移動平均線とスーパートレンドに基づくトレーリングストップ戦略

概要

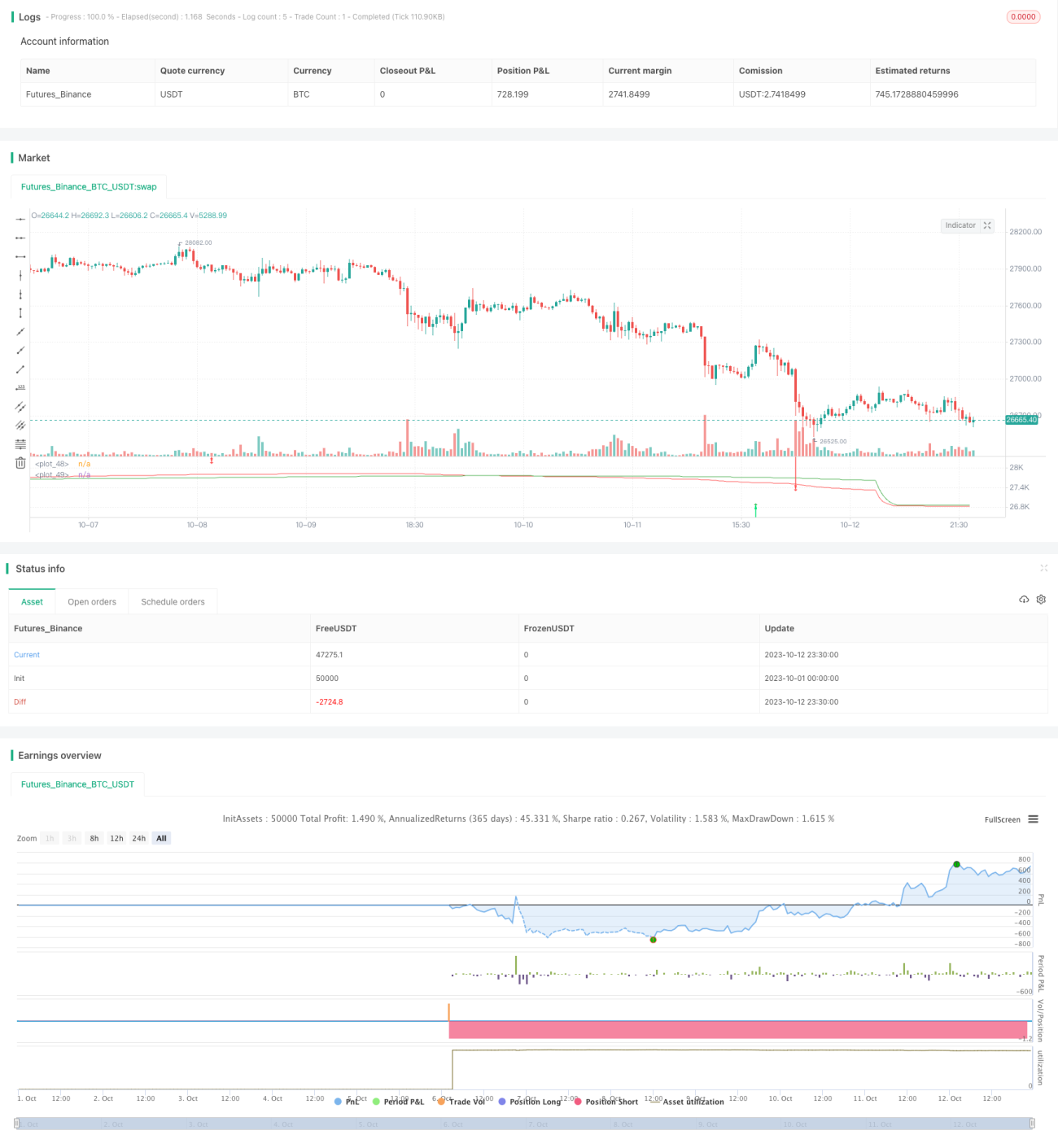

本戦略は、移動平均線インジケーターとスーパートレンドインジケーターを融合し、トレーリングストップ機能を備えたトレンドフォロー戦略です。移動平均線によるトレンド判断力と、スーパートレンドによるストップロス機能を最大限に活用し、トレンドに追随しながらリスクをコントロールします。

戦略の原理

本戦略は2本のFRAMA移動平均線を用いて売買シグナルを判断し、スーパートレンドインジケーターでフィルタリングを行います。

具体的には、短期線が長期線を上抜けたときに買いシグナル、下抜けたときに売りシグナルを生成します。偽のブレイクを避けるため、スーパートレンドインジケーターが同じ方向を示している場合にのみ取引を実行します。

ポジション管理については、スーパートレンドインジケーターの方向転換をストップロスの出口シグナルとして使用します。スーパートレンドが反転した場合、ストップロスでポジションをクローズします。

また、オプションでトレーリングストップ機能を設定できます。一定の利益を達成した後、トレーリングストップを有効にして利益を確定することができます。

優位性分析

- 移動平均線を利用してトレンド方向を判断することで、市場ノイズを効果的に除去し、正確にトレンドを判断できます。

- スーパートレンドインジケーターによるフィルタリングにより、偽のブレイクによる誤取引を回避します。

- スーパートレンドの方向転換をストップロスとして使用することで、迅速に損切りを行い、リスクを効果的に管理できます。

- オプションのトレーリングストップ機能により、利益を最大化できます。

リスク分析

- トレンドフォロー戦略であるため、トレンドが揉み合う局面ではポジションが拘束されるリスクがあり、ポジションサイズの管理に注意が必要です。

- 移動平均線には遅延性があるため、エントリーが早すぎたり遅すぎたりする可能性があります。

- スーパートレンドインジケーターのパラメーター設定が不適切だと、ストップロスが過激または保守的になりすぎる恐れがあります。

- トレーリングストップを有効にする場合、適切なトレーリング幅を設定しないと、過度に早い損切りを招く可能性があります。

これらのリスクは、移動平均線のパラメーター調整、スーパートレンドインジケーターの設定最適化、トレーリングストップの適切な使用により軽減できます。

最適化の方向性

本戦略は以下の点から最適化が可能です。

- 移動平均線パラメーターの最適化:最適なパラメーター組み合わせを探す

異なる期間パラメーターの組み合わせをテストし、平滑効果と感度の最適なバランスを見つけます。

- スーパートレンドインジケーターのパラメーターカスタマイズ

異なるATR期間と倍率パラメーターをテストし、ストップロス効果を最適化します。

- 他のインジケーターによるフィルタリング追加

コモディティチャネルインデックス(CCI)やボラティリティ指標などの追加フィルターをテストし、シグナルをさらに絞り込みます。

- トレーリングストップパラメーターの最適化

異なるトレーリングストップ幅をテストし、利益最大化とリスク管理の最適なパラメーターを見つけます。

- 他のストップロス戦略との組み合わせ

一般的なストップロス、ボラティリティストップロス、トレーリングストップなどの戦略との併用をテストします。

まとめ

本戦略は、移動平均線によるトレンド判断とスーパートレンドによるストップロス管理を統合し、トレーリングストップ機能を備えた比較的完成度の高いトレンドフォロー戦略です。パラメーター最適化とリスク管理により、戦略の安定性と収益性をさらに高めることができます。本戦略は、ある程度の知識を持つアルゴリズムトレーダーに適しています。

- 1