概要

本戦略は、RSIインジケーターと価格移動平均線を組み合わせ、株価が移動平均線を下回った際に売られ過ぎのエリアで買い建て(ロング)する機会を捉えます。株価がさらに下落するにつれ、戦略は事前設定されたパーセンテージに従って段階的に買い増しを行い、平均保有コストの低下を図ります。ポジションの利益が設定された利確パーセンテージに達した場合、戦略はポジションを決済します。同時に、本戦略は段階的利確(プログレッシブ・テイクプロフィット)メカニズムを導入し、既に実現した個別ポジションの利益に基づいて、全体ポジションの利確価格を動的に調整します。これにより、損失リスクを効果的に低減し、段階的な退出を実現します。

戦略の仕組み

-

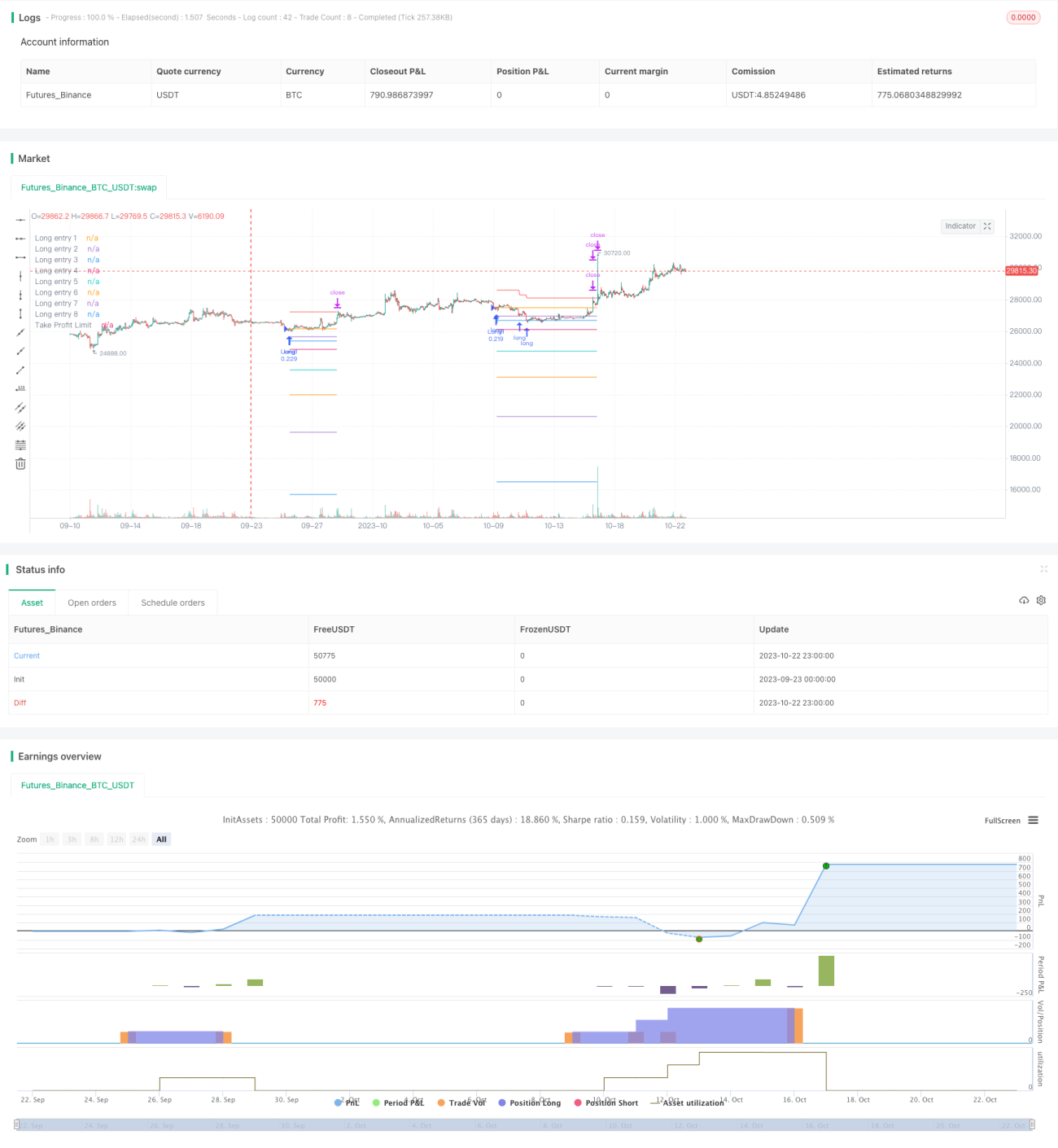

RSIが売られ過ぎラインの29を下回り、かつ終値が移動平均線を下回った場合、ロングの最初の注文を発注します。

-

株価が最初の注文から2%下落した際に追加で買い増し(ロング)します。3%下落した際に3回目の買い増し、以降最大8回まで買い増しを行います。これにより分割建ての効果が得られます。

-

ポジションを保有するたびに、その時点の建て値が記録されます。これらの価格ポイントがエントリーの参考価格となります。また、チャート上にこれらの価格ラインを描画します。

-

ポジション保有後、保有ポジションの平均価格が計算されます。平均価格の3%を各ポジションの利確価格、4%を全体ポジションの利確価格とします。

-

価格がいずれかのポジションの利確価格を上回った場合、そのポジションを決済します。

-

段階的利確の計算方法:ポジションを1つ決済するたびに、全体の利確価格からそのポジションで実現した利益を差し引きます。これにより利確ラインが緩やかに下方に移動し、全ポジションの利益が最大損失を補填できる場合にのみ、全てのポジションが利確されます。

-

価格が段階的利確ラインに達した場合、全てのポジションを決済します。

優位性の分析

-

RSIインジケーターは売られ過ぎゾーンを比較的正確に判断できるため、反転のチャンスを捉えやすくなります。

-

