Strategi Trading Garis Tren dengan Kemiringan Dinamis

Gambaran Umum

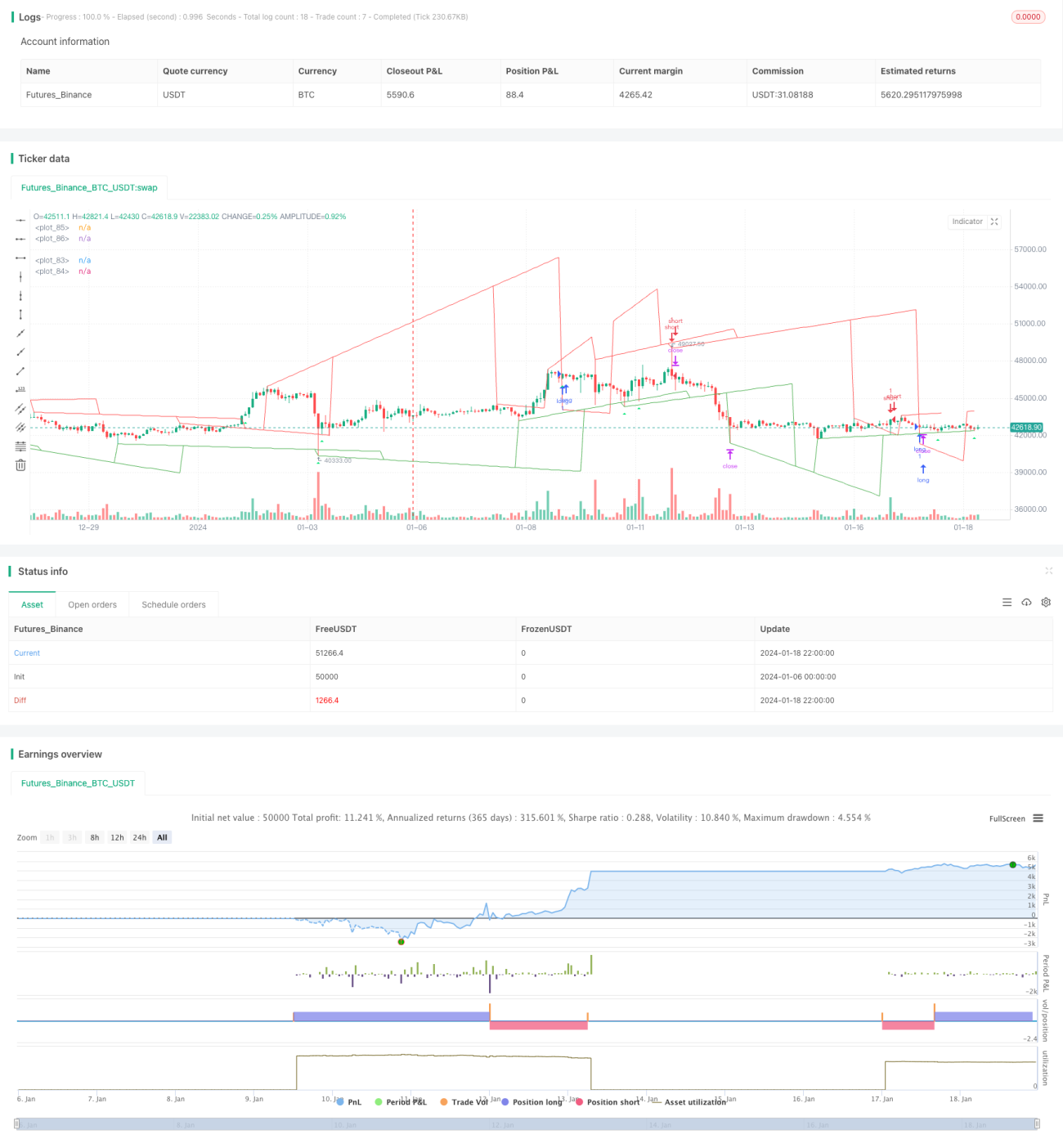

Ide inti dari strategi ini adalah menggunakan kemiringan dinamis untuk menilai arah tren harga, dikombinasikan dengan penembusan untuk menghasilkan sinyal trading. Secara spesifik, strategi ini melacak titik tertinggi dan terendah baru harga secara real-time, menghitung kemiringan dinamis berdasarkan perubahan harga dalam periode waktu yang berbeda, dan kemudian menggabungkan penembusan harga terhadap garis tren untuk menentukan sinyal bullish atau bearish.

Prinsip Strategi

Strategi ini terutama dibagi menjadi beberapa langkah berikut:

-

Menentukan harga tertinggi dan terendah: Melacak harga tertinggi dan terendah dalam periode tertentu (misalnya 20 candle) untuk menentukan apakah terjadi新高 (tertinggi baru) atau新低 (terendah baru).

-

Menghitung kemiringan dinamis: Mencatat nomor candle saat terbentuknya新高或新低, kemudian menghitung kemiringan dinamis dari titik tertinggi/terendah baru tersebut hingga titik tertinggi/terendah setelah periode tertentu (misalnya 9 candle).

-

Menggambar garis tren: Menggambar garis tren naik dan turun berdasarkan kemiringan dinamis.

-

Memperpanjang dan memperbarui garis tren: Ketika harga menembus garis tren, garis tren akan diperpanjang dan diperbarui.

-

Sinyal trading: Menggabungkan penembusan harga terhadap garis tren untuk menentukan sinyal beli (long) dan jual (short).

Keunggulan Strategi

Strategi ini memiliki keunggulan sebagai berikut:

- Penilaian arah tren secara dinamis, responsif terhadap perubahan pasar.

- Mampu mengontrol stop loss secara wajar, drawdown kecil.

- Sinyal trading penembusan yang jelas, implementasi sederhana.

- Parameter yang dapat disesuaikan, adaptif tinggi.

- Struktur kode yang jelas, mudah dipahami dan dikembangkan lebih lanjut.

Risiko dan Solusi

Strategi ini juga memiliki beberapa risiko:

- Sinyal bisa bergantian saat pasar sideways (konsolidasi), disarankan menambahkan kondisi filter.

- Sinyal palsu penembusan mungkin cukup banyak, dapat disesuaikan parameternya atau ditambahkan filter.

- Risiko stop loss saat pergerakan harga ekstrem, dapat diperbesar jarak stop loss.

- Ruang optimalisasi terbatas, profitabilitas terbatas, cocok untuk trading jangka pendek.

Arah Optimasi

Bagian yang dapat dioptimalkan dari strategi ini meliputi:

- Menambahkan lebih banyak indikator teknikal untuk menyaring sinyal.

- Mengoptimalkan kombinasi parameter untuk menemukan parameter terbaik.

- Mencoba memperbaiki strategi stop loss untuk mengurangi risiko.

- Menambahkan fungsi penyesuaian otomatis jarak masuk posisi.

- Mencoba menggabungkan dengan strategi lain untuk menemukan lebih banyak peluang.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi jangka pendek yang efisien berdasarkan kemiringan dinamis untuk menilai tren dan entry saat penembusan. Strategi ini memiliki akurasi penilaian yang baik, risiko terkendali, dan cocok untuk menangkap peluang jangka pendek di pasar. Dengan mengoptimalkan parameter lebih lanjut dan menambahkan kondisi filter, tingkat kemenangan dan profitabilitas strategi dapat ditingkatkan.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1