Strategi Pelacakan Momentum Adaptif Multi-Faktor

Ikhtisar

Strategi Momentum Adaptif Multi-Faktor mengidentifikasi tren pasar dan level support/resistance kunci melalui integrasi berbagai indikator teknis, memungkinkan perdagangan otomatis pada aset dengan volatilitas tinggi seperti mata uang kripto. Strategi ini menggabungkan indikator RSI, MACD, Stochastic, dan lainnya untuk menentukan waktu beli/jual, serta menggunakan persentase perubahan harga untuk identifikasi pola yang lebih akurat.

Prinsip Strategi

Inti dari Strategi Momentum Adaptif Multi-Faktor terletak pada integrasi berbagai indikator teknis. Strategi ini terutama menggunakan komponen berikut:

-

Indikator RSI untuk menentukan kondisi overbought/oversold. Dengan parameter yang berbeda, dapat mengidentifikasi sinyal RSI standar atau sinyal Connors RSI yang telah dimodifikasi, sehingga menilai apakah ada peluang pembalikan.

-

Indikator MACD membantu menentukan arah tren. Ketika garis MACD memotong ke atas atau ke bawah garis sinyal, maka akan menghasilkan sinyal beli dan jual.

-

Indikator Stochastic mengidentifikasi area overbought/oversold. Sinyal kombinasi golden cross/death cross antara garis K dan D digunakan untuk menentukan apakah terjadi pembalikan.

-

Persentase perubahan harga digunakan untuk memverifikasi apakah terjadi breakout yang valid. Perubahan persentase harga tertinggi, terendah, dan penutupan dalam periode tertentu dihitung untuk menentukan apakah terjadi breakout yang sebenarnya.

-

Indikator EMA menentukan tren bull/bear pada kerangka waktu yang lebih besar. Ketika garis cepat memotong ke atas garis lambat, itu adalah sinyal bullish; ketika memotong ke bawah, itu adalah sinyal bearish.

Strategi ini memilih untuk mengambil posisi long atau short berdasarkan kondisi pasar bullish/bearish, dan menetapkan stop loss serta take profit setelah masuk posisi untuk mengelola risiko secara efektif. Ketika sinyal pembalikan muncul, posisi ditutup. Seluruh proses pengambilan keputusan menggabungkan penilaian multi-faktor, menghasilkan keputusan yang lebih akurat.

Analisis Keunggulan

Strategi ini memiliki beberapa keunggulan berikut:

-

Penggerak multi-faktor memberikan keunggulan dalam penilaian. Dibandingkan dengan indikator tunggal, kombinasi beberapa indikator dapat saling memverifikasi, membuat hasil lebih akurat dan andal, sehingga menghemat biaya perdagangan yang tidak perlu.

-

Kondisi yang ketat menghindari perdagangan yang salah. Strategi menetapkan persyaratan ketat untuk kondisi beli/jual, membutuhkan beberapa indikator untuk memberikan sinyal secara bersamaan, sehingga dapat menyaring kebisingan yang besar dan menghindari perdagangan yang salah.

-

Parameter adaptif mengurangi intervensi manusia. Strategi memiliki kemampuan bawaan untuk menghitung parameter indikator secara dinamis, menghindari subjektivitas pemilihan parameter secara manual, sehingga parameter strategi menjadi lebih ilmiah dan objektif.

-

Mekanisme stop loss dan take profit mengelola risiko. Setelah membuka posisi, strategi menghitung dan menggambar level stop loss serta take profit secara real-time, yang secara efektif dapat mengendalikan kerugian per perdagangan dan menghindari likuidasi.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko yang perlu diwaspadai:

-

Kemungkinan indikator memberikan sinyal yang salah. Meskipun verifikasi multi-indikator dapat secara signifikan mengurangi tingkat sinyal palsu, kemungkinan masih ada. Hal ini dapat menyebabkan kerugian yang tidak perlu.

-

Risiko stop loss tertembus. Dalam kondisi pasar yang ekstrem, harga dapat turun drastis (cliff-like decline), menyebabkan stop loss yang ditetapkan mudah tertembus, mengakibatkan kerugian besar.

-

Overfitting akibat optimasi parameter. Meskipun parameter dinamis menghindari subjektivitas pemilihan manual, hal ini juga dapat menyebabkan parameter menjadi terlalu optimal dan kehilangan kemampuan generalisasi.

Solusi yang sesuai:

- Memperketat kondisi penyaringan sinyal untuk mengurangi tingkat sinyal palsu.

- Menggunakan metode pembukaan posisi secara bertahap untuk menghindari stop loss yang terlalu besar dalam satu kali perdagangan.

- Menambahkan jumlah sampel pengujian dan mengevaluasi stabilitas parameter secara ketat.

Arah Optimasi Strategi

Strategi Momentum Adaptif Multi-Faktor masih memiliki beberapa dimensi yang dapat dioptimalkan:

-

Menambah jumlah faktor penilaian. Menggabungkan sinyal dari lebih banyak jenis indikator yang berbeda, seperti volatilitas, volume perdagangan, dan sebagainya untuk penilaian tambahan.

-

Mengoptimalkan algoritma mekanisme stop loss. Dapat memperkenalkan algoritma stop loss yang lebih canggih seperti trailing stop loss, volatility stop loss, untuk lebih mengurangi probabilitas stop loss tertembus.