複数回に分けて買い増しを行うことで、安値で平均保有コストを下げることができます。

-

段階的利確により損失リスクを低減し、段階的な退出が可能です。たとえ損失が発生しても一定範囲に抑えられます。

-

利確比率や買い増し比率を設定可能で、市場に応じて戦略のリスクを調整できます。

-

チャート上に建て参考ラインや利確ラインを描画することで、ポジション分布を直感的に把握できます。

リスク分析

-

レンジ相場では、何度もエントリーと利確が発生し、取引頻度が高くなりスリッページ損失が生じる可能性があります。RSIパラメータを適度に緩和し、取引回数を減らすことができます。

-

買い増し回数や比率の設定が不適切だと過剰取引につながる恐れがあり、資金状況に応じて慎重に設定する必要があります。

-

市場がさらに下落して買い増しを続ける場合、底なしのリスクに直面する可能性があります。買い増し回数の上限を事前に設定し、最後の買い増し比率は保守的にすべきです。

-

利確比率を小さく設定しすぎると、早期利確につながる可能性があります。過去のバックテストデータに基づき適切な利確比率を設定すべきです。

最適化の方向性

-

MACDなどのインジケーターを導入してRSIシグナルをフィルタリングし、無駄な取引を減らすことができます。

-

ATRに基づいてストップロスを設定し、異常な相場変動による巨額損失を回避できます。

-

買い増し回数、比率、利確比率などのパラメータを最適化し、異なる銘柄に適応できるようにすることができます。

-

ボラティリティに応じて利確比率を動的に調整し、変動が大きい時期には適度に緩和することができます。

まとめ

本戦略は、RSIインジケーターを活用して売られ過ぎゾーンを判断し、価格移動平均線と組み合わせた逆張り取引を行います。同時に、スマートな買い増しと段階的利確メカニズムを用いることで、リスクを管理しつつ効率的なロング戦略を実現します。インジケーターパラメータや利確メカニズムなどを最適化することで、より安定・高効率な戦略に改善できます。本戦略は、株価指数先物や暗号通貨など、トレンド反転の特徴を持つ金融商品に広く応用でき、実用的な投資価値を持ちます。

- 1