Strategi Indeks Momentum Pembalikan Ganda

Ikhtisar

Strategi Indeks Momentum Pembalikan Ganda adalah strategi kombinasi yang menggabungkan strategi Pembalikan 123 dan strategi Indeks Momentum Relatif (RMI). Strategi ini bertujuan untuk meningkatkan akurasi keputusan perdagangan dengan memanfaatkan sinyal ganda.

Prinsip Strategi

Strategi ini terdiri dari dua bagian:

-

Strategi Pembalikan 123

- Lakukan posisi beli (long) ketika harga penutupan kemarin lebih rendah dari hari sebelumnya, harga penutupan hari ini lebih tinggi dari hari sebelumnya, dan garis Slow K 9-hari di bawah 50.

- Lakukan posisi jual (short) ketika harga penutupan kemarin lebih tinggi dari hari sebelumnya, harga penutupan hari ini lebih rendah dari hari sebelumnya, dan garis Fast K 9-hari di atas 50.

-

Strategi Indeks Momentum Relatif (RMI)

- RMI adalah variasi dari RSI yang menambahkan faktor momentum. Rumusnya: RMI = (SMA momentum naik) / (SMA momentum turun) * 100

- Lakukan posisi beli ketika RMI di bawah garis jenuh beli (overbought); lakukan posisi jual ketika RMI di atas garis jenuh jual (oversold).

Strategi kombinasi ini hanya akan menghasilkan sinyal perdagangan ketika sinyal ganda dari Pembalikan 123 dan RMI searah. Hal ini dapat secara efektif mengurangi peluang perdagangan yang salah.

Analisis Keunggulan Strategi

Strategi ini memiliki keunggulan sebagai berikut:

- Menggabungkan dua indikator, meningkatkan akurasi sinyal.

- Memanfaatkan strategi pembalikan, cocok untuk pasar yang bergerak sideways (oscilasi).

- Indikator RMI sensitif, dapat mengidentifikasi titik balik tren yang kuat.

Analisis Risiko Strategi

Strategi ini juga memiliki beberapa risiko:

- Filter ganda dapat melewatkan sebagian peluang perdagangan.

- Sinyal pembalikan dapat menghasilkan kesalahan interpretasi.

- Pengaturan parameter RMI yang tidak tepat dapat memengaruhi hasil.

Risiko-risiko ini dapat dikurangi dengan menyesuaikan kombinasi parameter dan mengoptimalkan metode perhitungan indikator.

Arah Optimalisasi Strategi

Strategi ini juga dapat dioptimalkan dari beberapa aspek berikut:

- Menguji berbagai kombinasi parameter untuk menemukan parameter terbaik.

- Mencoba kombinasi indikator pembalikan yang berbeda, seperti KDJ, MACD, dll.

- Menyesuaikan rumus RMI agar lebih sensitif.

- Menambahkan mekanisme stop-loss untuk mengendalikan kerugian per perdagangan.

- Menggabungkan volume perdagangan untuk menghindari sinyal palsu.

Kesimpulan

Strategi Indeks Momentum Pembalikan Ganda melalui penyaringan sinyal ganda dan optimalisasi parameter dapat secara efektif meningkatkan akurasi keputusan perdagangan dan mengurangi kemungkinan sinyal yang salah. Strategi ini cocok untuk pasar yang bergerak sideways dan dapat menggali peluang pembalikan. Strategi ini dapat lebih ditingkatkan efeknya dan mengurangi risiko dengan menyesuaikan parameter serta mengoptimalkan metode perhitungan indikator.

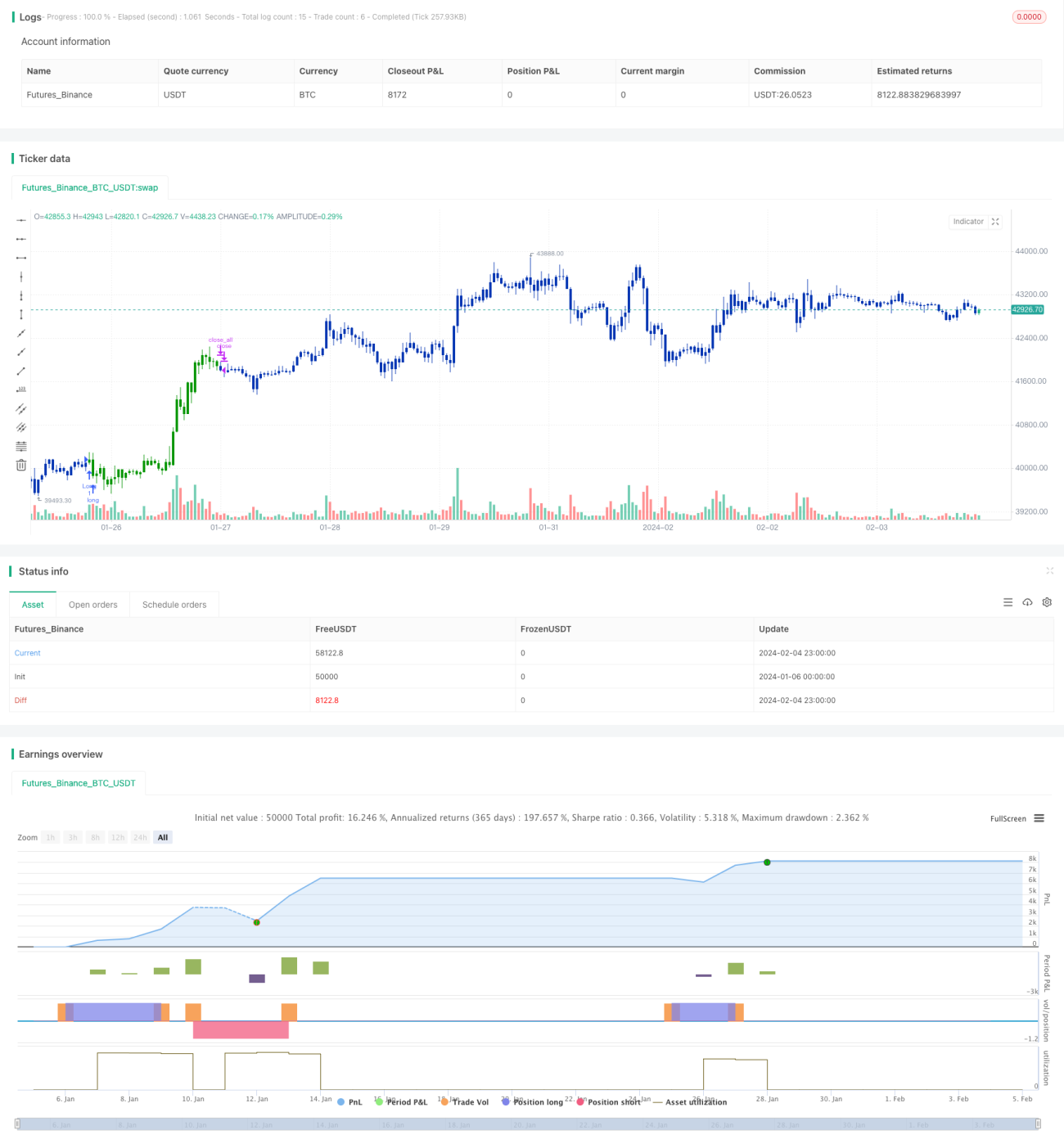

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal. - 1