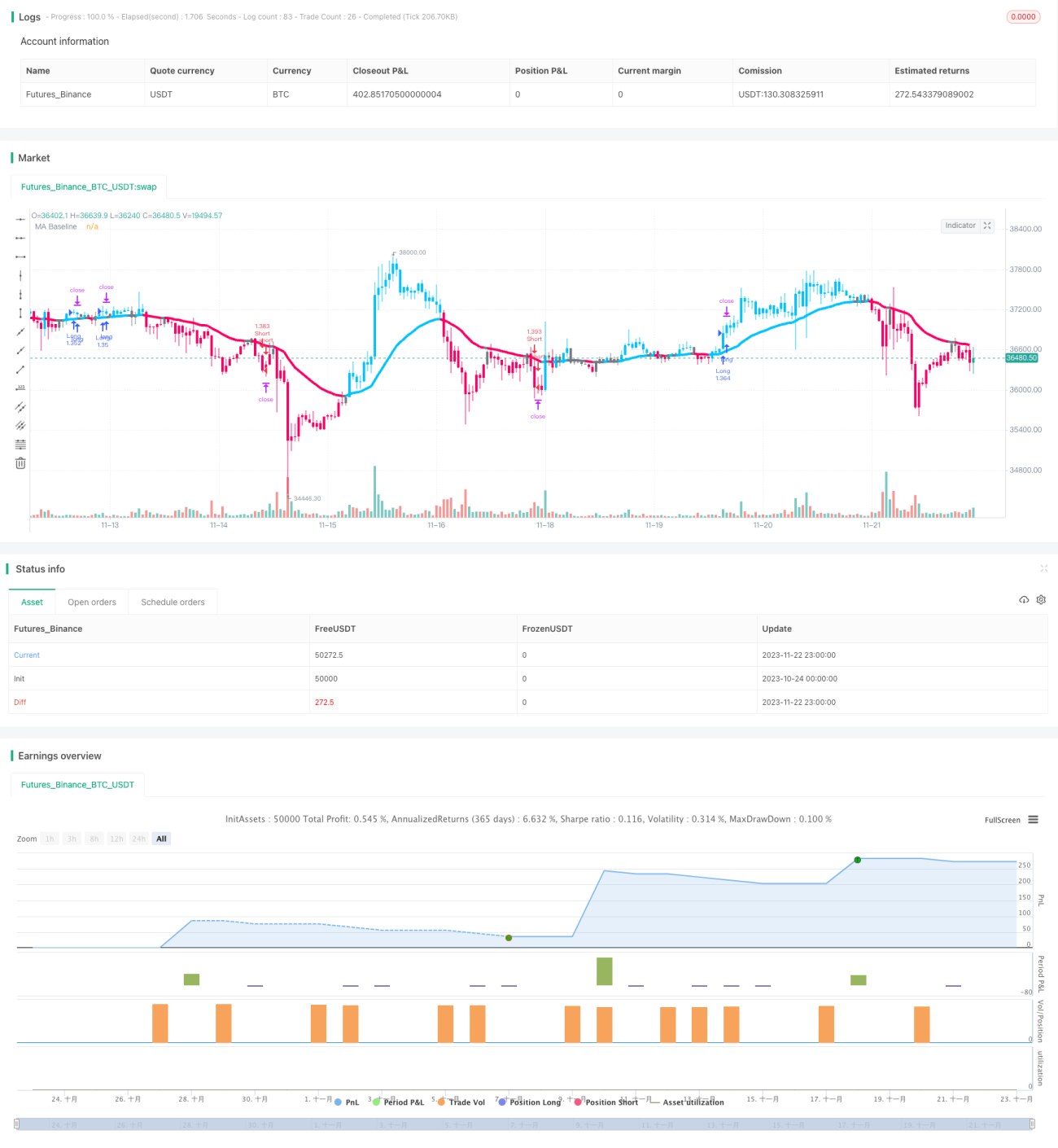

Menurut backtest dari pengembang, dari 100 transaksi, transaksi yang menguntungkan mencapai 74%, dengan total keuntungan 427%.

Analisis Risiko dan Penanganan

-

Risiko fluktuasi pasar yang ekstrem

Selama kisaran konsolidasi level besar, mungkin terjadi beberapa kerugian kecil secara berurutan. Dalam hal ini, stop loss tetap dapat disesuaikan atau perdagangan dapat dihentikan sementara.

-

Risiko keterbatasan posisi long dan short

Saat ini, strategi dapat digunakan untuk posisi long maupun short. Jika dibatasi hanya untuk long atau hanya short, peluang keuntungan akan berkurang setengahnya.

-

Risiko sesi perdagangan

Strategi menggunakan data 5 menit untuk pengambilan keputusan. Jika hanya ada beberapa jam data dalam satu hari perdagangan, sampel tidak mencukupi dan sinyal mungkin tidak dapat diandalkan.

Arah Optimasi Strategi

-

Optimasi parameter stop loss dan take profit

Pengujian level stop loss dan take profit yang berbeda dapat dilakukan untuk menemukan parameter optimal. Stop loss yang terlalu kecil tidak efektif mengendalikan risiko, sedangkan terlalu besar dapat menyebabkan hilangnya keuntungan yang lebih besar.

-

Penambahan penyesuaian posisi otomatis

Dapat diatur trailing stop atau moving stop untuk mengunci keuntungan. Atau menambah posisi berdasarkan kondisi tertentu untuk meraih keuntungan lebih besar.

-

Kombinasi dengan indikator lain

Menguji kombinasi indikator yang berbeda untuk menentukan kombinasi mana yang paling efektif. Indikator tambahan juga dapat disertakan untuk verifikasi silang.

-

Optimasi parameter

Pengujian backtest dengan parameter yang berbeda dapat dilakukan untuk menemukan arah optimasi. Dalam strategi ini, mengubah parameter Bollinger Bands atau moving average mungkin menghasilkan hasil yang lebih baik.

Kesimpulan

Strategi ini mengintegrasikan beberapa indikator untuk menentukan arah tren, dilengkapi dengan take profit dan stop loss otomatis, sehingga dapat meraih keuntungan dalam tren kuat sekaligus mengendalikan kerugian per transaksi dalam kisaran yang sangat kecil. Berdasarkan data backtest dari pengembang, rasio profitabilitas dan tingkat keuntungan sangat ideal. Melalui optimasi tertentu, stabilitas dan profitabilitas strategi berpotensi ditingkatkan lebih lanjut.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1