-

Memperkenalkan model pembelajaran mesin. Menggunakan model seperti RNN, LSTM untuk memodelkan data historis guna membantu pengambilan keputusan beli/jual.

-

Integrasi strategi. Menggunakan beberapa sub-strategi dan mengintegrasikannya dengan metode pembelajaran ensemble untuk mendapatkan kinerja keseluruhan yang lebih stabil.

Ringkasan

Strategi Momentum Adaptif Multi-Faktor mengintegrasikan berbagai indikator teknis untuk mengidentifikasi waktu beli/jual. Dibandingkan dengan indikator tunggal, strategi ini memberikan penilaian yang lebih akurat, serta memiliki parameter adaptif bawaan dan mekanisme stop loss untuk mengelola risiko. Langkah selanjutnya, dengan memperkenalkan lebih banyak faktor penilaian tambahan, algoritma stop loss yang canggih, dan metode pembelajaran mesin, efektivitas strategi ini dapat lebih ditingkatkan.

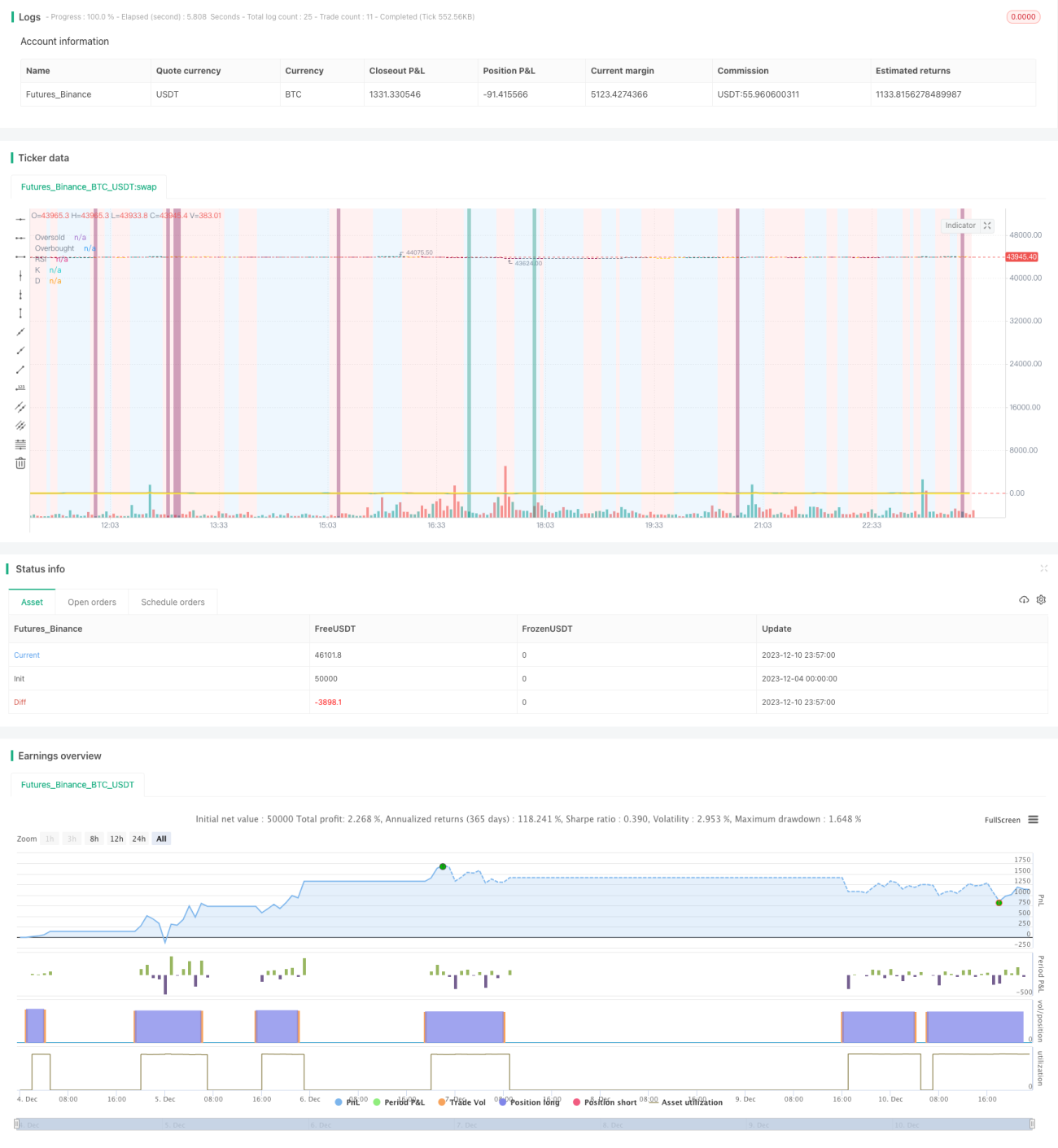

/*backtest

start: 2023-12-04 00:00:00

end: 2023-12-11 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

// ██████╗██████╗ ███████╗ █████╗ ████████╗███████╗██████╗ ██████╗ ██╗ ██╗ - 1