Strategi Trading Pelacakan Candlestick Grid Dua Arah

Ringkasan

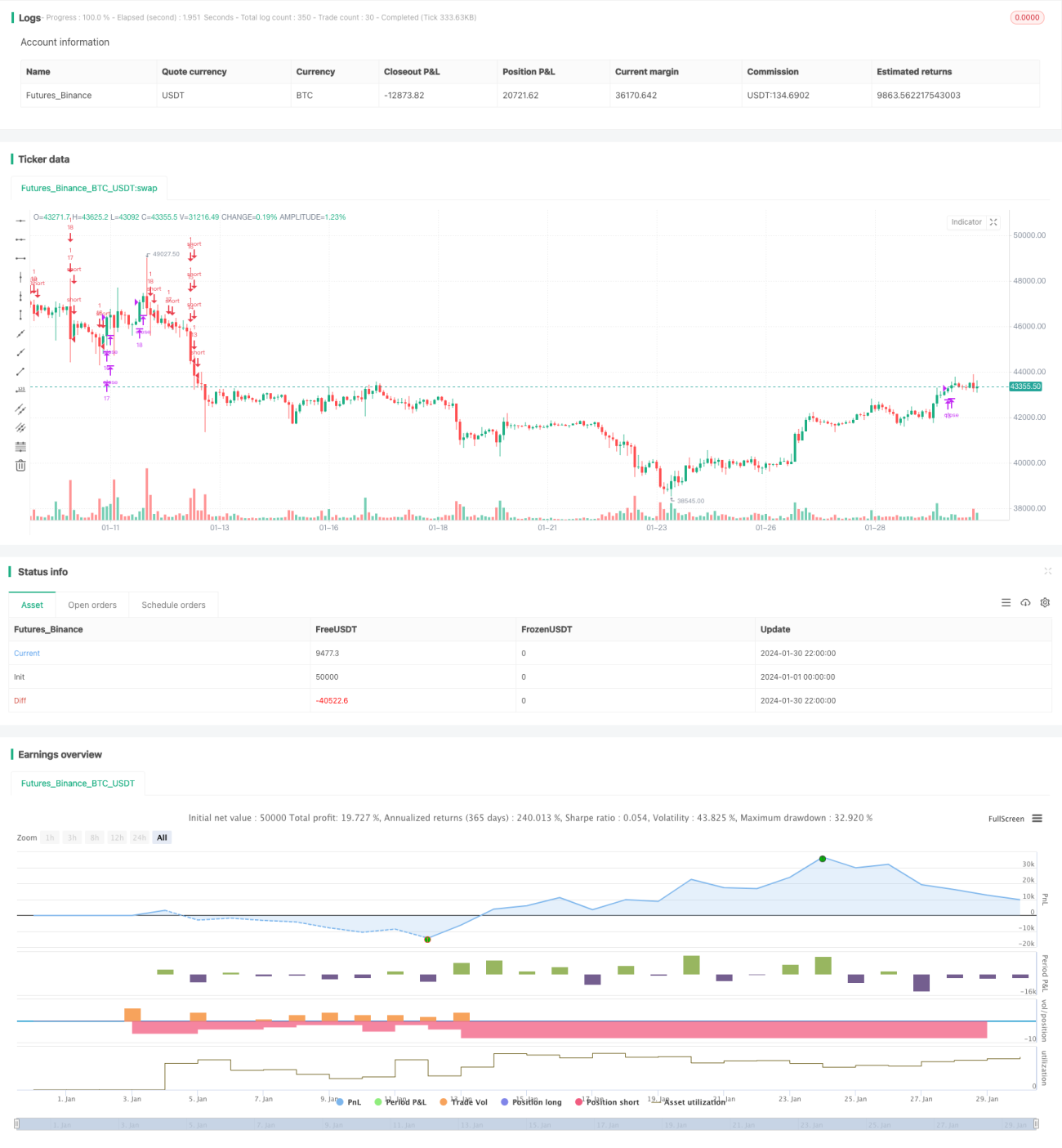

Strategi ini adalah strategi trading grid dua arah yang didasarkan pada perubahan real-time candlestick. Strategi ini dapat menghasilkan keuntungan stabil baik di pasar bullish maupun bearish.

Prinsip Strategi

-

Berdasarkan jumlah grid yang ditentukan pengguna, secara otomatis menghitung rentang harga grid dan harga setiap grid.

-

Ketika harga menembus harga grid, buka posisi beli (long) dengan jumlah tetap; ketika harga turun di bawah harga grid, tutup posisi beli dan buka posisi jual (short).

-

Dengan cara ini, ketika harga berfluktuasi dalam rentang grid, keuntungan dapat diperoleh dengan melacak perubahan harga.

Analisis Keunggulan

-

Secara otomatis menghitung rentang grid yang wajar, tanpa perlu menentukan support dan resistance secara manual.

-

Perdagangan dua arah, dapat beradaptasi dengan kondisi pasar yang berubah-ubah.

-

Jumlah pembukaan posisi tetap, membantu pengendalian risiko.

-

Kode intuitif dan sederhana, mudah dipahami dan dimodifikasi.

Analisis Risiko

-

Fluktuasi pasar yang tajam dapat menyebabkan kerugian membesar.

-

Akumulasi biaya transaksi juga akan mempengaruhi keuntungan akhir.

-

Perlu menentukan jumlah grid secara wajar; terlalu banyak grid akan meningkatkan frekuensi transaksi tetapi keuntungan per transaksi terbatas.

Arah Optimasi

-

Menambahkan strategi stop loss untuk menghindari kerugian membesar.

-

Menambahkan fungsi penyesuaian jumlah grid secara dinamis.

-

Pertimbangkan penambahan leverage untuk memperbesar volume perdagangan.

Kesimpulan

Strategi ini secara keseluruhan memiliki ide yang jelas dan sederhana, memperoleh pendapatan stabil melalui perdagangan grid dua arah, namun juga memiliki risiko perdagangan tertentu. Melalui optimasi berkelanjutan, diharapkan dapat mencapai hasil yang lebih baik.

- 1